By GNG Research / Vulcan-mk5 | March 2026

There is a particular kind of frustration that only value investors understand. You watch a great business get repriced violently lower, your screen lights up green across every fundamental metric, and yet the stock keeps falling. The tape is relentless. The narrative is brutal. Every instinct trained by years of momentum-chasing whispers to wait, to let it bottom, to find something cleaner.

That frustration is exactly where Accenture (ACN) sits right now, and I think it is wrong to wait.

The stock has fallen roughly 35% from its highs. It is trading at valuations not seen since consulting budgets were being slashed in a rate-shock environment that no longer applies. And underneath the wreckage of price momentum sits one of the most consistently profitable, cash-generative enterprises in global technology services: a business with a 95th-percentile cash flow predictability score and a 100th-percentile EPS predictability score across the Vulcan universe of 5,000+ tickers.

That is not a coincidence. That is the fingerprint of a toll collector.

What Accenture Actually Does, and Why It Matters Now

Think of the world’s largest corporations as cities. Every time they need to modernize their infrastructure, train their workforce on new technology, redesign their supply chains, or stand up an AI capability, they hire a construction crew. Accenture is the construction crew. The largest one on earth.

With $70.7 billion in annual revenue and operations spanning every major market and vertical, ACN does not merely consult. It executes. It embeds thousands of specialists inside client organizations for multi-year engagements, collects predictable managed services fees, and then resells those same capabilities across its next fifty engagements. The business model is designed to compound knowledge into margin at scale, and over the last five years, it has done exactly that, growing revenue at a 9.1% compound rate.

The bear argument right now is that this model is slowing. Federal government contract exposure has created headline risk. Consulting budgets are softer. The AI transition might displace some of what ACN does.

Each of those concerns is real. None of them is new. And none of them changes the math at $213.

The Valuation Disconnect That Changes Everything

Here is the tension I keep returning to: Accenture is priced like a no-growth utility, but it keeps performing like a growth compounder.

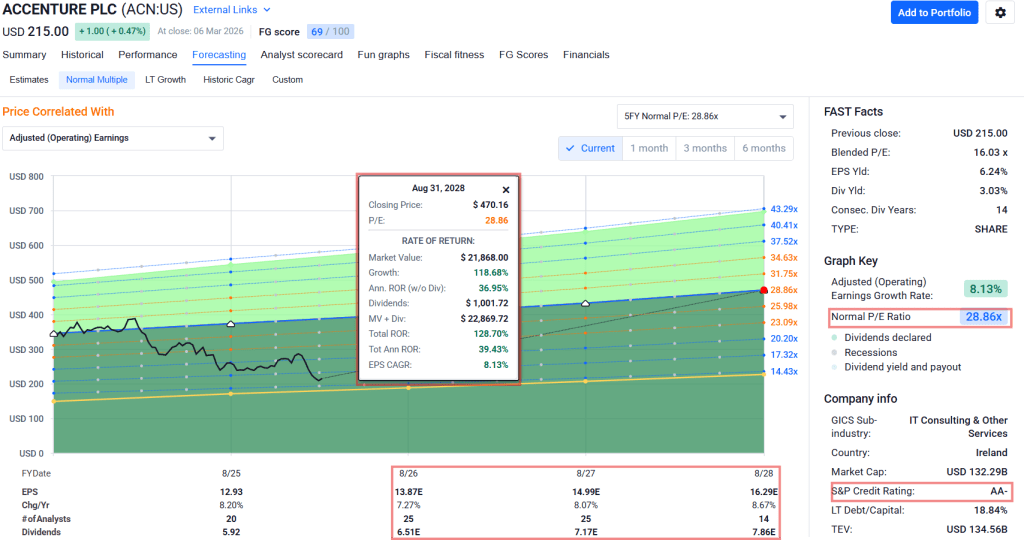

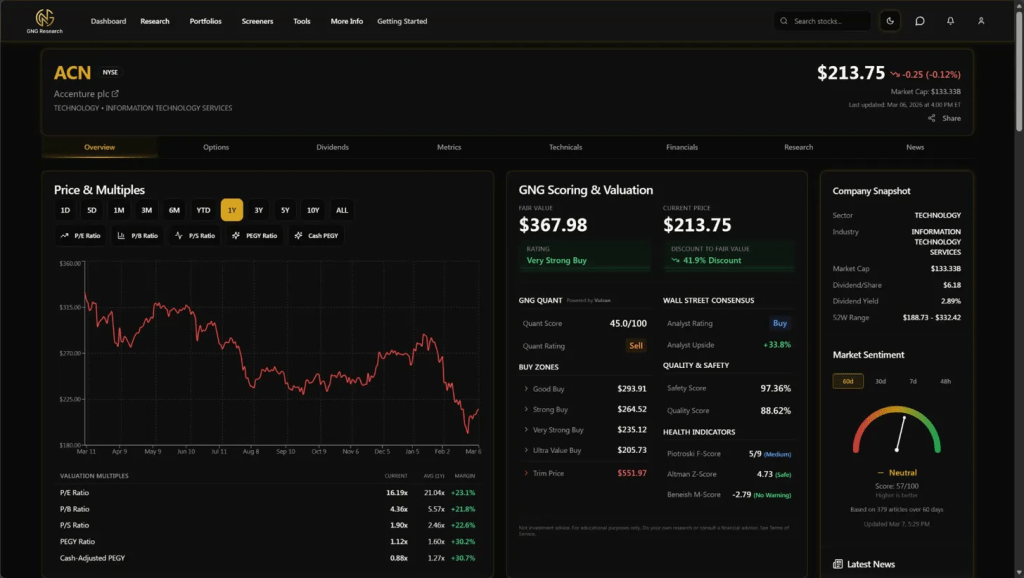

The Vulcan framework’s blended fair value for ACN lands at $292, derived from a conservative weighting of multiple methods: a Greenwald earnings power value floor, a discounted cash flow model anchored to actual free cash flow generation, and Street consensus targets. At the current price around $213, the stock is sitting at a 27% discount to that figure. That is not a small margin of safety number on a mediocre business. That is a significant discount on a franchise with a Quality Score of 94 out of 100 and a Safety Score of 97.36.

The forward P/E is 14.4x. The EV to forward EBITDA is 9.4x. These are the multiples you assign to a business you believe will stagnate for the next five years. But the analyst consensus for next year’s EPS is $14.94 on a current price of $213, which implies the market is giving you roughly 14x earnings on a business that has compounded EPS for a decade.

The Chowder Rule result, which combines the forward dividend yield with the five-year dividend growth rate, comes to 16.2%. The threshold I use for quality dividend compounders is 15%. ACN clears it while carrying a debt-to-equity ratio of 0.3, an interest coverage ratio of 40x, and an Altman Z-Score of 4.7, well above the distress zone.

The Counter-Intuitive Case: AI Is Not the Threat Here

The conventional read on AI’s impact on IT consulting firms is essentially: automation replaces consultants, demand contracts, margins compress. It is an intellectually tidy narrative and almost certainly wrong for ACN specifically.

Consider what Accenture actually reported for fiscal year 2025: generative AI bookings nearly doubled to $5.9 billion, and generative AI revenue tripled to $2.7 billion. This is not a company losing AI business to the machines. This is the company being hired to implement AI for everyone else.

The demand signal from Q1 FY2026 reinforces this. Revenue came in at $18.74 billion, up 6% in USD, with total new bookings of $20.94 billion. Consulting bookings reached $9.88 billion and managed services bookings hit $11.06 billion. Management reiterated full-year revenue growth guidance of 2% to 5% in local currency and adjusted EPS guidance of $13.52 to $13.90.

This is not the reporting of a franchise under structural pressure. This is a franchise in a digestion phase, one where the market has decided that a modest guidance range justifies stripping 35% from the price.

The toll collector metaphor applies directly here: every enterprise that needs to wire AI into its operations has to pay someone to do it. The bigger and more complex the organization, the more they need ACN specifically, because ACN is the only firm with the scale, the global delivery infrastructure, and the pre-built AI capability frameworks to execute at the Fortune 500 level. That is a structural moat, not a feature that gets disrupted.

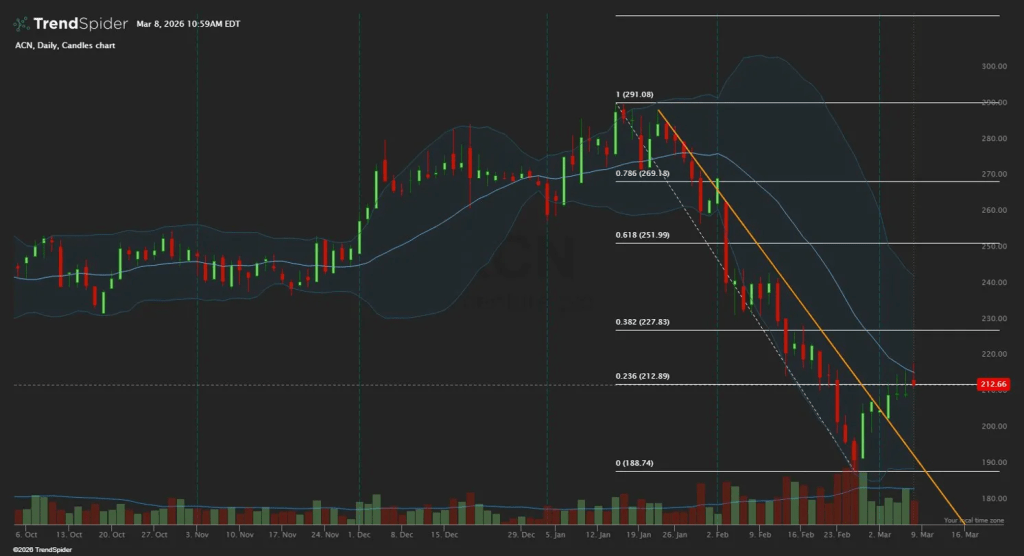

The Chart: What the Tape Is Actually Saying

The Technical daily chart introduced earlier tells a specific technical story. ACN peaked at $291.08 in early January 2026 and has been in an aggressive downtrend since. The price recently undercut the 0.382 Fibonacci retracement at $227.83 and is currently testing the 0.236 level at $212.89. The 1-year max drawdown is 42.8%, and the slope of the orange descending channel is still pointed lower.

Two things are true simultaneously: the tape is weak, and the valuation is compelling.

For a systematic investor, this is the core tension. Momentum signals say wait. Value signals say act. My resolution to that tension is position sizing: I do not need the tape to reverse to build a position, I need the valuation to be real and the business to not be broken. On both counts, ACN passes.

The Piotroski F-Score of 5 out of 9 is medium, not excellent, which acknowledges that the recent price compression and soft earnings momentum are real signals, not noise. I am not pretending the business is in pristine shape. But a Piotroski of 5 on a franchise with 20.2% ROIC and 40x interest coverage is the signature of a cyclically pressured quality business, not a deteriorating one.

Five Specific Risks Worth Naming

I will not paper over these. Each represents a scenario where the thesis fails.

First, federal government exposure. If the DOGE-related budget pressures expand into a sustained, multi-year freeze on federal IT consulting contracts, ACN’s federal segment revenue could see meaningful deterioration. That revenue line has been a source of market anxiety throughout this drawdown.

Second, a prolonged consulting slowdown. If corporate IT budgets stay constrained into 2027, the 2% to 5% revenue guidance could prove optimistic. A revenue miss combined with margin compression would pressure the multiple even at current low valuations.

Third, currency headwinds. ACN derives a significant portion of its revenue outside the United States. A strong USD environment compresses reported revenue growth, and the 6% USD growth versus 5% local currency growth in Q1 FY26 illustrates this drag. If the dollar strengthens further, the headline numbers will disappoint even if underlying demand holds.

Fourth, AI disruption risk from below. While ACN is capturing AI-enabled bookings today, there is a legitimate scenario where second-tier technology firms and specialized AI implementation boutiques erode ACN’s pricing power in lower-complexity engagements over a 3 to 5 year horizon.

Fifth, valuation compression staying persistent. The market does not have to re-rate ACN toward fair value on any particular timeline. A stock can trade cheap for extended periods. The $204 ultra-value zone exists precisely because a further 5% to 10% decline is well within the range of possibilities before momentum stabilizes.

My Execution Strategy

I approach this with tranche-based sizing, not a single entry.

The current zone around $213 to $219 is what the Vulcan framework classifies as Very Strong, which means the discount to blended fair value is above 20% and the quality and safety checks pass. This is a zone where I build a starter position, sized at roughly half of my intended full allocation.

If the stock continues lower toward $204 and below, that is the ultra-value zone where I complete the position. The combination of a 16.2% Chowder score, 3.0% forward yield, 20.2% ROIC, and 100th-percentile EPS predictability makes me comfortable adding at that level with conviction.

My buy zone ceiling is $263, which is roughly 90% of the blended fair value, where the margin of safety begins to compress below my comfort threshold.

Position size for this type of high-quality, moderate-yield compounder: 1% to 2% of portfolio. It sits comfortably in the barbell alongside higher-growth positions, contributing income yield and stability rather than explosive upside.

Invalidation trigger: two consecutive quarters of declining bookings combined with a guidance cut below 2% revenue growth for FY26. That would signal demand deterioration beyond a digestion phase and would require re-evaluating the thesis.

The 12-month base case return from current levels, if the stock re-rates toward the $292 blended fair value, is approximately 37% including dividends. The downside case, if business fundamentals deteriorate and the multiple compresses further, is approximately 5% to 8% loss. That asymmetry is why this is a Strong Buy at $213.

Master Metrics

| Metric | Value |

|---|---|

| Ticker | ACN |

| Company | Accenture plc |

| Sector | Technology / IT Services |

| Quality Score | 94 / 100 |

| Safety Score | 97.36% |

| Value Score | 92 / 100 |

| Growth Score | 87 / 100 |

| Vulcan Blended Fair Value | $292 |

| GNG Fair Value | $367.98 |

| SR Fair Value | $285.41 |

| Margin of Safety (vs. $292) | ~27% |

| Forward P/E | 14.4x |

| EV / Forward EBITDA | 9.4x |

| ROIC | 20.2% |

| Return on Equity | 24.7% |

| Return on Assets | 12.3% |

| FCF Per Share | $18.26 |

| FCF as % of Sales | 16.3% |

| Net Margin | 10.8% |

| Operating Margin | 14.8% |

| Gross Margin | 32.0% |

| Debt / Equity | 0.3 |

| Interest Coverage | 40.0x |

| Altman Z-Score | 4.7 (Safe) |

| Piotroski F-Score | 5 / 9 (Medium) |

| Beneish M-Score | -2.67 (No Warning) |

| TTM Yield | 2.9% |

| Forward Yield | 3.0% |

| Div. 5Y Avg Growth | 13.1% |

| Chowder Rule (5Y) | 16.2% |

| Buyback Yield | 3.6% |

| Total Cash Return | 9.0% |

| EPS Predictability Pctl. | 100th |

| Cash Flow Predictability Pctl. | 95th |

| 5Y EPS Growth Est. | 8.8% |

| Avg. EPS Est. Next Y. | $14.94 |

| Sales (TTM) | $70.7B |

| Revenue Growth (5Y Avg) | 9.1% |

| Beta (3Y) | 0.81 |

| 1Y Max Drawdown | -42.8% |

| Institutional Ownership | 82.7% |

| Buy Zone (Very Strong) | $213 to $219 |

| Buy Zone Ceiling | $263 |

| Ultra Value Zone | $204 and below |

| Invalidation Trigger | 2 qtrs declining bookings + guidance cut |

This narrative is for informational and educational purposes only. Not investment advice. Always do your own research. The author may hold positions in securities mentioned. Data sourced from GNG Research, Vulcan SR, and public company filings.

Leave a comment