I started buying Palantir (PLTR).

Not because it is cheap. It is not.

Not because the valuation suddenly became easy. It did not.

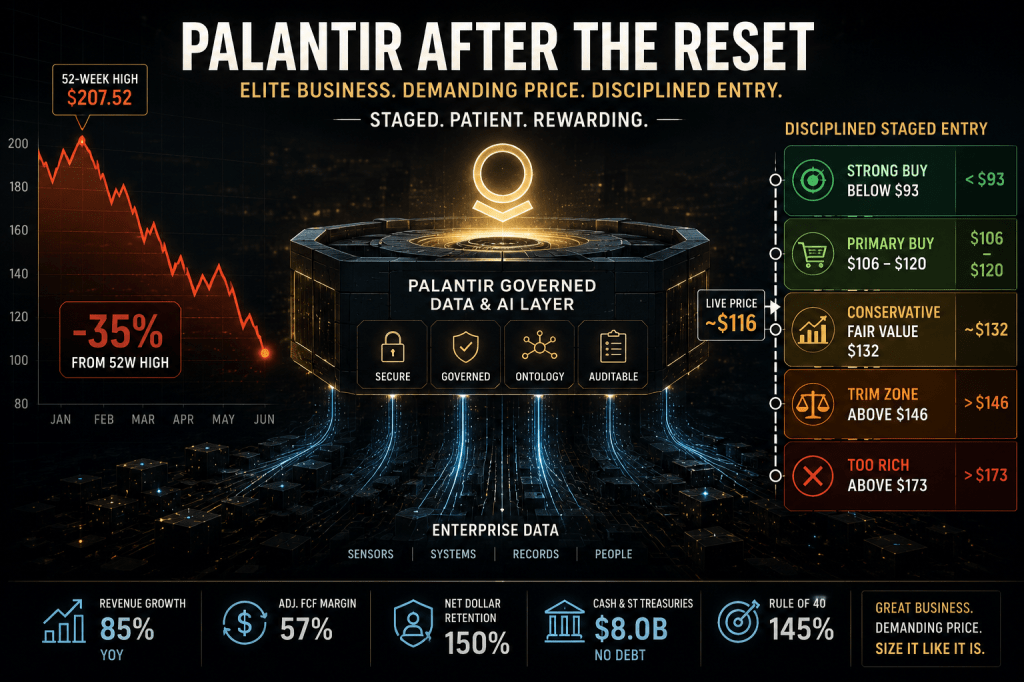

I bought a starter position because the reset finally moved the stock from “too hard to underwrite” to “ownable in the right size.” That distinction matters. A 35% drawdown from the 52-week high sounds like a bargain until you look at what is still embedded in the price. At roughly $116, Palantir still carries one of the most demanding valuations in public software. The market is not pricing this like a normal enterprise software company. It is pricing it like one of the few companies that might become a core operating layer for institutional AI.

That is the debate.

The business is exceptional. The price is still uncomfortable. The right answer, for me, is not all in or stay away. It is staged exposure.

I started with a 1% position in the growth IRA model portfolio and capped the name at 2%. That is the entire posture of this article. I like the company enough to own it. I respect the valuation enough to size it carefully.

What Palantir actually sells

The easiest way to misunderstand Palantir is to treat it like another AI software stock.

That misses the point.

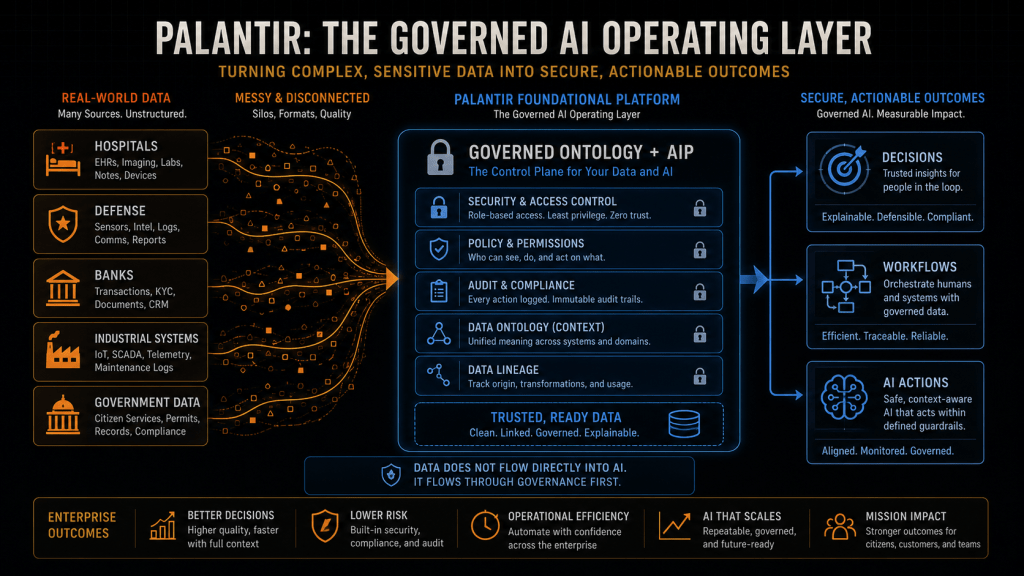

Palantir sells a governed decision layer for institutions that cannot afford sloppy data, uncontrolled AI outputs, or black-box automation. The company sits between messy enterprise data and high-consequence decisions. Its ontology organizes fragmented systems into a usable operating picture, and AIP lets humans and software act on that picture inside controlled guardrails.

That sounds abstract, so put it into real-world terms.

A hospital network cannot just dump patient records into a generic AI tool and hope nothing breaks. A defense agency cannot let a chatbot casually access classified intelligence. A bank cannot automate regulated workflows without permissioning, audit trails, lineage, and explainability. For those customers, governance is not a feature. Governance is the product.

That is Palantir’s moat.

The company is strongest where the cost of being wrong is high. Defense, intelligence, health care, energy, manufacturing, financial services, and large regulated enterprises are exactly the places where generic AI is powerful but dangerous without a control layer.

The more serious AI deployment gets, the more the question shifts from “Can the model answer?” to “Can the institution trust the model inside a real workflow?”

That is where Palantir has earned its reputation.

The quarter that changed the underwriting

Palantir’s Q1 2026 was not a normal software quarter.

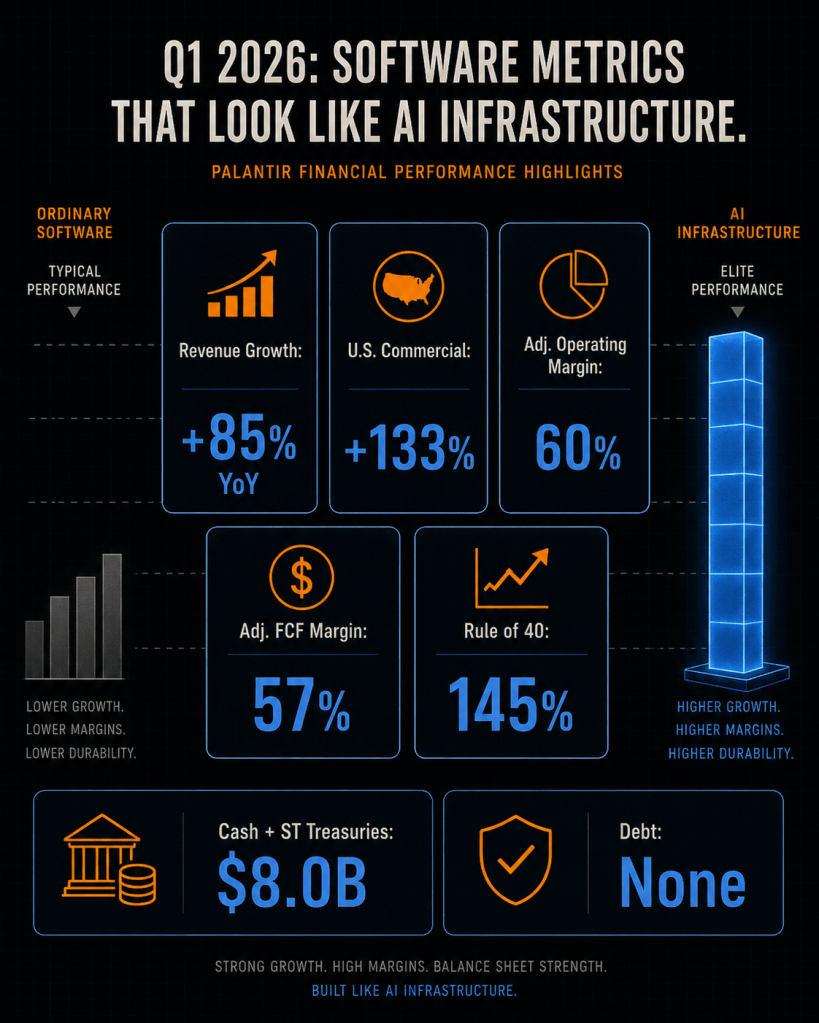

Revenue grew 85% year over year to $1.633 billion. U.S. revenue grew 104% to $1.282 billion. U.S. commercial revenue grew 133%. U.S. government revenue grew 84%. Those are not small-company numbers anymore. This is a large software company accelerating at a rate that most public software companies never reach in the first place.

The margin profile was just as unusual.

GAAP operating income was $754 million, a 46% margin. Adjusted operating income was $984 million, a 60% margin. Cash from operations was $899 million. Adjusted free cash flow was $925 million, a 57% margin. Rule of 40 came in at 145%.

That is why the stock gets treated differently.

Normal software companies do not grow revenue 85%, produce nearly 60% adjusted free cash flow margins, carry no debt, and raise guidance at the same time. Palantir is showing something closer to AI infrastructure economics than standard SaaS economics.

The balance sheet matters too. Palantir ended the quarter with roughly $8.0 billion of cash and short-term U.S. Treasury securities and no debt outstanding. That gives the company flexibility, but it also matters for the downside case. If growth slows, this is not a levered software business with balance sheet stress layered on top of multiple compression.

Then management raised full-year guidance. FY26 revenue is now expected at $7.650 billion to $7.662 billion, roughly 71% growth. Adjusted free cash flow is guided to $4.2 billion to $4.4 billion.

That is the bull case in hard numbers.

Why the recent deals matter

The Q1 numbers explain why Palantir deserves attention. The recent deal flow explains why the story may still be expanding.

The most important announcement was the June 29 partnership with Nvidia. Palantir and Nvidia launched an engine for deploying Nvidia’s open AI models into sovereign and critical-infrastructure environments. In plain English, Nvidia provides powerful AI models and compute architecture. Palantir provides the governed deployment layer that helps those models operate inside environments where security, compliance, and control matter.

That is strategically important.

Nvidia is my second-largest holding, so I pay attention when it chooses partners in sovereign AI and critical infrastructure. The signal is not that this single announcement changes Palantir’s financial model overnight. The signal is that Palantir is becoming part of the institutional AI deployment stack.

The Zeta Global partnership is a different kind of signal. On June 23, Palantir and Zeta announced a seven-year go-to-market partnership under which Zeta is rebuilding its data cloud on Palantir’s platform. Zeta’s CEO said the relationship could drive more than $100 million in annual revenue to Zeta over time.

That revenue does not accrue directly to Palantir, which is important to say clearly. The value to Palantir is validation. A marketing-AI company is choosing to rebuild core infrastructure on Palantir rather than treat Palantir as a side tool.

There was also an expanded relationship with Surf Air Mobility in the same window. That one is smaller, but it points in the same direction. Palantir is trying to become the platform other companies build on, not just a vendor they buy from.

That is a stronger strategic position.

The valuation problem is still real

Now comes the part that keeps me from getting carried away.

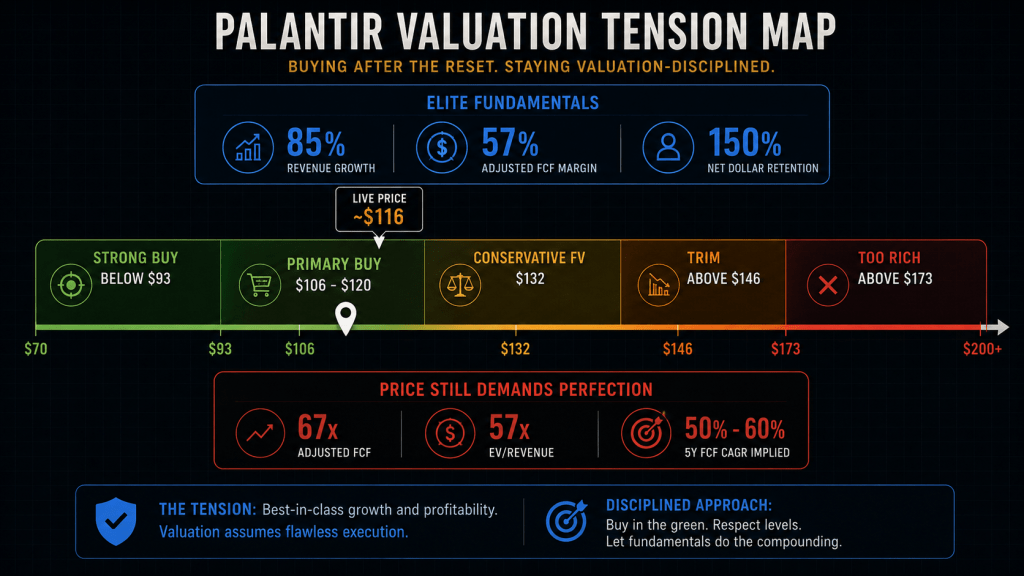

At roughly $116, Palantir is still expensive. Very expensive.

The stock trades around 67 times this year’s adjusted free cash flow guidance before any haircut for stock-based compensation. Enterprise value is roughly 57 times revenue. These are not “reasonable software multiple after a pullback” numbers. These are “elite execution for years” numbers.

That is why I do not call this a clean GARP buy.

It is a GARP-quality business. It is not yet a clean GARP-at-a-reasonable-price stock.

The distinction matters. Palantir clearly passes the growth and quality side of GARP. Revenue growth is extraordinary. Margins are elite. Free cash flow conversion is rare. The balance sheet is pristine. The company is raising guidance. The strategic position is improving.

But valuation is where the model tightens.

Stock-based compensation is the first adjustment. Q1 stock comp was about $201.6 million, up from $155.3 million a year earlier. I do not treat SBC as free. Under the Vulcan framework, SBC is an economic cost because it transfers value from shareholders to employees. It is not cash leaving the business today, but it is still dilution or buyback burden over time.

Start with FY26 adjusted free cash flow guidance around $4.3 billion at the midpoint. Annualize Q1 SBC, tax-adjust it, and the Vulcan economic free cash flow proxy lands closer to $3.66 billion. That is still outstanding. It is just not the same as underwriting the headline $4.3 billion as fully owner-equivalent cash flow.

The reverse DCF is the real gut check.

Using a live price near $116, diluted share count around 2.57 billion, net cash around $8.0 billion, and that economic free cash flow base, the market is effectively asking Palantir to compound free cash flow at roughly 50% to 60% a year for five years to justify today’s enterprise value.

That is a high bar.

A company can be exceptional and still fail to clear that bar. That is why my answer is staged buy, not aggressive buy.

Where fair value sits

My conservative Vulcan blended fair value is about $132.

That number is not magic. It is not a prediction. It is a center of gravity.

The blend weights my internal model at 60% and external analyst anchors at 40%. I do that because Palantir is a stock where fair value depends heavily on future growth assumptions. If you lean too hard on external price targets, you risk accepting market enthusiasm as analysis. If you lean too hard on a conservative internal model, you may understate what an elite AI platform can be worth if growth stays extreme for longer than normal.

The internal model is intentionally cautious because most of Palantir’s value lives in future growth value, not current earnings power. Greenwald-style earnings power valuation does not capture this kind of business well by itself. If you value Palantir only on current normalized cash earnings, you will almost certainly miss the upside. If you value it only on a heroic growth curve, you risk paying for perfection.

That is the whole tension.

My fair value zones are simple:

- Below $93 is the strong-buy area.

- $106 to $120 is the primary buy zone.

- Around $132 is the conservative fair value anchor.

- Above $146 is where I start thinking about trim discipline.

- Above $173 is too rich to chase.

At $116, the stock sits inside the primary buy zone, but not with enough margin of safety to justify a full-size position.

The five risks I am watching

The first risk is valuation perfection. The stock still requires a lot of future success. If growth slows faster than expected, the multiple can compress even if the company remains excellent.

The second risk is SBC. Palantir’s margins are outstanding, but the gap between adjusted free cash flow and economic free cash flow matters. If stock comp keeps rising with the share price, investors need to account for that dilution.

The third risk is government and political exposure. Palantir’s government work is durable, but it comes with headline risk, contract-cycle risk, and political controversy. The market can punish those headlines even when the financials are intact.

The fourth risk is margin normalization. A 60% adjusted operating margin is extraordinary. It may not be the right margin to capitalize permanently. If Palantir invests more aggressively in deployment, sales capacity, infrastructure, and partnerships, margins could move lower while revenue continues to grow.

The fifth risk is technical damage. The stock is still below key moving averages, with the 50-day around $140 and the 200-day around $160 in the recent setup. It recently printed a fresh 52-week low near $106. That level matters. If the stock loses $106 and cannot stabilize, the market may be rejecting the post-earnings reset.

That is why I want the position small enough that I can hold it through volatility instead of reacting emotionally to it.

My actual plan

I started with a 1% position.

I am capping the name at 2%.

That cap is not because I lack conviction in the business. It is because the valuation and volatility demand discipline. A high-conviction stock can still be a bad portfolio decision if the position size ignores drawdown risk.

The $106 to $120 range is where I am willing to add modestly. That is the primary buy zone.

If the stock falls into the $95 to $105 range without a fundamental break, I would get more aggressive. Below $93 is the zone where the valuation starts to offer a much better cushion, assuming guidance and business momentum remain intact.

A decisive reclaim of $128 would be the first signal that the breakdown is repairing. I would add with more confidence above that level if the next quarter confirms the revenue and free cash flow trajectory.

Above $146, I become more cautious. Above $173, I would not chase.

The invalidation triggers are also clear.

If Palantir cuts FY26 revenue guidance, I stop adding. If it cuts adjusted free cash flow guidance, I stop adding. If the stock sustains a close below $106 without stabilizing, I stop adding until the chart repairs.

I am not trying to win a debate about whether PLTR is cheap. It is not cheap. I am trying to own a small amount of an elite AI software platform at a price where the math is finally survivable.

Who should own it

For a long-term growth investor who can think in five-year windows and tolerate a 35% to 40% drawdown, PLTR is now ownable in pieces.

For a valuation-first investor, it is still a watchlist name unless it moves closer to $105 or below.

For a trader, the levels matter more than the story. A reclaim of $128 says the repair is underway. A sustained break below $106 says the market is not ready.

I fall into the first camp, but with strict sizing. I want exposure to the platform. I do not want a position so large that I am forced to sell it during the exact volatility I should have expected.

Master metrics table

| Metric | Value |

|---|---|

| Live price context | About $116 |

| 52-week high | $207.52 |

| Drawdown from high | About 35% |

| Market cap | About $283B to $298B |

| FY26 revenue guide | $7.650B to $7.662B |

| FY26 revenue growth implied | About 71% |

| FY26 adjusted FCF guide | $4.2B to $4.4B |

| Q1 2026 revenue growth | 85% YoY |

| Q1 U.S. revenue growth | 104% |

| Q1 U.S. commercial growth | 133% |

| Q1 U.S. government growth | 84% |

| Q1 adjusted operating margin | 60% |

| Q1 adjusted FCF margin | 57% |

| Rule of 40 | 145% |

| Net dollar retention | 150% |

| Cash and short-term Treasuries | $8.0B |

| Debt outstanding | None |

| Forward P/E | About 88x |

| EV / revenue | About 57x |

| Adjusted FCF multiple | About 67x |

| Vulcan economic FCF proxy | About $3.66B |

| Reverse DCF implied 5Y FCF CAGR | About 50% to 60% |

| GNG Quality Score | 84.1 |

| GNG Safety Score | 84.2 |

| Piotroski F-Score | 7 to 8 |

| 1-year max drawdown | About -37% |

| 50-day / 200-day MA | About $140 / $160 |

| Vulcan blended fair value | About $132 |

| Base 12-month target | $135 |

| Vulcan rating | Buy, staged |

| GARP verdict | GARP-quality business, conditional GARP buy |

| My position | Started 1%, capped at 2% |

Final view

The reset did not make Palantir cheap.

It made Palantir ownable.

That is the difference.

This is one of the strongest operating profiles in public technology: 85% revenue growth, 57% adjusted free cash flow margin, 150% net dollar retention, $8.0 billion of cash and short-term Treasuries, and no debt. The company is not just talking about AI. It is converting AI demand into revenue, margin, contracts, and guidance.

But the price still demands respect. The reverse DCF needs roughly 50% to 60% annual free cash flow growth for five years. That is not a casual assumption. That is an elite-execution assumption.

So my answer is deliberately balanced.

I want to own it. I do not want to over-own it.

I started small, I will add only in defined zones, and I will stop adding if the guidance or the chart breaks. For me, PLTR is a staged buy after the reset, not a clean bargain and not a stock to chase without discipline.

The business is elite. The price is demanding. The position size is what makes the math work.

References

- Palantir Q1 2026 results and FY26 guidance: SEC Form 8-K, Exhibit 99.1, May 4, 2026; Q1 2026 earnings materials.

- Palantir Q1 2026 Form 10-Q: stock-based compensation, cash, short-term Treasuries, and debt disclosure.

- Palantir and Nvidia sovereign AI engine announcement: company press release, June 29, 2026.

- Palantir and Zeta Global seven-year go-to-market partnership: company press releases, June 23, 2026.

- Palantir and Surf Air Mobility expanded partnership: company disclosure, June 29, 2026.

- Quality, safety, valuation, and technical metrics: GNG Research database and Vulcan screening cache. Database price fields are used as context only; live quote governs zones and return math.

This is research and analysis, not personalized investment advice. I hold the position described above. Do your own work before acting.

Leave a comment