Reddit (RDDT) dropped 50% from its 52-week high while the business posted 69% full-year revenue growth, turned $530 million in net income, and generated $684 million in free cash flow. The stock is broken. The company is not. That gap is where the opportunity lives, and I think staged buying between $125 and $160 offers one of the better asymmetric setups in internet advertising right now.

The Setup Nobody Wants to Talk About

Something unusual happened to (RDDT) between October 2025 and March 2026. The company executed one of the cleanest monetization ramps in recent internet history, and the market responded by cutting the stock in half.

Q4 2025 revenue hit $726 million, up 70% year over year. Daily active uniques grew 19% to 121.4 million. Full-year revenue cleared $2.2 billion. Net income for the year came in at $530 million. Free cash flow reached $684 million. The company exited the year with $2.477 billion in cash, equivalents, and marketable securities, zero meaningful debt, and announced a $1 billion share repurchase authorization.

And the stock responded by falling from $283 to $136.

That is the kind of disconnect I build positions around. Not because the bears are wrong about the risks (they are not), but because the price is now compensating you for those risks in a way it was not six months ago.

What Reddit Actually Became

The old knock on Reddit was that it could never monetize. It was a chaotic collection of forums where advertisers feared brand safety issues and users despised anything that smelled like a sponsored post. That critique aged poorly.

Reddit’s gross margin sits at 91.2%. That is not a typo. It is higher than (META), higher than (GOOGL), higher than almost any ad-supported platform you can name. Operating margin reached 20.1% on a GAAP basis (32% adjusted), and the company is still early in its monetization curve. Active advertisers grew over 75% in Q4 alone, with AI-driven campaign tools accelerating onboarding.

Three engines are working simultaneously. The core advertising business keeps scaling, with Q1 2026 guidance of $595 million to $605 million in revenue and $210 million to $220 million in adjusted EBITDA, both above consensus at the time of the guide. The data licensing layer (partnerships with companies training AI models) adds a second revenue stream that barely existed 18 months ago. And on March 24, the company unveiled expanded shopping tools, including Collection Ads, community deal overlays, and an alpha Shopify integration that simplifies catalog and pixel setup for merchants.

That last piece matters more than it looks. Reddit reported a 40% year-over-year increase in high-intent shopping conversations, and its Dynamic Product Ads drove 91% higher return on ad spend year over year in Q4 2025. Commerce is the next monetization frontier, and management is building the plumbing now.

Why the Stock Collapsed Anyway

If the business is this good, why is (RDDT) trading at half its October level? Three forces converged.

First, multiple compression. Reddit came public riding a wave of AI hype and meme-stock nostalgia. The market gave it a blended P/E north of 60x at the peak. When rate-cut expectations got pushed further out and the macro tape weakened in early 2026, high-multiple internet names got repriced aggressively. (RDDT) was one of the most expensive, so it got hit the hardest.

Second, insider selling created optics problems. CEO Steve Huffman sold shares in late February. The COO sold $5.6 million worth. The CTO sold too. None of those sales were unusual for a recently-IPO’d company with executives holding concentrated positions, but on a weak tape, the headlines land harder.

Third, a UK regulatory fine added noise. The UK’s Information Commissioner’s Office fined Reddit about $19.5 million for failing to protect children’s personal data. Reddit is appealing, calling the demand to collect more user identity data “counterintuitive.” The fine itself is financially immaterial, roughly 0.9% of trailing revenue, but it feeds a narrative about regulatory exposure that spooks momentum-sensitive holders.

The Anthropic lawsuit adds another headline. Reddit sued Anthropic last June over alleged unauthorized scraping of user content for AI training. A federal judge tentatively ruled on March 20 that the case should return to California state court. The lawsuit is early-stage and the financial outcome is uncertain, but it reinforces Reddit’s leverage over its data assets, which is actually a positive for the long-term monetization thesis.

Where the Valuation Actually Stands

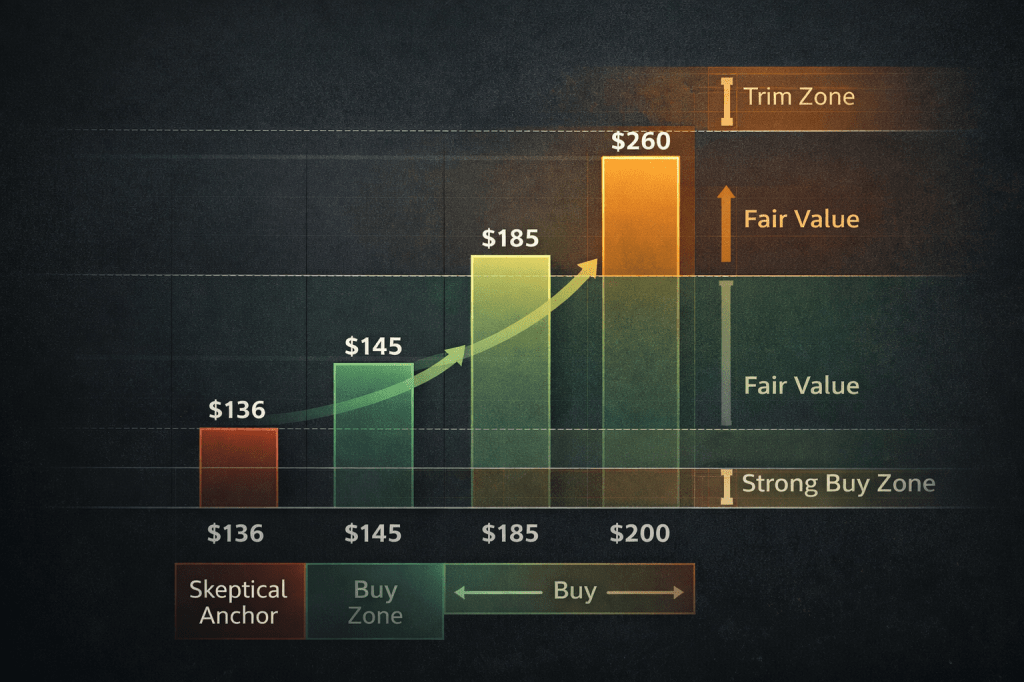

I ran this through several lenses and landed on a blended fair value of roughly $185.

The skeptical anchor comes from conventional relative metrics, which suggest fair value near $133 to $145, roughly around the current price. That framework treats Reddit like an average internet stock. It is not average.

The growth-adjusted anchor is more constructive. If you apply a 30x to 31x multiple to a forward EPS bridge centered on the 2027 earnings path ($5.75 to $5.81 consensus), you get a value in the mid-$170s. That is conservative for a company growing revenue at this pace with these margins.

The Street sits higher still. Analyst consensus target is around $232, and the GNG Research database shows a fair value estimate of $260.53 with a 46.4% discount to that level. I treat those as context, not gospel.

Blending the conservative internal view with the skeptical and optimistic anchors, I land at roughly $185. That gives you about 36% upside from the March 24 close of $136.12, with a margin of safety around 26%.

That is enough for a BUY, but I want to be clear about what it is not: it is not a deep-value Strong Buy. The trend is broken, volatility is extreme, short interest runs in the mid-teens, and too much of the bull case still leans on defending a premium multiple. I need to see the tape improve before upgrading.

The Five Things That Could Kill This

I am buying (RDDT) here, but I refuse to pretend the risks are small. They are real and specific:

1. Ad cycle sensitivity. Reddit generates essentially all its revenue from advertising. If the U.S. economy tips into recession and ad budgets get cut, even 69% topline growth can decelerate fast. Invalidation: quarterly revenue growth below 25% for two consecutive quarters.

2. Multiple compression round two. At 35x forward earnings, (RDDT) is not expensive relative to its growth, but it is not cheap in absolute terms either. If the macro tape keeps deteriorating, another leg down in the multiple could push the stock into the $95 to $110 range. Invalidation: forward P/E sustaining below 20x without a growth reacceleration catalyst.

3. User growth stalls. Reddit’s DAUq growth of 19% is healthy but decelerating from prior quarters. If user growth cools sharply, the monetization story loses its denominator. Invalidation: DAUq growth below 10% year over year.

4. Regulatory escalation. The UK fine was manageable. But if similar enforcement actions multiply across the EU or if content moderation costs spike, margins could erode. Reddit’s appeal of the UK fine signals the company will fight, but the regulatory direction globally is toward tighter platform oversight.

5. Data licensing dependency. Reddit has AI training data deals that contribute to revenue. If the legal and political environment turns hostile to web-scraping-based AI training (see the Anthropic lawsuit), those deals could become harder to negotiate or renew.

How I Am Playing It

Rating: BUY, staged entry

At $136.12, (RDDT) sits inside my buy zone of $135 to $160. The strong buy zone is $125 to $135.

My execution plan: first tranche here around $135 to $140. Add more aggressively on any panic into $125 to $135. If the stock reclaims and holds the 200-day moving average (currently around $191), I can add on confirmation, but I would rather start with price weakness than chase strength in a name this volatile.

Trim logic: begin de-risking in the $190 to $205 range if fundamentals are merely intact and the move is mostly multiple expansion. More aggressive trim above $220 unless earnings revisions have moved materially higher.

Invalidation framework: I would downgrade the thesis if we see a sequence of DAUq growth cooling sharply, revenue guidance slipping below Street expectations, ad tool and commerce rollout failing to translate into monetization, and margin expansion rolling over. Any two of those four in combination would push me to Hold or Sell.

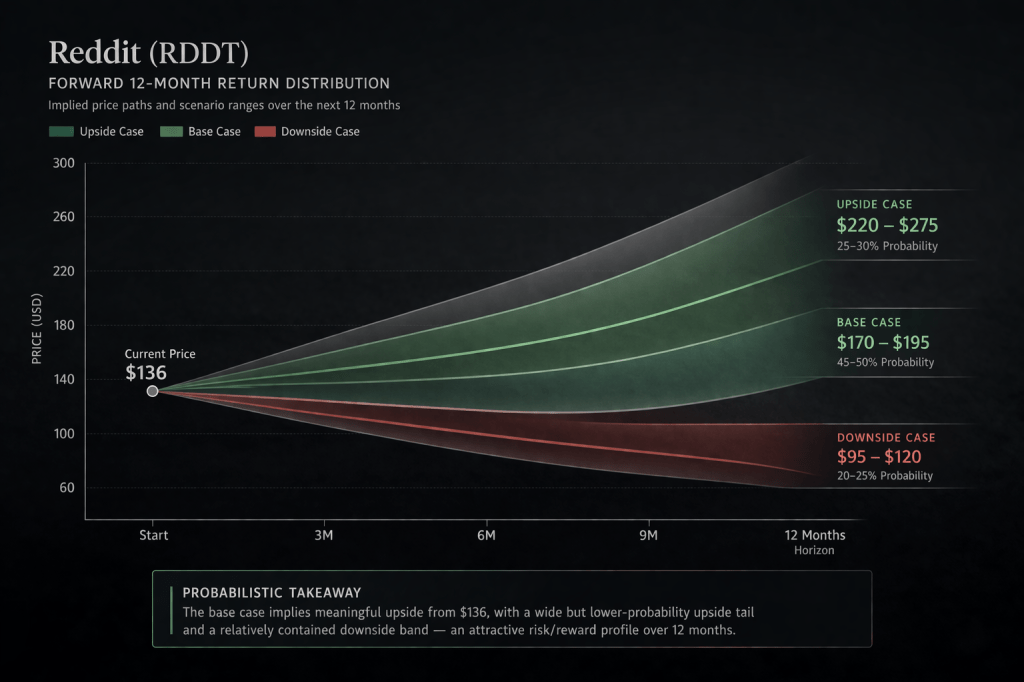

Forward Return Bands

Based on the current price anchor, valuation work, and the stock’s realized volatility profile:

Downside (roughly 20th percentile): $95 to $120. Total return around negative 12% to negative 30%. This is the world where ad growth decelerates hard, the multiple compresses again, and the tape stays hostile.

Base case (roughly 50th percentile): $170 to $195. Total return around 25% to 43%. Execution stays solid, Q1 guidance is met or beaten, and the market gives a still-premium but less manic valuation.

Upside (roughly 80th percentile): $220 to $275. Total return around 62% to 102%. Commerce, AI ad tools, and data licensing all keep working, and the market decides the de-rating went too far.

My positioning targets the base case. If the upside case materializes, that is a bonus, but I refuse to size positions off moonshot scenarios.

Master Metrics Table

| Metric | Value | Context |

|---|---|---|

| Price anchor | $136.12 | March 24, 2026 close |

| Blended fair value | ~$185 | Vulcan internal estimate |

| Upside to FV | ~36% | BUY-worthy asymmetry |

| Revenue growth FY2025 | 69% | Exceptional topline expansion |

| Q4 revenue | $726M | 70% year-over-year growth |

| Q4 DAUq | 121.4M | 19% year-over-year growth |

| Gross margin | 91.2% | Best-in-class economics |

| Net margin | 24.1% | Real profitability |

| FCF FY2025 | $684M | Strong cash generation |

| Cash and securities | $2.477B | Net cash balance sheet |

| Debt / Equity | 0.0 | Zero leverage |

| Forward P/E | ~35x | Premium but supported by growth |

| Altman Z-Score | 56.7 | Extreme financial safety |

| Piotroski F-Score | 6-7 | Healthy fundamentals |

| Short interest | ~14% | Elevated, can amplify moves |

| Price vs 200d MA | -27% | Trend broken, not repaired |

| Max drawdown 1Y | -52% to -68% | Very high volatility stock |

| Analyst target | ~$232 | Street still constructive |

| Buyback authorization | $1B | Capital return support |

| Q1 2026 revenue guide | $595M-$605M | Above consensus |

The Bottom Line

(RDDT) is a damaged stock sitting on top of a still-improving business. That combination is where I have historically found my best entry points, across every sector and market cycle. The business proved itself in 2025. The question now is whether the market will pay for that proof again, and at what price the risk/reward favors the buyer.

At $136, I think it does. Not overwhelmingly, not without real downside scenarios, but enough to start building a position. Buy in stages, respect the volatility, and let the fundamentals do the work over 12 months.

Disclosure: This analysis is for educational purposes and reflects the author’s personal research process. It is not personalized investment advice. Do your own due diligence before making investment decisions. The author may hold or initiate a position in (RDDT).

Leave a comment