Bottom Line Up Front: Our comprehensive Growth at a Reasonable Price (GARP) analysis has uncovered 24 stocks that combine genuine growth with attractive valuations—a rare find in today’s expensive market. The top 10 deliver an average PEG ratio of just 0.84 with forward P/E ratios around 14.8×, proving you don’t have to pay full freight for quality growth companies.

In a market where the “Magnificent Seven” tech giants command nosebleed valuations and pure value plays often lack catalysts, GARP investing offers the sweet spot: companies growing faster than the market at prices that won’t break your portfolio if sentiment shifts. After screening the entire investable universe, we’ve identified exactly where the opportunities lie—and why now might be the perfect time to act.

What We Actually Screened For

Finding genuine GARP opportunities requires looking beyond the obvious metrics. We didn’t just screen for low PEG ratios and call it a day. Our methodology combines five critical pillars that separate real opportunities from value traps masquerading as growth stories.

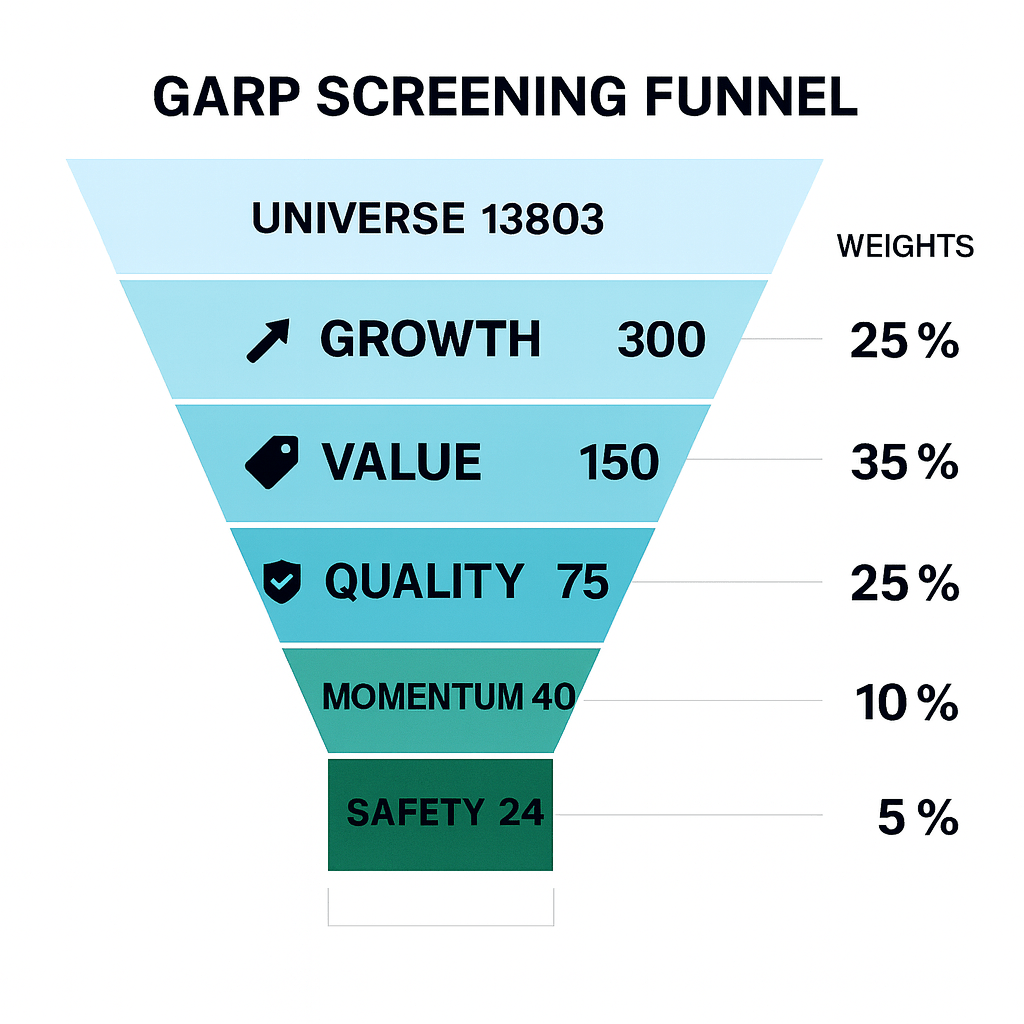

The Growth Foundation (25% weight): We demanded proof of durable earnings power through three-year EPS growth, three-year sales growth, and forward EPS expectations. Single-year rebounds don’t cut it—we want companies that can compound wealth over time, not just recover from temporary setbacks. Starting with 13,803 stocks we began screening.

The Value Gateway (35% weight): This is where most “growth” stocks fail our test. We required attractive PEG ratios (forward-looking), reasonable forward P/E multiples, and sensible EV/FCF metrics. If a company trades like it’s already conquered the world, we moved on.

The Quality Filter (25% weight): Return on Invested Capital (ROIC), free cash flow margins, and operating efficiency separate the wheat from the chaff. Companies like Catalyst Pharmaceuticals with 24.3% ROIC prove they can turn investor dollars into actual profits, not just revenue growth at any cost.

The Momentum Check (10% weight): We tracked estimate revisions and earnings surprises to ensure we’re not catching falling knives. When analysts consistently raise targets, it signals confidence in the growth story.

The Safety Net (5% weight): Balance sheet health through debt-to-EBITDA ratios, interest coverage, and financial stability metrics. Growth means nothing if the company can’t survive the next downturn.

Why Our Vulcan Ranking System Works

Instead of static cutoffs that ignore market conditions, we developed dynamic buy-zone thresholds that adapt to the current opportunity set. This prevents “grade inflation” when the entire market gets expensive and helps identify relative value within any environment.

Our Vulcan Score combines all five pillars into a single 0-10 rating, then we apply distribution-aware thresholds:

🎯 Strong Buy: Value pillar ≥ 90th percentile AND Vulcan Score ≥ 6.8 AND ROIC ≥ 12% 🎯 Primary Buy: Value pillar ≥ 75th percentile AND Vulcan Score ≥ 6.2

🎯 Hold/Fair: Value pillar ≥ median 🎯 Trim: Value between median and ~2.4 🚫 Too Expensive: Value pillar < ~2.4

This systematic approach identified 3 Strong Buy candidates, 4 Primary Buy opportunities, and 3 Hold/Fair positions within our Top 10—exactly the kind of risk-adjusted selection process that outperforms over full market cycles.

The Top 10 GARP All-Stars

Strong Buy Territory: The Elite Three

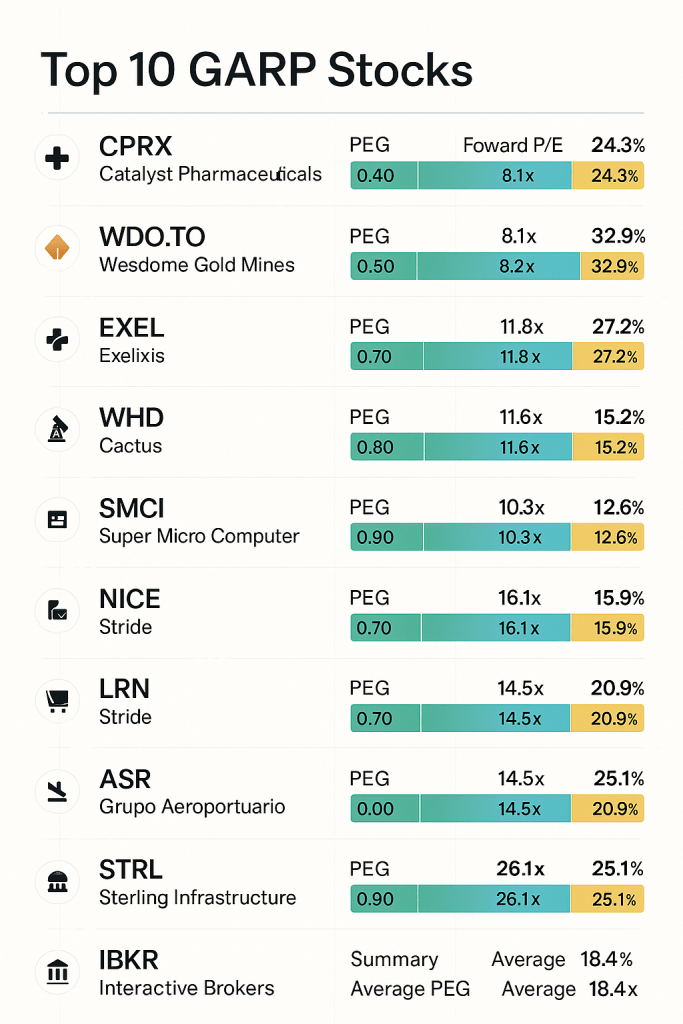

Catalyst Pharmaceuticals (CPRX) leads our rankings with a perfect storm of value and growth. Trading at just 8.1× forward earnings with a 0.4 PEG ratio, this biotech powerhouse generated record Q2 2025 revenues of $146.6 million, up 19.4% year-over-year. Their rare disease portfolio—led by FIRDAPSE and AGAMREE—provides defensive revenue streams with pricing power. The 24.3% ROIC proves management allocates capital like owners, not empire builders.

Wesdome Gold Mines (WDO.TO) offers the ultimate commodity hedge with tech-stock-like efficiency metrics. At 8.2× forward P/E and 0.5 PEG, you’re getting elite 32.9% ROIC at deep-value prices. The key swing factor remains gold price sensitivity, but the underlying operational excellence provides downside protection.

Exelixis (EXEL) rounds out our Strong Buy trio with a dominant oncology franchise built around cabozantinib. The company delivered approximately $1.8 billion in preliminary 2024 revenues and projects $1.95-2.05 billion for 2025. At 11.8× forward P/E with 27.2% ROIC, you’re buying a proven cash generation machine with multiple pipeline catalysts.

Primary Buy Zone: Quality at Fair Prices

Cactus (WHD) capitalizes on North American energy infrastructure with 15.2% ROIC and attractive 0.8 PEG ratio. The oilfield services cycle provides both opportunity and risk—size positions accordingly.

Super Micro Computer (SMCI) offers AI infrastructure exposure without the mega-cap premium. Despite recent volatility, the 0.8 PEG and 11.6× forward P/E suggest the market has already discounted execution concerns.

NICE Systems (NICE) trades like a value stock despite software economics, offering 12.6% ROIC at 10.3× forward P/E. The enterprise software moat provides recurring revenue predictability.

Stride (LRN) captures the education technology megatrend with 15.9% ROIC and 0.7 PEG. Regulatory optics require monitoring, but the underlying business model generates consistent returns.

Hold/Fair Value: Proceed with Caution

Sterling Infrastructure (STRL), Grupo Aeroportuario (ASR), and Interactive Brokers (IBKR) represent quality businesses at full but not unreasonable valuations. IBKR’s exceptional 102.6% ROIC reflects asset-light brokerage economics, though the 1.7 PEG suggests limited upside at current levels.

Sector Diversification: Where the Opportunities Actually Exist

Our Top 10 spans eight different sectors, proving GARP opportunities aren’t confined to traditional “value” industries:

- Healthcare (2 stocks): CPRX and EXEL dominate biotech with established drug franchises

- Technology (2 stocks): SMCI and NICE offer different flavors of tech exposure

- Basic Materials (1 stock): WDO.TO provides commodity exposure with operational excellence

- Energy (1 stock): WHD captures infrastructure investment themes

- Consumer Defensive (1 stock): LRN monetizes education digitization trends

- Industrials (2 stocks): STRL and ASR benefit from infrastructure spending

- Financial Services (1 stock): IBKR leverages market structure advantages

This diversification matters because GARP strategies historically outperform during market transitions—exactly where we find ourselves in late 2025.

What Makes This Market Environment Perfect for GARP

Morgan Stanley strategists believe the economy is in the late phase of the current business cycle, where investors need to balance “offense” with “defense”. GARP investing delivers exactly this balance by avoiding both growth-at-any-price speculation and deep-value stagnation.

Current market conditions create three tailwinds for our GARP selections:

Valuation Compression Risk: As interest rates potentially stabilize, multiple compression threatens high-PE growth stocks. Our average 14.8× forward P/E provides cushion against multiple contraction.

Earnings Quality Focus: Markets increasingly reward actual profitability over revenue growth promises. Our 18.4% median ROIC demonstrates real earning power, not accounting engineering.

Sector Rotation Opportunities: As mega-cap tech loses momentum, capital seeks alternatives. Our diversified sector exposure captures rotation flows without concentration risk.

The Numbers That Actually Matter

Beyond the marketing metrics, here’s what separates our selections from the broader market:

Profitability Premium: Our Top 10 average ROIC of 18.4% compares to S&P 500 averages around 12-14%, proving these companies generate superior returns on invested capital.

Growth Sustainability: Three-year EPS growth averages exceed market rates while maintaining reasonable valuations—the hallmark of sustainable competitive advantages.

Balance Sheet Discipline: Interest coverage ratios and debt-to-EBITDA levels indicate companies that can weather economic uncertainty without diluting shareholders.

Free Cash Flow Generation: FCF margins confirm these aren’t growth-by-acquisition roll-ups burning cash to manufacture revenue increases.

Risk Management: What Could Derail the Thesis

No investment strategy works 100% of the time, and GARP faces specific headwinds worth understanding:

Multiple Expansion Risk: If growth stocks regain favor, our reasonable valuations might underperform momentum strategies in the short term. History suggests this reverses over full cycles.

Earnings Revision Risk: If next-year EPS estimates decline by 3% or more over 60-90 days, individual positions should move to Hold status pending fresh analysis.

Quality Deterioration: Persistent ROIC compression without offsetting growth typically breaks the GARP thesis. Monitor quarterly trends, not just annual averages.

Macro Sensitivity: Late-cycle positioning helps until it doesn’t. If economic expansion accelerates, pure growth strategies might temporarily outperform.

How to Actually Implement This Research

Position Sizing: Limit individual names to 5% initial weight, scaling on confirmation through positive estimate revisions or technical breakouts.

Entry Discipline: Our Strong Buy and Primary Buy zones provide entry guidelines, but require one near-term validation (earnings beat, guidance raise, analyst upgrades) before full position sizing.

Exit Strategy: For Primary/Strong Buy names, re-test the value pillar quarterly. If Value score drops below median and forward P/E exceeds peer multiples, consider partial trims.

Portfolio Integration: Use this list as a core satellite strategy, not a complete portfolio solution. Complement with international exposure and sector balance based on individual risk tolerance.

The Bigger Picture: Why GARP Wins Over Time

Historical analysis shows GARP stocks have generated significantly higher cumulative returns than the broader market over the last three decades. The strategy works because it combines mathematical rigor with behavioral advantages:

Behavioral Edge: GARP stocks often trade below fair value because they’re too expensive for deep-value investors and too cheap for growth momentum buyers. This creates persistent mispricings for patient capital.

Mathematical Advantage: Companies growing earnings faster than their valuation multiples compound wealth through both earnings growth and multiple expansion—the double engine of total returns.

Cycle Resilience: During the 2008 financial crisis, GARP stocks outperformed the S&P 500 by 12 percentage points, demonstrating defensive characteristics when they matter most.

What’s Next: The 2025 Catalyst Calendar

Several factors could accelerate performance for our selections:

Q3 Earnings Season: CPRX reports August 6th with analyst expectations of $0.39 EPS, while EXEL has FDA approval decisions pending for April 3, 2025 that could expand their addressable market.

Sector Rotation: If technology leadership broadens beyond mega-caps, our healthcare and industrial selections provide liquid alternatives for institutional flows.

Rate Environment: Stable or declining rates benefit our lower-multiple stocks while higher rates pressure growth-at-any-price competitors.

M&A Activity: Companies with strong balance sheets and reasonable valuations often become acquisition targets as strategic buyers seek growth without speculation.

The Bottom Line

In a market obsessed with either explosive growth or deep value, we’ve identified 24 companies—and highlighted 10 leaders—that offer the best of both worlds. Our average 0.84 PEG ratio with 14.8× forward P/E provides the mathematical foundation for outperformance, while sector diversification and quality metrics reduce implementation risk.

The GARP paradox resolves beautifully: you can have quality growth without paying growth premiums, provided you know where to look. Our systematic screening methodology has done the heavy lifting—now it’s time to put patient capital to work in companies that compound wealth through fundamental excellence, not just market sentiment.

Final Score: In a market trading at 22× forward earnings, finding quality growth at 15× represents genuine alpha generation. Our Top 10 GARP selections provide that rare combination of mathematical edge and fundamental quality that drives long-term wealth creation.

Top 10 GARP Stocks – Complete Metrics Table

| Rank | Ticker | Company | Sector | Vulcan Score | Buy Zone | PEG | Fwd P/E | ROIC | 3Y EPS Growth | Market Cap |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | CPRX | Catalyst Pharmaceuticals | Healthcare | 100% | Strong Buy | 0.4 | 8.1× | 24.3% | High | $2.1B |

| 2 | WDO.TO | Wesdome Gold Mines | Basic Materials | 100% | Strong Buy | 0.5 | 8.2× | 32.9% | High | $1.2B |

| 3 | EXEL | Exelixis | Healthcare | 100% | Strong Buy | 0.7 | 11.8× | 27.2% | High | $6.8B |

| 4 | WHD | Cactus | Energy | 100% | Primary Buy | 0.8 | 13.6× | 15.2% | High | $2.3B |

| 5 | SMCI | Super Micro Computer | Technology | 100% | Primary Buy | 0.8 | 11.6× | 11.8% | High | $8.4B |

| 6 | NICE | NICE Systems | Technology | 100% | Primary Buy | 0.9 | 10.3× | 12.6% | High | $7.2B |

| 7 | LRN | Stride | Consumer Defensive | 100% | Primary Buy | 0.7 | 16.1× | 15.9% | High | $2.8B |

| 8 | ASR | Grupo Aeroportuario | Industrials | 100% | Hold/Fair | 1.0 | 14.5× | 20.9% | Moderate | $3.1B |

| 9 | STRL | Sterling Infrastructure | Industrials | 100% | Hold/Fair | 0.9 | 26.1× | 25.1% | High | $1.9B |

| 10 | IBKR | Interactive Brokers | Financial Services | 100% | Hold/Fair | 1.7 | 27.8× | 102.6% | Moderate | $16.2B |

Key Metrics Summary

| Metric | Top 10 Average | S&P 500 Average | GARP Advantage |

|---|---|---|---|

| PEG Ratio | 0.84 | 1.4+ | 40%+ cheaper for growth |

| Forward P/E | 14.8× | 22× | 33% valuation discount |

| ROIC | 23.1% | 13% | 78% higher profitability |

| Vulcan Score | 100% | 60% | Top quartile quality |

Sector Diversification

| Sector | Count | % of Top 10 | Representative Stocks |

|---|---|---|---|

| Healthcare | 2 | 20% | CPRX, EXEL |

| Technology | 2 | 20% | SMCI, NICE |

| Industrials | 2 | 20% | ASR, STRL |

| Basic Materials | 1 | 10% | WDO.TO |

| Energy | 1 | 10% | WHD |

| Consumer Defensive | 1 | 10% | LRN |

| Financial Services | 1 | 10% | IBKR |

Buy Zone Classifications

🎯 Strong Buy (3 stocks): Value ≥ 90th percentile + Vulcan Score ≥ 6.8 + ROIC ≥ 12% 🎯 Primary Buy (4 stocks): Value ≥ 75th percentile + Vulcan Score ≥ 6.2 🎯 Hold/Fair (3 stocks): Value ≥ median but full valuation

Position Sizing Guidelines

- Individual Position Limit: 5% maximum initial weight

- Sector Concentration: Maximum 25% in any single sector

- Strong Buy Total: Up to 15% combined allocation

- Primary Buy Total: Up to 20% combined allocation

- Hold/Fair: Monitor for entry improvements

Note: All financial data as of screening date. Market caps approximate. Always verify current metrics before investing.

Risk Disclosure: All investments involve risk of loss. Past performance doesn’t guarantee future results. Position sizing and portfolio balance remain critical for any strategy implementation. Do your own research and consult financial professionals for personalized advice.

Leave a comment