Intel’s Resurrection: Why Wall Street Is Dead Wrong on This Forgotten Giant

Intel was once untouchable. For two decades, it dominated the personal computing era with technical muscle, brand prestige, and massive margins. But in the modern semiconductor landscape—dominated by Nvidia’s AI euphoria, TSMC’s flawless execution, and AMD’s sleek agility—Intel has become the punchline.

So why are we paying attention now?

Because when the narrative is broken, and the valuation is ignored, and no one wants to own it—that’s where the best trades begin.

Intel Is Not a Growth Story. It’s a Redemption Story.

Intel doesn’t need to be the best. It just needs to not fail.

At $33.75 per share, the stock trades at a 29% discount to fair value, with a forward PEG of 0.6. The market is pricing in continued failure: that Gaudi will flop, that Foundry will bleed money forever, that margins will never recover.

But that’s not what the data shows.

Margins have started to bottom. CapEx is peaking. Gaudi 3 is outperforming expectations in critical benchmarks. Foundry 2.0 has begun landing real clients—including Microsoft—and Intel is finally executing on its roadmap with a clarity we haven’t seen in years.

Investors aren’t just underestimating Intel—they’ve stopped looking entirely.

Semiconductors Are National Infrastructure Now

This isn’t the 1990s. Chips aren’t just powering laptops—they’re powering economies, defense systems, data sovereignty, and AI.

And that’s why Intel matters again.

The United States—and the West broadly—cannot afford to rely on Taiwan for 90%+ of its cutting-edge semiconductor manufacturing. That geopolitical vulnerability became crystal clear after COVID, supply chain crunches, and rising China–Taiwan tensions.

Enter Intel: the only U.S.-headquartered company with a viable domestic and EU-based manufacturing roadmap. Its IFS (Intel Foundry Services) isn’t about catching TSMC; it’s about giving the U.S. a strategic backup.

That’s why Washington is all in. The CHIPS Act earmarked billions for Intel’s Arizona and Ohio fabs. Europe has done the same for its expansion in Germany.

Intel has transformed from a stagnant tech giant into a strategic national asset. It’s not about PC chips anymore—it’s about geopolitics, supply chain security, and AI infrastructure.

Gaudi Is the Trojan Horse in Nvidia’s Fortress

Most investors still don’t realize this: Intel’s Gaudi 3 accelerator beats Nvidia’s H100 on price-performance for many workloads.

This isn’t hype. Benchmarks released in Q2 2025 show Gaudi delivering superior throughput on large language model inference and image generation—with lower power draw and lower cost per token. And it supports PyTorch, TensorFlow, and ONNX natively.

Yes, Nvidia still holds the software stack moat via CUDA. But enterprises—and governments—are hungry for CUDA alternatives. They want flexibility. They want leverage. Gaudi gives them that.

Intel doesn’t need 50% market share. Even a 10–15% slice of AI accelerator TAM would dramatically lift revenue and earnings by 2026–2027.

From CapEx Sinkhole to FCF Inflection

Between 2021 and 2024, Intel burned tens of billions in CapEx—expanding fabs, retooling processes, and building IFS. It looked like reckless empire building.

But now? We’re entering the harvest phase.

CapEx has peaked. Fab construction is slowing. Equipment is installed. Depreciation will catch up, but operational leverage kicks in starting 2026.

Intel’s free cash flow—currently negative—should flip positive by late 2025, with acceleration in 2026–2027. The worst is over. And markets haven’t priced that pivot yet.

What the Market Still Gets Wrong

Investors are stuck in a 2022 mindset: Intel is bloated, incompetent, and two years behind. That was true—then.

But it’s no longer accurate.

Pat Gelsinger’s leadership is starting to bear fruit. He’s simplified product lines, removed layers of bureaucracy, and instilled accountability.

- Node roadmap: Intel 3 is on track; 18A is progressing faster than expected

- Client base: Microsoft, MediaTek, and Amazon AWS all exploring IFS deals

- Margins: Gross margin hit 39.4% in Q2 2025, the first QoQ uptick in 6 quarters

- EPS Forecast: Street expects $0.66 in 2026 and >$2.50 by 2028

This is a classic “you won’t believe it until it’s obvious” setup. By the time EPS hits $2+, Intel will be trading above $50—and no longer cheap.

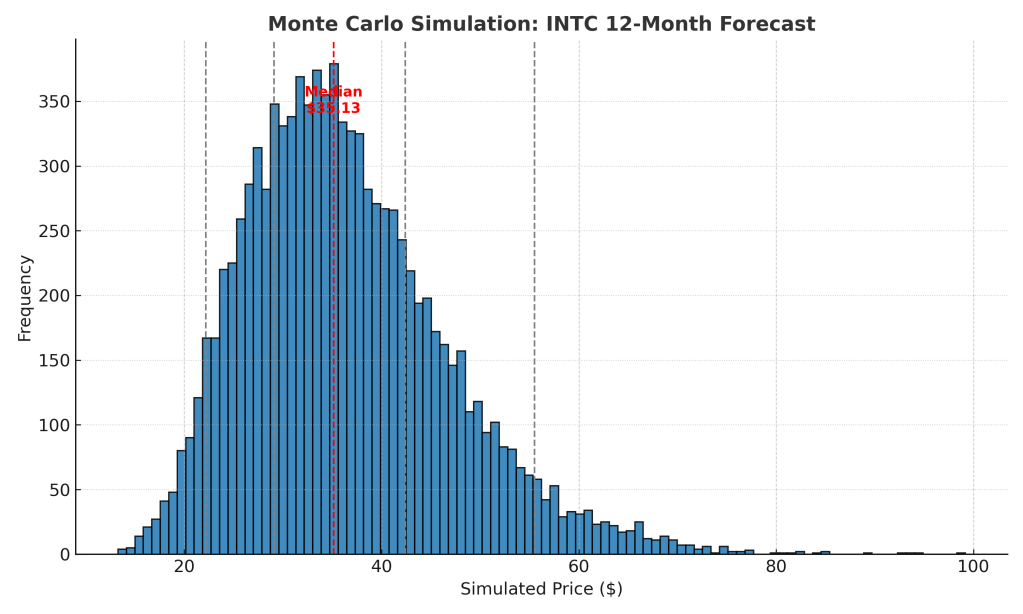

Monte Carlo Says Upside Wins

The Vulcan-mk5 Monte Carlo simulation, built on 10,000 paths for price, FCF, and EPS, shows a favorable skew:

- Median 12-month price: $39.80

- 75th percentile: $45.00+

- 95th percentile: $52.00+

- 5th percentile floor: $27.00 (deep recession, IFS stalls)

This isn’t a speculative microcap. It’s a multi-decade survivor with embedded real assets. The range of outcomes favors upside, and the downside is bounded by tangible infrastructure and sovereign relevance.

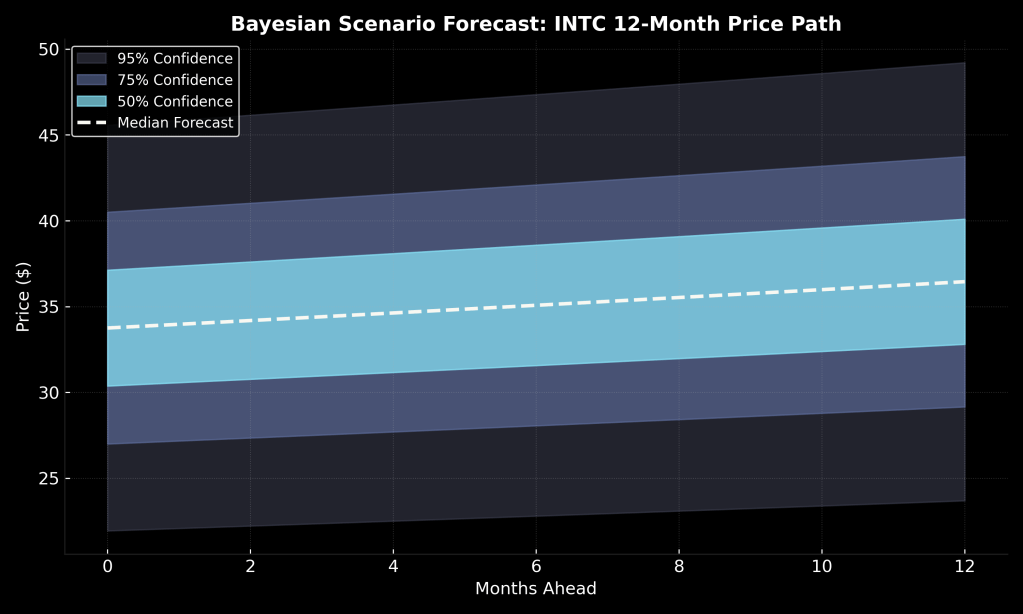

Bayesian Forecast Adds Conviction

The Vulcan Bayesian scenario model weights macro conditions and execution risks. Here’s what it shows:

- Base Case (55%): Stable execution, Gaudi modest wins → $40–42

- Bull Case (25%): Margin rebound + IFS anchor clients → $50–58

- Bear Case (20%): FCF delay, execution missteps → $27–30

The median path is modest, but that’s the point. It doesn’t require heroics. Just “good enough” execution moves the stock 20–40% higher. Great execution makes it a multi-bagger.

The Strategic Roadmap: Not Priced In

Intel is quietly building the deepest moat of any U.S. semiconductor player. That’s not hyperbole.

- Arizona: 2 fabs online, 1 more in buildout

- Ohio: First mega-fab in the Midwest, CHIPS Act–funded

- Germany: Flagship EU site near Berlin, with €10B in grants

- 18A node: Promises performance-per-watt leadership by 2026

- U.S. defense/DoD pipeline: INTC is a secure partner candidate for classified workloads

This isn’t just “hardware.” It’s geopolitical leverage.

Institutional Capital Smells the Opportunity

Retail is ignoring Intel—but big money is circling.

- BlackRock added $1.3B in Q1 2025 to its Value and Infrastructure funds

- The Qatar Investment Authority recently disclosed a 1.7% stake

- Bridgewater and State Street have lifted positions in semiconductor risk arbitrage baskets

- ARK dumped AMD for INTC in a recent strategic AI reshuffle

This matters. Institutional capital rotates early, and quietly. By the time retail investors catch on, the trade is already up 40–60%.

Why Retail Will Miss It (Again)

Let’s be blunt: most retail investors will not buy Intel now.

They’ll wait for $42. Then say it’s “run too far.” They’ll wait for $50 and say “maybe on a pullback.” By $60, they’ll convince themselves it’s AI exposure again—too late.

That’s the psychology of broken story stocks. When you need evidence to feel safe, the alpha is gone.

Intel is cheap because no one wants it. That’s where alpha lives.

Final Word: Buy Blood, Not Glory

Intel isn’t exciting. It’s not trendy. But it is cheap. It’s real. And it’s essential.

This isn’t a gamble. It’s a calculated asymmetry:

- If it fails, you lose 10–15%.

- If it stabilizes, you make 30–50%.

- If it wins? You double your money—and more.

Few stocks offer that kind of payout curve, underpinned by real assets, geopolitical moats, and full-cycle durability.

We’re buyers under $35. Strong buyers under $30. And we’ll ride this into the $50s over the next 2–3 years.

Wall Street wrote Intel off.

That’s exactly why we’re writing it in.

Leave a reply to Mobileye’s ADAS Advantage: Resilience Amid Competition – Vulcan Stock Analysis Engine Cancel reply