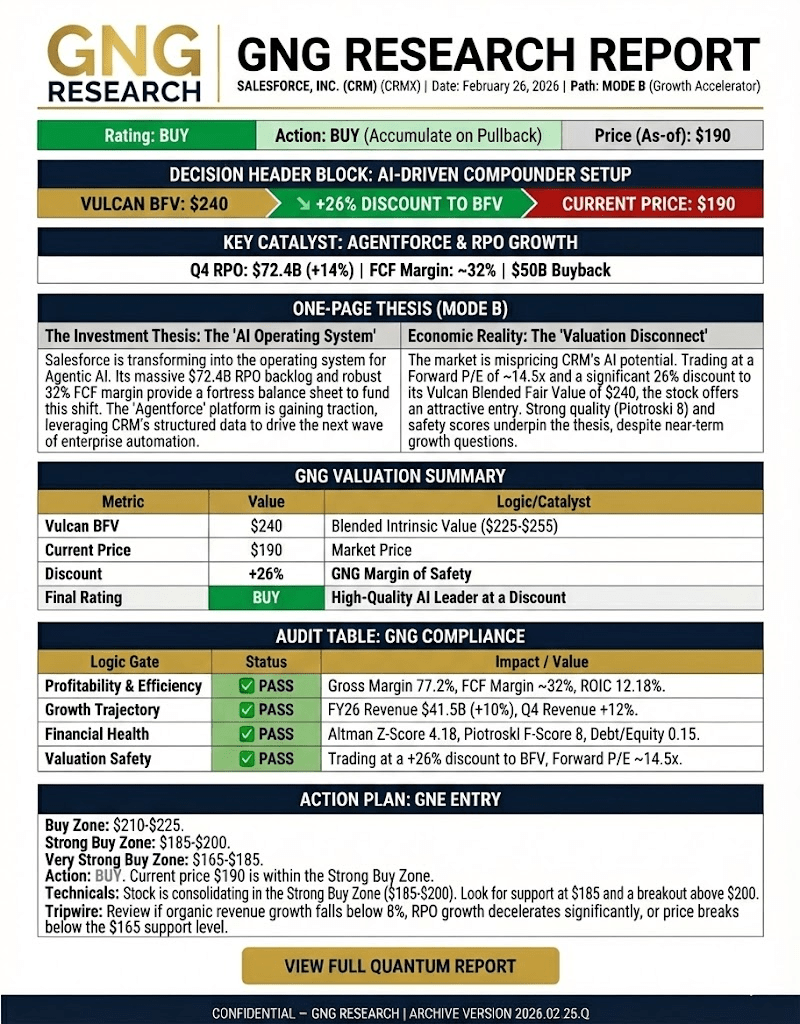

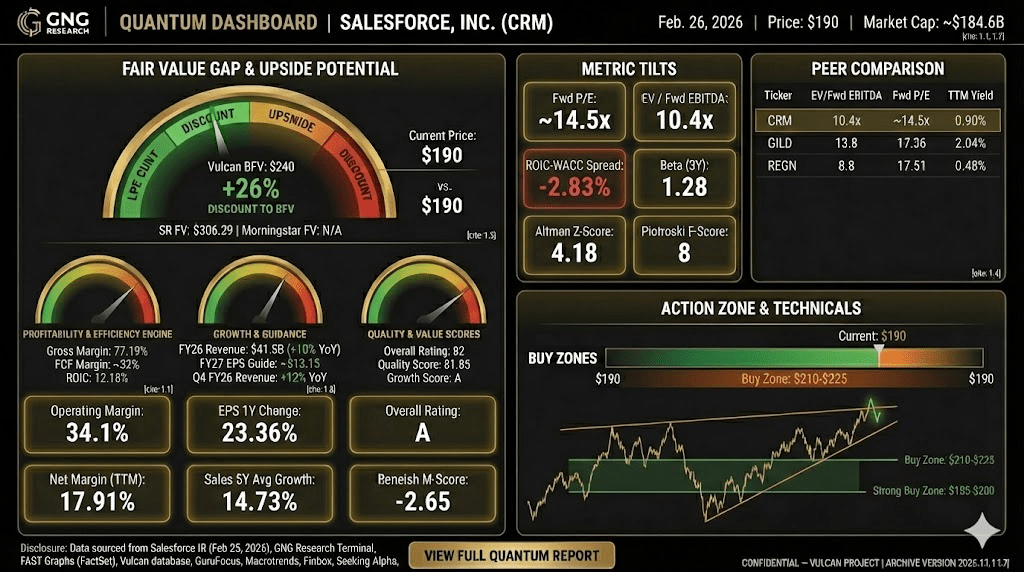

Ticker: CRM | Sector: Technology / Software – Application | Rating: BUY | 12-Month Target: $240

As-of date: February 25, 2026 (post Q4 FY26 earnings)

Bull / Base / Bear: $300 / $240 / $200

The Disconnect Nobody’s Talking About

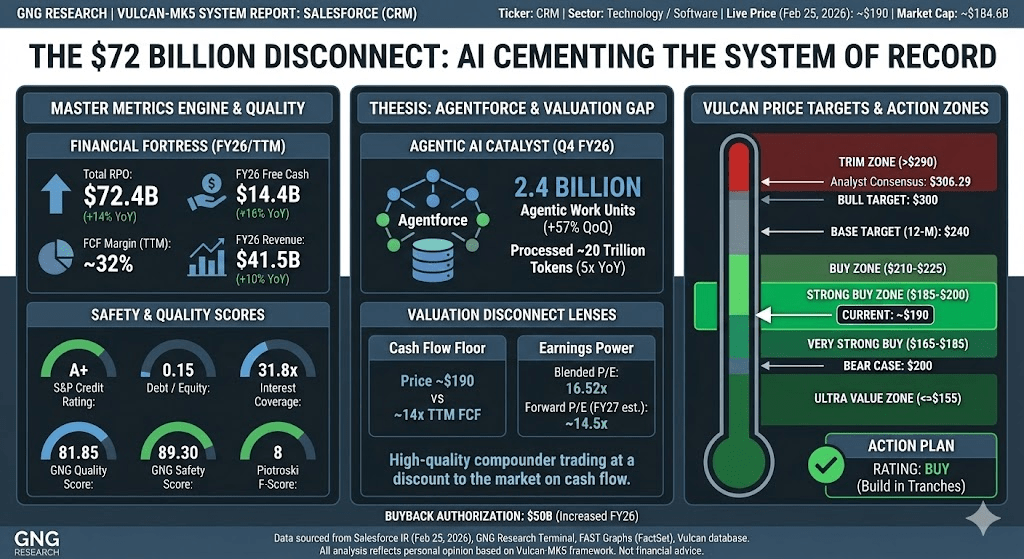

Salesforce just printed $72 billion in remaining performance obligations, up 14% year over year, and the stock is sitting near its 52-week low. Let that sink in for a moment. Seventy-two billion dollars worth of signed commitments from the world’s largest enterprises, and the market is pricing CRM like a company whose best days are behind it.

I’ve been running this through the Vulcan screening system for weeks now, and the signal keeps getting louder: this is a high-quality business being sold at a mid-teens multiple while generating north of $14 billion in annual free cash flow. The gap between what the numbers say and what the stock price implies is wide enough to drive a truck through, and that’s exactly the kind of setup our framework was built to find.

Here’s the counterintuitive part. The market isn’t wrong that Salesforce faces real questions about AI disruption and growth deceleration. It’s wrong about the magnitude of those risks relative to the cash flow engine sitting underneath the stock. This is the investing equivalent of refusing to buy a rental property because you’re worried about paint colors while ignoring that it’s generating 32 cents of free cash on every dollar of revenue.

What Salesforce Actually Is (And Why That Matters More Than Ever)

Think of Salesforce (CRM) as the nervous system of the modern corporation. Every customer interaction, every sales pipeline, every service ticket, every marketing campaign flows through this platform for more than 150,000 companies worldwide. That’s not an app you can rip out and replace on a Tuesday afternoon. It’s the connective tissue that holds commercial operations together.

The Q4 FY26 earnings report, released today, confirmed exactly what the backlog has been whispering: this platform is getting stickier, not weaker. Revenue hit $11.2 billion for the quarter, up 12% year over year. Full year revenue came in at $41.5 billion. Non-GAAP operating margins held at 34.1% for the fiscal year. And the company generated $14.4 billion in free cash flow, up 16% from last year.

But the real story isn’t the backward-looking numbers. It’s the forward-looking architecture.

Agentforce: From Buzzword to Business Line

The “AI kills CRM” narrative has been loud on FinTwit for over a year now. The thesis goes something like this: autonomous AI agents will handle customer interactions directly, bypassing the CRM application layer entirely. It’s a clean narrative. It’s also mostly wrong.

Salesforce reported 2.4 billion Agentic Work Units delivered across its platform, growing 57% quarter over quarter. They’ve processed nearly 20 trillion tokens to date, up 5x year over year. More than 60% of Agentforce bookings in Q4 came from existing customer expansions, not new logos chasing a demo. Production accounts increased nearly 50% sequentially.

Here’s why this matters for the “AI replaces CRM” bears: agentic AI doesn’t work in a vacuum. It needs structured data, enterprise permissions, workflow governance, and audit trails. All of that lives inside Salesforce. The more autonomous agents a company deploys, the more critical the system of record becomes, the same way self-driving cars make road infrastructure more important, not less.

Salesforce isn’t being disrupted by AI. It’s becoming the operating system that AI agents run on top of. That’s a fundamentally different trajectory than what the market is pricing.

The Valuation Math That Should Bother You

Let me walk through three valuation lenses, because I don’t trust any single approach.

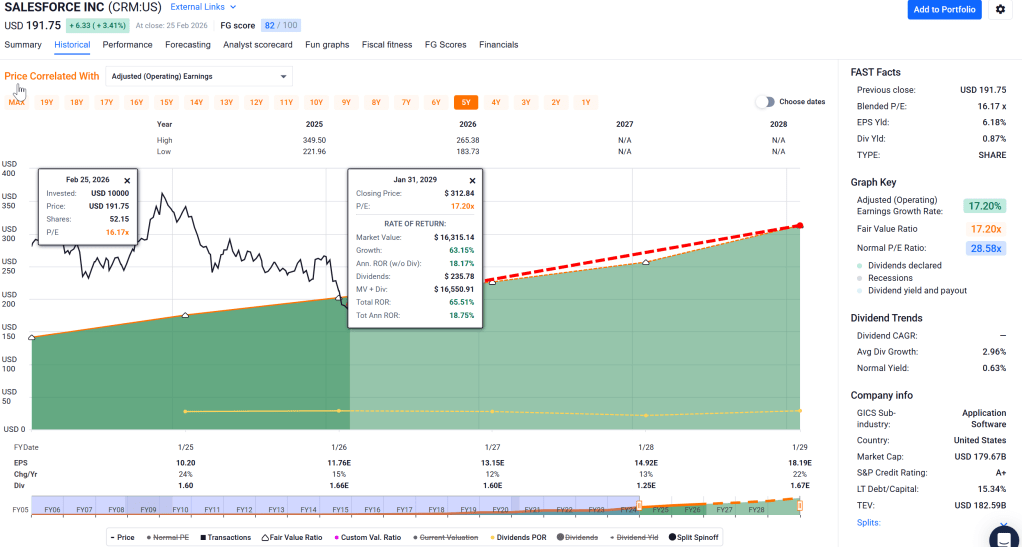

Lens 1: Cash flow floor. At roughly $190 per share, CRM trades at approximately 14x trailing free cash flow. For context, the S&P 500 trades around 22x-24x earnings. A company growing revenue at 10-12% with 32% FCF margins and an A+ credit rating shouldn’t trade at a discount to the broad market on a cash flow basis. The FCF yield here is nearly 7%. That’s a cushion.

Lens 2: Earnings power multiple. FY27 guidance implies non-GAAP EPS of roughly $13.15 at the midpoint. At the current blended P/E of 16.5x (confirmed by FactSet), the stock is pricing in essentially zero multiple expansion. If confidence normalizes even modestly, say to 18.5x forward earnings, you get $243. That’s my base case: $240 requires only a slight improvement in sentiment, not a heroic revaluation.

Lens 3: Relative sanity check. Analyst consensus target is $306, implying roughly 60% upside. I’m not underwriting that as a base case. But the Street having 36 Buy ratings against 13 Holds and only 1 Sell tells you the fundamental community isn’t worried about existential risk. Our base sits well below consensus, which I think makes it more credible, not less.

The Balance Sheet Is a Fortress (And That Matters in This Tape)

In a market where leverage is starting to bite weaker names, Salesforce’s balance sheet reads like a credit analyst’s comfort blanket. Debt to equity sits at just 0.15. Net debt to EBITDA is essentially zero at 0.03. Interest coverage is north of 31x. Altman Z-Score registers 4.18 on our GNG data and 5.29 on FactSet’s calculation, both firmly in the “safe” zone. S&P rates them A+.

This matters because it means the downside scenario is multiple compression, not financial distress. If the stock drops to $175 because sentiment stays sour, Salesforce keeps generating $14 billion in cash and buying back stock. Management just raised the repurchase authorization to $50 billion. They returned $14.3 billion to shareholders in FY26 alone, including $12.7 billion in buybacks. At a depressed valuation, those buybacks become enormously accretive.

Five Risks I’m Watching (With Specific Triggers)

I’m not going to pretend this is a layup. Here’s what could go wrong, with the numbers that would change my mind.

Risk 1: Growth decelerates below 8%. If organic revenue growth (ex-Informatica) slips into high single digits for two consecutive quarters, the market will lock CRM into a “mature software” multiple of 14x-15x forward. That caps upside at roughly $195-200 and the thesis shifts to HOLD.

Risk 2: AI monetization cannibalizes seats. Agentforce needs to be additive ARR, not a replacement for per-seat licensing. If Q1-Q2 FY27 earnings calls reveal flat or declining seat counts without offsetting consumption revenue growth, the economics get murkier fast.

Risk 3: Informatica integration stumbles. The acquisition adds roughly 3 percentage points to FY27 revenue growth. Integration risk is real, as any enterprise software M&A playbook will tell you. Watch for customer churn signals and margin compression in the data integration segment.

Risk 4: Macro tightening compresses multiples further. If 10-year Treasury yields push above 5% again, all duration assets get repriced. Large-cap software multiples are rate-sensitive. CRM at 14x FCF has some cushion, but a broader risk-off move could take it toward $165-175.

Risk 5: Competitive displacement at the margin. Microsoft’s Agent 365 is deployed across 80% of the Fortune 500. ServiceNow’s “Now Assist” just crossed $600 million in ACV. Neither of these is an existential threat to Salesforce’s core CRM, but they’re competing hard for the adjacent agentic workflow budget.

How I’d Play It (Exact Levels)

Action zones:

The current price of roughly $190 sits in the upper half of the Buy zone and right at the Strong Buy threshold ($185-$200). This is a “build in tranches” setup, not a full-size entry.

If you don’t own it: start a 25-33% position here in the $185-$200 range. Add on weakness toward $165-$185 (Very Strong Buy zone). Reserve dry powder for any panic washout toward $155 (Ultra Value).

If you already own it: hold your core position. Don’t trim until at least $290 unless the fundamental triggers above start firing. Re-evaluate at $240-$255 as the base-case target zone approaches.

Position sizing: 1-2% of portfolio maximum for individual stock allocation. This is high conviction on quality, but the near-term volatility (stock is down 37% over the trailing twelve months) demands discipline.

Invalidation trigger: RPO/backlog trends rolling over materially, or two consecutive quarters of guidance stepping down into persistent sub-8% organic growth. Either of those would shift my rating from BUY to HOLD.

The Bottom Line

Salesforce at $190 is a high-quality compounder trading at a discount to the market on every cash flow metric that matters. The AI narrative cutting against it is, in my view, exactly backwards: agentic AI makes the system of record more valuable, not less. The balance sheet provides a floor. The buyback provides compression. The backlog provides visibility.

Is this going to $300 tomorrow? No. The market needs to see Agentforce convert from usage metrics to reported ARR dollars before it re-rates meaningfully. But at 16.5x earnings with 32% FCF margins, an A+ credit rating, and $72 billion in commitments on the books, I think the risk-reward is decisively tilted in the long investor’s favor.

My base case is $240 over the next twelve months. That’s roughly 26% upside plus a small dividend. In a market starved for quality at reasonable prices, that’s a setup worth building into.

Master Metrics Table

| Metric | Value | Source |

|---|---|---|

| Ticker | CRM | — |

| Sector / Industry | Technology / Software – Application | — |

| Market Cap | ~$184.6B | GNG |

| Live Price (Feb 25, 2026) | ~$190 | NYSE |

| FY26 Revenue | $41.5B (+10% YoY) | Salesforce IR |

| Q4 FY26 Revenue | $11.2B (+12% YoY) | Salesforce IR |

| Q4 Non-GAAP EPS | $3.81 (beat $3.05 est.) | Salesforce IR |

| FY26 Non-GAAP Op Margin | 34.1% | Salesforce IR |

| FY26 Free Cash Flow | $14.4B (+16% YoY) | Salesforce IR |

| FCF Margin (TTM) | ~32% | GNG / FAST Graphs |

| Total RPO | $72.4B (+14% YoY) | Salesforce IR |

| Blended P/E | 16.52x | FAST Graphs (FactSet) |

| Forward P/E | ~14.5x (FY27 est.) | GNG |

| FY27 EPS Guide (midpoint) | ~$13.15 | Salesforce IR |

| Debt / Equity | 0.15 | GNG |

| Interest Coverage | 31.8x | GNG |

| Altman Z-Score | 4.18 (GNG) / 5.29 (FactSet) | GNG / FAST Graphs |

| Piotroski F-Score | 8 | GNG |

| S&P Credit Rating | A+ | FAST Graphs |

| Quality Score (GNG) | 81.85 | GNG |

| Safety Score (GNG) | 89.30 | GNG |

| FG Score | 82 / 100 | FAST Graphs |

| Analyst Consensus Target | $306.29 | GNG |

| 12-Month Vulcan Target | $240 (Base) | Vulcan |

| Buy Zone | $210-$225 | Vulcan |

| Strong Buy Zone | $185-$200 | Vulcan |

| Very Strong Buy Zone | $165-$185 | Vulcan |

| Ultra Value Zone | <=$155 | Vulcan |

| Trim Zone | >=$290 | Vulcan |

| Buyback Authorization | $50B (increased FY26) | Salesforce IR |

Disclosure

I may hold positions in securities discussed. This is not financial advice. All analysis reflects personal opinion based on the Vulcan-MK5 screening framework. Do your own due diligence. Data sourced from Salesforce IR (Feb 25, 2026 press release), GNG Research Terminal, FAST Graphs (FactSet), and the Vulcan database.

About the Author

Founding Head of Systems & Strategy at GNG Research. Systematic investor sharing institutional-quality analysis at Vulcan Stock. Follow the framework on X: @VulcanMK5.

Leave a comment