On Sunday night, one of the most famous value investors of the last twenty years posted that he had bought more shares of PayPal (PYPL) at $40.98. His reasoning was almost boring in its simplicity: the company trades at seven to eight times earnings and is buying back its own stock hand over fist. No hype, no product reveal, no story about the next big thing. Just a cash-generating business that the market has decided to price as if the cash is about to stop.

Try GNG AI Analyst, simply ask it “Do a stock analysis of PYPL” or “Show a peer comparison for PYPL” – https://www.gngresearch.com/ai-console

That decision is the whole investment question. Picture a fully built office tower in a neighborhood that has fallen out of fashion. Tenants are paying rent on time, the elevators work, the books balance, and the owner is quietly buying back pieces of the building from nervous co-owners at a steep discount. Yet the official appraisal keeps dropping, because everyone assumes the tenants will eventually leave for the shiny new development across town. PayPal is that tower. The appraisal is the stock price. The rent is free cash flow. And the bet here is whether enough tenants stay long enough for the market to recheck its math.

The Tenants Everyone Expects to Leave

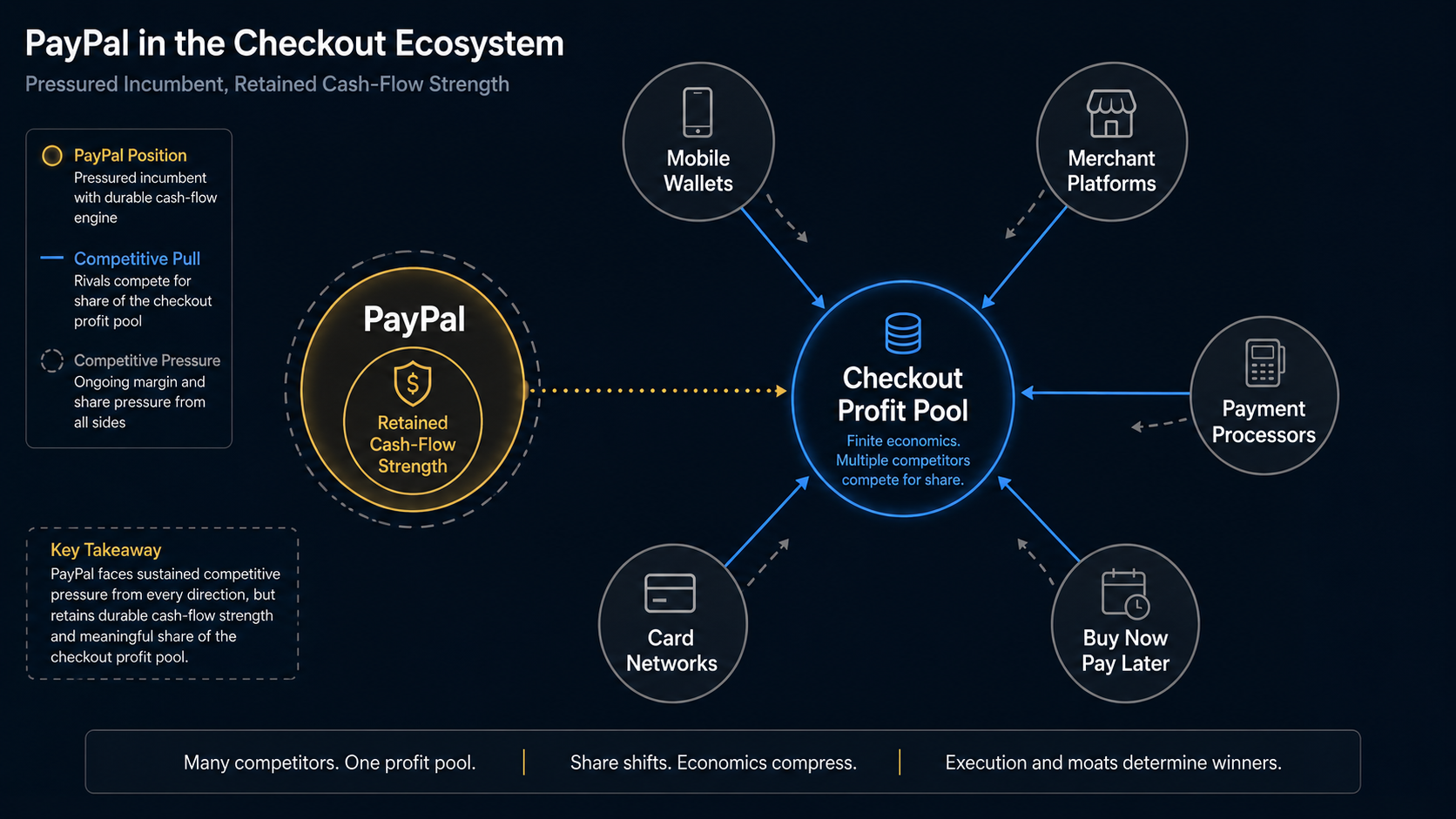

The fear is real and worth stating plainly. PayPal’s branded checkout button, the yellow one shoppers have clicked for two decades, faces the most serious competitive pressure in the company’s history. Apple’s wallet sits inside every iPhone. Stripe and Adyen power the back end of modern commerce. Shopify routes its own merchants. Klarna and the card networks keep expanding into checkout. When investors look at PayPal (PYPL), they see a once-dominant gateway slowly being routed around, and they price the equity for a long, quiet decline.

The first quarter of 2026 did not settle the argument. Revenue rose 7% to roughly $8.4 billion, total payment volume climbed 11% to $464 billion, payment transactions grew 7% to 6.5 billion, and active accounts edged up 1% to 439 million. Those are not the numbers of a dying business. But operating margin compressed, and management’s full-year guidance still points to flat-to-slightly-lower earnings. The market heard that and concluded the growth it is getting costs too much to produce. So the stock barely moved on an earnings beat, which is what happens when buyers want proof, not promises.

New leadership knows this. Chief Executive Enrique Lores, who took the role in March 2026, has reorganized the company into three focused units and laid out a plan built on simplification, cost discipline, and a heavier use of artificial intelligence across the platform. The reorganization is an admission that the old PayPal tried to do too much. Whether the new structure converts into stable transaction-margin dollars is the single operating fact that will decide this stock over the next year.

The Rent That Keeps Clearing

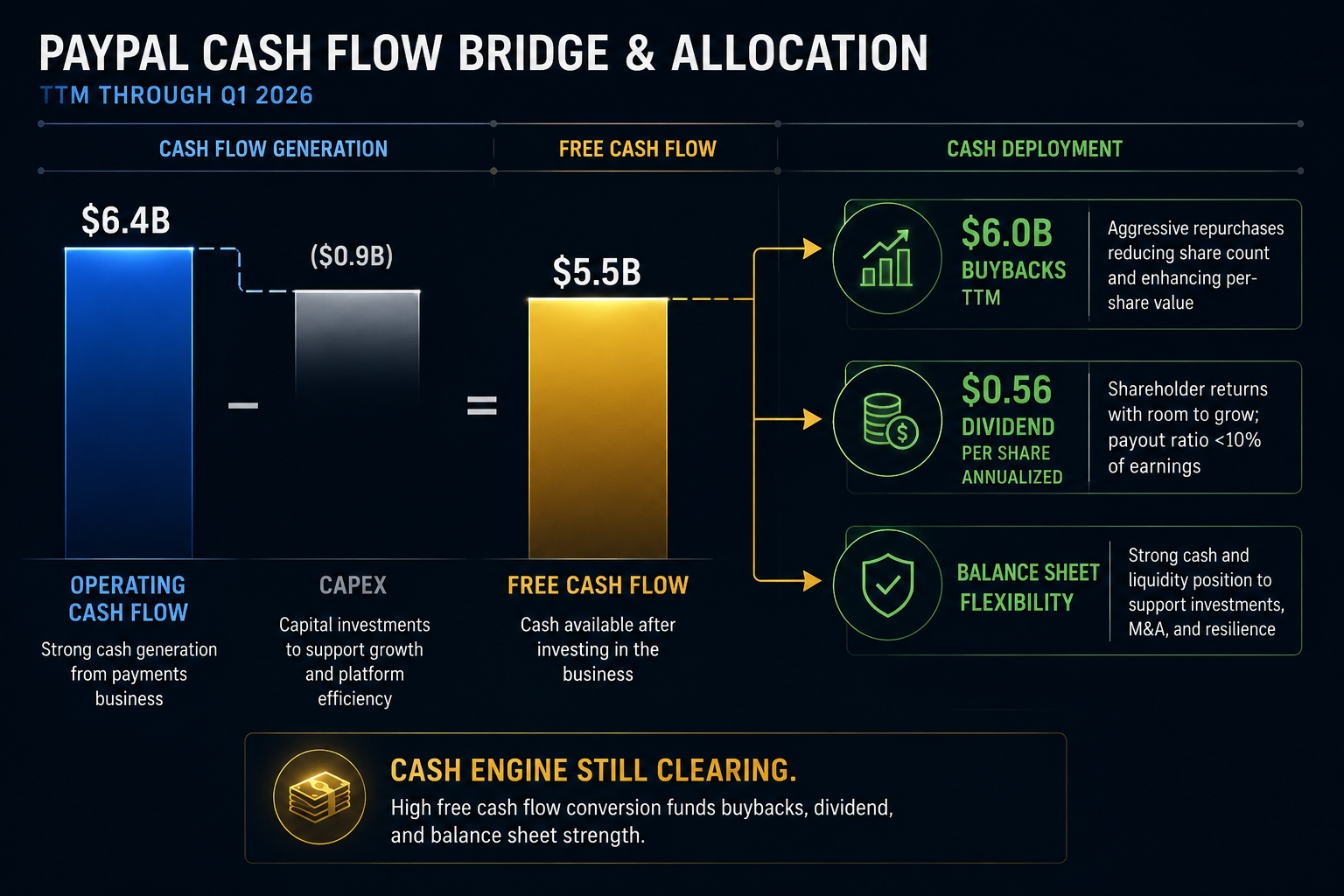

Here is the part the appraisal ignores. PayPal generated about $5.5 billion of trailing free cash flow on roughly $6.4 billion of operating cash flow, a free-cash-flow margin above 16%. In the first quarter alone, reported free cash flow was $0.9 billion and adjusted free cash flow reached $1.7 billion once you strip out the timing of buy-now-pay-later loans moving off the balance sheet. The cash engine is not sputtering. It is running at a level most companies its size would envy.

The company is doing the unglamorous, shareholder-friendly thing with that cash. PayPal repurchased about $1.5 billion of stock in the first quarter and roughly $6.0 billion over the trailing year, retiring close to 100 million shares. Share count has shrunk at nearly 6% a year over the past three years, which means every remaining owner’s slice of the rent quietly grows even if the building’s total income stays flat. In 2025 the company also initiated a dividend, now running at $0.14 per quarter, or about $0.56 annualized for a forward yield near 1.3%. The payout consumes well under a tenth of earnings, so it has room to grow without straining the cash flow.

Leverage is not the problem either, despite headlines about a fintech in trouble. Gross debt sits near $11.6 billion against $13.5 billion of cash and investments, interest coverage runs around fifteen times, and net debt to EBITDA is roughly a third of one turn. This is a balance sheet that can absorb a multi-year turnaround without forcing management’s hand. The cash, the buyback, and the modest dividend together are why a deep-value investor like the one who bought more on Sunday keeps circling back.

The Appraisal Gap

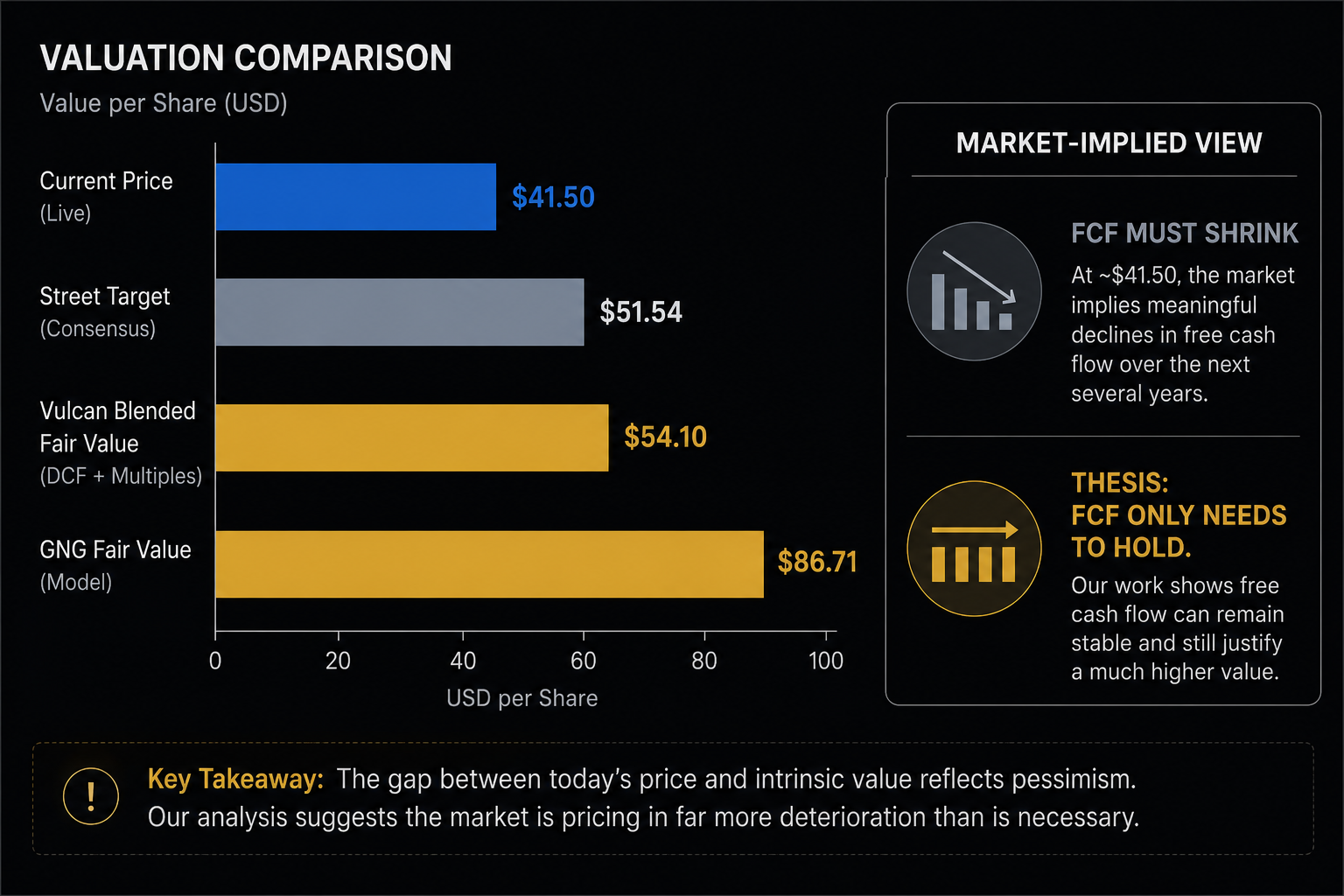

Now to the math that makes PayPal (PYPL) interesting rather than merely cheap. At roughly $41.50, the stock trades near 7.8 times forward earnings, about 6.9 times price-to-free-cash-flow, and just under 5 times EV/EBITDA, carrying a free-cash-flow yield above 14%. For a company still growing revenue in the mid-single digits with mid-teens net margins, those are multiples normally reserved for businesses in visible structural decline.

A blended fair value built from a stock-based-compensation-adjusted discounted cash flow, a free-cash-flow multiple, an earnings-power floor, and Street and independent anchors lands near $54 per share. That implies roughly 30% price upside from current levels before counting the dividend. The GNG Research valuation model is even more generous, flagging a fair value well above $80 and a discount to fair value near negative 52%, which in the GNG convention signals a stock trading far below its modeled worth. Two independent frameworks pointing to deep undervaluation does not guarantee the gap closes, but it does tell you the cushion is wide.

The most useful way to see the mispricing is to run the cash flows backward. At the current price and a conservative cost of equity, the market is implying that PayPal’s free cash flow will shrink every year for the next five years. The stock does not need a comeback to growth to work. It needs only to avoid a permanent decline in its cash generation. That is a low bar for a business still adding accounts, growing volume, and reorganizing itself to spend smarter.

What a Famous Buyer Is Actually Confirming

The recent disclosure that Michael Burry’s Scion Asset Management built a PayPal position, first revealed in its first-quarter filing and then publicly added to this past weekend, matters for a specific reason. It is outside confirmation of the read rather than a substitute for it. Burry framed PayPal exactly the way the numbers do: a cash-rich, low-leverage business buying back stock at a price that, in his words, should look attractive to private-equity firms and strategic acquirers at seven to eight times earnings. His emphasis was owner earnings and capital discipline, not momentum or a product catalyst.

His broader argument is worth understanding because it reframes why the stock fell. Burry has described the selloff in software and payments names as amplified by technical and financing pressures rippling through leveraged corners of the market, rather than a clean verdict that these businesses are broken. PayPal, in his telling, is precisely the kind of company that does not depend on fragile financing and so was punished by association. That distinction lines up with the GNG read: the balance sheet and cash flow are not the issue; confidence in the durability of transaction-margin dollars is.

For a serious investor, the correct way to hold this is simple. Burry’s involvement raises the odds that the market starts debating PayPal as an owner-earnings mispricing instead of dismissing it as a fading brand. It improves the setup and may shorten the wait. It does not remove the burden of proof. The company still has to show that branded checkout stops bleeding share, that Venmo finally monetizes at scale, and that the buyback is retiring stock below intrinsic value rather than papering over stagnation.

Reading the Technical Floor

The chart still shows a building that buyers have abandoned. PayPal (PYPL) is down about 44% over the past year, sits roughly 25% below its 200-day moving average near $55, and carries a 14-day relative strength index in the mid-30s with momentum indicators pointed down. This is a washed-out chart that has shown no real sign of repair yet. The first sign of repair would be a weekly close back above $46, the zone where the 50-day average and recent congestion sit. A reclaim of the 200-day around $55 would suggest larger institutions are beginning to underwrite the turnaround.

On the downside, support steps in near $41, then the 52-week low region around $38, then a deeper shelf near $35 that overlaps with the most conservative fair-value floors. The stock is sitting almost exactly on the first support level now, which is why staged entries make more sense than a single committed buy.

Five Risks Worth Pricing

The largest risk is business erosion rather than balance-sheet failure. If transaction-margin dollars, the cleanest measure of PayPal’s core profit engine, turn negative for two consecutive quarters, the entire cash-durability thesis weakens and the stock likely retests the $34 to $38 zone.

The second risk is the negative earnings-revision trend. Analyst estimates have been cut far more often than raised in recent months, and falling estimates tend to keep a lid on the multiple regardless of how cheap the stock looks on paper.

The third risk is stock-based compensation. Buybacks first have to offset shares issued to employees before they create real per-share value, so part of that $6 billion repurchase is treadmill spending rather than true shareholder yield.

The fourth risk is execution under new leadership. A reorganization announced is not a reorganization delivered, and the targeted cost savings could slip while competitors keep moving.

The fifth risk is simple impatience. This is a 12-to-24-month proof window, and a name with a 1.34 beta and around 40% one-year volatility can stay frustrating for several quarters before any rerating arrives.

Sizing and Execution

PayPal is a position for value-oriented investors who can sit through ugly price action and revision noise, not for anyone chasing momentum. The work here is patience, and the structure should reflect that. A staged entry fits the setup: a first tranche in the low $40s where the stock trades now, a second tranche near $40 if it revisits Burry’s add price, and a final value tranche only if the $38 low is tested without a fundamental break in the cash flows.

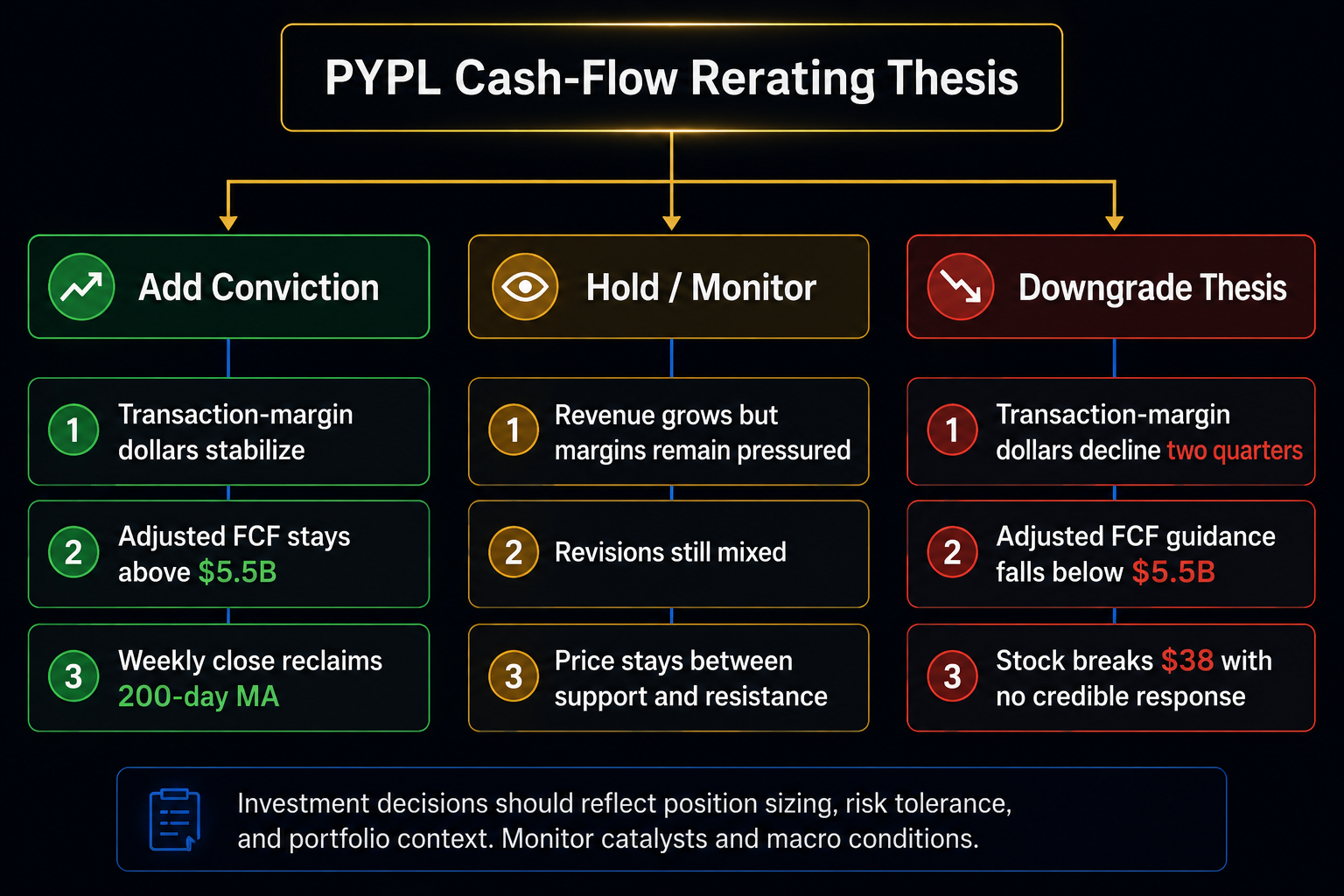

Sizing should respect the volatility. For most retail portfolios, a starting position of 1% to 2% that can build toward 3% to 4% across tranches keeps the risk contained while leaving room to benefit if the rerating comes. A disciplined stop sits around 15% below blended cost, but the more important invalidation is operational rather than technical. Downgrade conviction if transaction-margin dollars decline for two straight quarters, if adjusted free-cash-flow guidance falls below $5.5 billion, or if the stock breaks $38 while management offers no credible response. Add conviction if the next two quarters show stable transaction-margin dollars, accounts that stop slipping sequentially, and a weekly close that reclaims the 200-day line.

The honest summary is that PayPal is a cash-flow rerating candidate rather than a pristine compounder like Visa (V) or Mastercard (MA). The market has marked down the appraisal because it doubts how long the customers behind that cash flow will stay. What it appears to discount is that the rent is still clearing today, the balance sheet is clean, and management keeps buying back its own equity at a depressed price. A business like that does not need a heroic return to growth to reward an owner; it needs the cash to stop shrinking. Whether it does will show up in transaction-margin dollars over the next two quarters, and that figure is worth watching far more closely than the daily price.

Master Metrics Table

| Metric | PYPL |

|---|---|

| Last close (live) | ~$41.53 |

| As-of price in source doc | $42.95 |

| Market cap | ~$38B |

| P/E (TTM) | ~7.8x |

| Forward P/E | ~7.8x |

| Price / FCF | ~6.9x |

| EV/EBITDA | ~4.9x |

| FCF yield | ~14% |

| Vulcan Blended Fair Value | $54.10 |

| Upside to BFV (from ~$41.50) | ~30% |

| GNG Research Fair Value | $86.71 |

| GNG Discount to Fair Value | -52.1% (below FV) |

| Street target | $51.54 |

| Vulcan Score | 6.95 / 10 |

| Value Score | 9.80 / 10 |

| Quality Score | 8.50 / 10 |

| Momentum Score | 2.10 / 10 |

| ROIC | ~19% |

| Operating margin | ~18% |

| Net margin | ~15% |

| TTM operating cash flow | $6.39B |

| TTM free cash flow | $5.50B |

| Q1’26 adjusted FCF | $1.7B |

| TTM buyback | ~$6.0B (~100M shares) |

| Share count CAGR (3Y) | -5.8% |

| Forward dividend | $0.56 (initiated 2025) |

| Forward yield | ~1.3% |

| Payout ratio | ~8% |

| Gross debt | ~$11.6B |

| Cash and investments | ~$13.5B |

| Net debt / EBITDA | ~0.3x |

| Interest coverage | ~15x |

| Piotroski F-Score | 8 |

| Beneish M-Score | -2.49 |

| Beta | 1.34 |

| RSI (14) | ~35 |

| 200-day MA | ~$55 |

| 52-week range | ~$38 to ~$79 |

| 12-month return | ~-44% |

| Short interest | ~4.8% |

| Next earnings | July 27, 2026 |

| Rating | Strong Buy (staged) |

References

- PayPal Holdings Q1 2026 earnings release and 8-K, U.S. Securities and Exchange Commission, May 5, 2026.

- PayPal Holdings strategic reorganization 8-K, April 29, 2026, and CEO appointment release, February 3, 2026.

- PayPal Holdings FY2025 proxy and shareholder materials (dividend initiation, buyback totals), SEC filings, 2026.

- GNG Research terminal data, PayPal Holdings record (valuation, quality, technical, and capital-return metrics).

- Michael Burry, Scion Asset Management Substack commentary (the $40.98 add and the acquirer/buyback framing), as reported by Stocktwits, June 15, 2026. Recommend linking the original Substack post directly before publishing.

- Investing.com and CNBC, coverage of Scion Asset Management Q1 2026 13F disclosures, May 2026.

- Reuters, coverage of PayPal turnaround plan and competitive landscape, May 2026.

Leave a comment