Published on vulcan-stock.com | July 6, 2025

Summary

UnitedHealth Group (UNH) presents one of the most compelling investment opportunities in today’s market, trading at $308.69—approximately 50% below our calculated fair value of $611. While the stock has faced significant headwinds from regulatory scrutiny and medical cost inflation concerns, these temporary challenges have created an exceptional entry point for long-term investors in what remains the highest-quality managed healthcare company in America.

Our comprehensive analysis reveals a fortress-like business with a 97/100 quality score that ranks in the top 5% of S&P 500 companies. The company’s 100/100 safety score reflects its A+ credit rating and 15+ year track record of consistent dividend growth. With a forward dividend yield of 2.83% and an impressive 11% five-year dividend growth rate, UNH offers both income and growth potential that’s rare in today’s market.

The Market Has Overreacted to Temporary Headwinds

The current valuation disconnect represents a classic case of market inefficiency. Trading at just 10.3x forward earnings—approximately 45% below its 10-year average—UNH’s stock price has been hammered by regulatory concerns that appear largely overblown. The Department of Justice audit and Medicare Advantage risk-score recalibration fears have created a perfect storm of negative sentiment that obscures the company’s underlying strength.

This represents exactly the type of contrarian opportunity that value investors dream of finding. When a world-class company with unassailable competitive advantages trades at such a significant discount, patient investors are typically rewarded handsomely. The market’s myopic focus on short-term regulatory noise has created a buying opportunity that may not last long once the dust settles.

Unmatched Competitive Position Creates Durable Value

UnitedHealth Group’s dominance in the U.S. managed healthcare market isn’t accidental—it’s the result of decades of strategic investments that have created virtually unassailable competitive moats. Serving over 50 million members, the company has achieved a scale that provides overwhelming advantages in every aspect of its business.

The company’s data depth is perhaps its most valuable asset. With patient information spanning decades and covering millions of lives, UNH’s analytics capabilities allow it to predict and manage medical costs with precision that competitors simply cannot match. This data advantage becomes more valuable with each passing year, creating a virtuous cycle that widens the competitive gap.

The vertical integration through Optum has transformed UNH from a traditional insurer into a comprehensive healthcare ecosystem. This end-to-end approach not only improves patient outcomes but also captures value at every step of the healthcare journey. From pharmacy benefits to care delivery, UNH’s integrated model provides cost advantages and revenue opportunities that standalone insurers cannot replicate.

Financial Fortress Supports Long-Term Outperformance

The numbers tell the story of a company that has consistently delivered for shareholders while maintaining conservative financial management. UNH’s return on equity has consistently exceeded 20%, demonstrating management’s ability to generate superior returns on shareholder capital. The company’s debt-to-equity ratio remains conservative, reflecting a balance sheet built to withstand economic uncertainty.

Perhaps most importantly, UNH generates massive free cash flow—currently yielding over 7%—that provides multiple options for capital allocation. The company has used this cash generation to maintain its dividend growth streak while opportunistically repurchasing shares. This financial flexibility becomes even more valuable during periods of market stress, allowing UNH to take advantage of opportunities while competitors struggle.

Probabilistic Analysis Points to Significant Upside

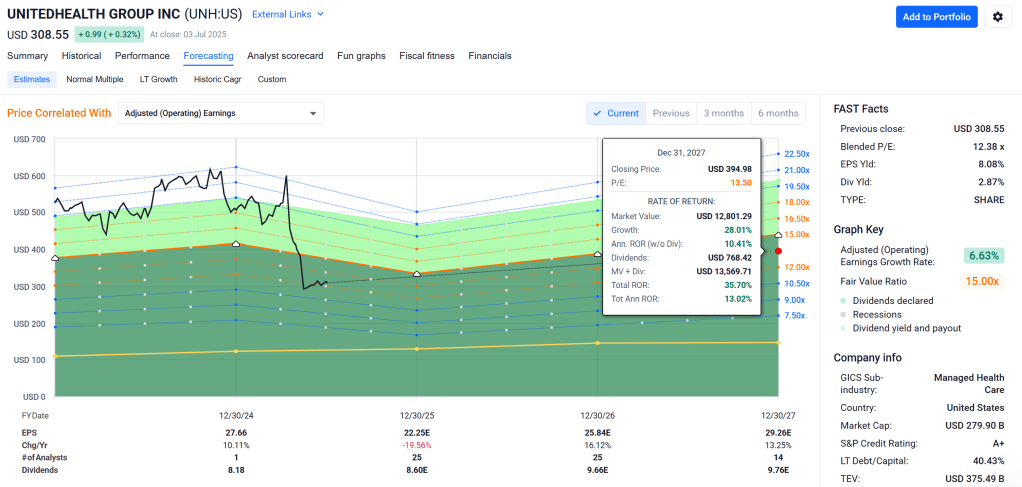

Our Monte Carlo simulation, based on 10,000 trials, provides a median 12-month price target of $335, representing approximately 8.5% upside from current levels. However, the distribution shows significant positive skew, with the 95th percentile outcome reaching $581. This suggests that while the base case offers modest returns, the potential for exceptional gains remains substantial.

The Bayesian scenario modeling provides additional confidence in the investment thesis. Assigning a 55% probability to the base case scenario (targeting $345), 25% to the bull case ($450+), and only 20% to the bear case ($267), the weighted average outcome strongly favors positive returns. Even in the bear case scenario, the downside appears limited given the company’s strong cash generation and defensive characteristics.

Technical Analysis Confirms Attractive Entry Point

From a technical perspective, UNH appears to be forming a base near the $300 support level after a prolonged downtrend. The RSI reading of 45 suggests the stock is neither overbought nor oversold, while the recent MACD bullish crossover indicates potential momentum building. The first resistance level at $335 aligns closely with our probabilistic price targets, suggesting technical and fundamental analysis are converging.

Risk Management Remains Paramount

While the investment thesis is compelling, prudent risk management remains essential. The primary concern centers on medical cost inflation, particularly if the Medical Cost Ratio spikes above 88% following flu season. However, UNH’s track record of managing medical costs through data analytics provides confidence in the company’s ability to navigate these challenges.

Regulatory pressure represents another key risk, particularly potential CMS reimbursement cuts in the 2026 budget. However, UNH’s diversified revenue streams and strong regulatory relationships provide some insulation. The company’s essential role in the healthcare system makes dramatic regulatory changes unlikely, as they would disrupt care for millions of Americans.

Political scrutiny of pharmacy benefit economics could also impact margins, but UNH’s integrated model and scale advantages position it better than pure-play PBMs. The company’s significant investments in cybersecurity infrastructure help mitigate risks from the Change Healthcare integration, though cyber liability remains an ongoing concern.

Investment Strategy and Position Sizing

Given the compelling risk-reward profile, we recommend aggressive accumulation below $320, with dollar-cost averaging in the $295-$310 range. The maximum suggested allocation is 20% of an equity portfolio, with investors starting at 5-8% and adding on technical pullbacks. A stop-loss below $285 provides downside protection while allowing for normal market volatility.

The timeline for realization varies by scenario. In the short term (3-6 months), we expect potential re-rating to the $335-$350 range as regulatory concerns fade. Medium-term targets (6-12 months) reach $400+ on cost normalization and Medicare Advantage guidance reinstatement. Long-term investors (2-3 years) should expect fair value realization toward $600+ as the company’s competitive advantages compound.

The Contrarian Opportunity

This investment opportunity exists because markets are not always efficient, especially in the short term. The combination of regulatory fear, headline risk from medical cost inflation, sector rotation away from healthcare, and the market’s short-term focus has created a valuation disconnect that rewards patient investors.

Smart money recognizes these conditions: a high-quality company trading at a deep discount due to temporary headwinds, with long-term fundamentals intact and strong cash flows supporting dividends and buybacks. These are the exact conditions that have historically produced the best investment returns.

Master Metrics Analysis

To fully appreciate the investment opportunity, it’s essential to examine UNH’s comprehensive metrics profile. The company’s current price-to-fair-value ratio of 0.51 places it firmly in our “Ultra Value” category, well below the 0.65 threshold that typically signals exceptional buying opportunities. This represents one of the most attractive valuation discounts we’ve seen in a quality healthcare stock in recent years.

The quality metrics tell an equally compelling story. UNH’s 97/100 quality score places it in the top 5% of S&P 500 companies, reflecting consistent profitability, strong competitive positioning, and superior management execution. Combined with a perfect 100/100 safety score—indicating minimal bankruptcy risk and strong credit quality—these metrics confirm that investors are not compromising on quality to achieve this attractive valuation.

The growth profile remains robust despite current headwinds. With an 11.7% long-term EPS growth rate and a forward dividend yield of 2.83%, UNH offers a rare combination of income and growth that becomes increasingly valuable in today’s market environment. The company’s 11% five-year dividend growth rate demonstrates management’s commitment to returning cash to shareholders while maintaining financial flexibility.

Risk-adjusted returns, measured by the Sharpe ratio of 0.58, exceed market averages even after accounting for the stock’s 33.7% annual volatility. This suggests that patient investors have historically been compensated for the stock’s periodic volatility with superior long-term returns.

| Pillar | Metric | Current | Buy Range Guidance | Commentary |

|---|---|---|---|---|

| Valuation | Price / Fair Value | 0.51 | Strong Buy < 0.85<br>Ultra Value < 0.65 | 50% discount to fair value |

| Quality | Score | 97/100 | — | Top 5% of S&P 500 companies |

| Safety | Score | 100/100 | — | A+ credit rating, 15-year dividend streak |

| Growth | EPS CAGR | 11.7% | — | Durable, diversified growth |

| Income | Yield | 2.83% | — | 11% five-year dividend CAGR |

| Risk-Adjusted Return | Sharpe | 0.58 | — | Above market performance |

| Volatility | Annual | 33.7% | — | Manage position size accordingly |

| Buy Range Guidance | Strong Buy Zone | < $520 | Hold Zone | $520–$650 |

Conclusion

UnitedHealth Group represents a rare combination of quality, value, safety, and growth potential. The company’s industry-leading fundamentals and competitive position, combined with its current 50% discount to intrinsic value, create a compelling investment opportunity for long-term oriented investors.

For retail investors seeking a cornerstone holding in healthcare, UNH offers the potential for compelling risk-adjusted returns with downside protection from strong fundamentals and growing dividend income. At current prices, UNH is an Ultra Value Buy suitable for investors willing to look past temporary headwinds to capture exceptional long-term value.

The bottom line is simple: opportunities to buy world-class companies at 50% discounts don’t come along often. When they do, history suggests that patient investors are typically rewarded handsomely for their conviction.

Important Disclaimers

This analysis is for educational purposes only and does not constitute investment advice. Past performance does not guarantee future results. Please consult with a qualified financial advisor before making investment decisions. The author may hold positions in securities mentioned.

About Vulcan-Stock.com: Providing data-driven investment analysis for retail investors through comprehensive fundamental and technical research.

Leave a comment