Every decade or so, the market hands you a company printing money at a pace that makes most software businesses look anemic, then panics over something that has nothing to do with the cash register. AppLovin ($APP) just fell nearly 50% from its December highs. The fundamentals? They just posted the strongest quarter in company history.

That disconnect is your signal.

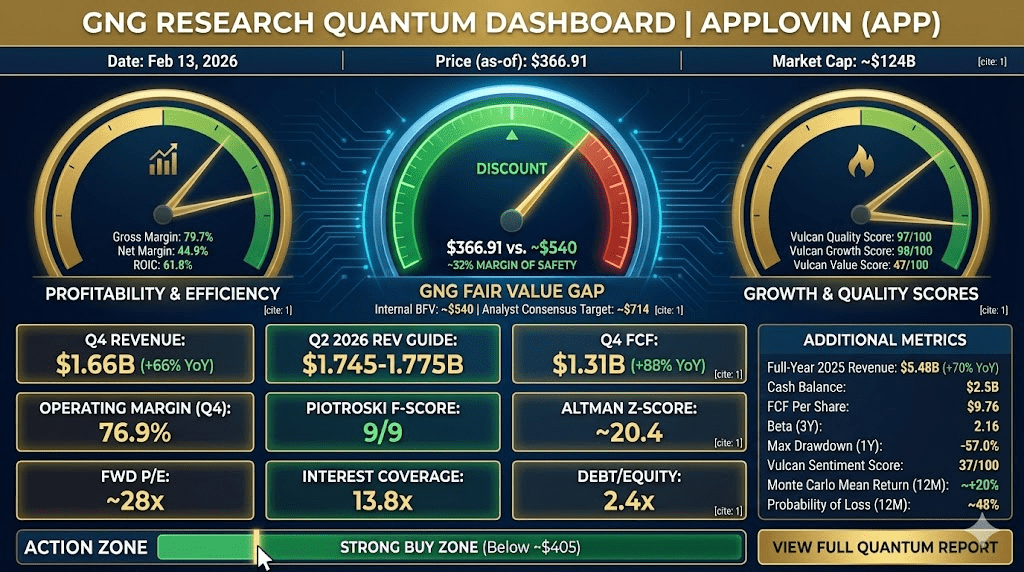

Vulcan-mk5 Rating: STRONG BUY (Staged Entry) Vulcan Composite: Quality 97 | Growth 98 | Value 47 | Sentiment 37 As-of 2/13 Price: $366.91 | Internal BFV: ~$540 | Margin of Safety: ~32%

The Toll Road Hidden Inside Your Phone

Think of AppLovin like a toll road, except the road lives inside every mobile app you have ever downloaded. When a game developer wants paying users, they go to AppLovin’s platform. When a publisher wants to maximize ad revenue, they plug into AppLovin’s MAX auction engine. Every transaction, every auction, every matched ad generates a toll. The more data flows through the system, the smarter the AI gets, the higher the toll collectors’ margins climb.

That is not a metaphor. It is the actual business model. And the toll just got wider.

In Q4 2025, AppLovin reported revenue of $1.66 billion, up 66% year over year. Adjusted EBITDA hit $1.40 billion at an 84% margin, the highest in company history. Free cash flow surged 88% to $1.31 billion. The CFO called their combination of growth and profitability “extraordinarily rare,” and for once, that is not corporate puffery. Their Rule of 40 score clocked in at 150. For context, anything above 40 is considered healthy. Above 100 is elite. 150 is in a category that most software companies never touch.

The engine behind all of this is AXON 2.0, AppLovin’s proprietary AI model that matches advertisers with users in real time. Unlike generic large language models, AXON is narrowly focused on one task: predicting which ad will generate a conversion. That narrow focus is the moat. Every auction run through the system generates training data that makes the next prediction more accurate. It is a compounding flywheel, and competitors cannot replicate it without the same volume of transactional data.

The Numbers That Matter (And Why the Selloff Ignores Them)

Here is what the market seems to have forgotten while panic-selling:

Operating margin expanded from 44.3% to 76.9% in just twelve months. ROIC sits at 61.8%, the kind of number you associate with Visa or Mastercard, not a company most retail investors classify as “ad-tech.” Piotroski F-Score is 9 out of 9, a perfect score on financial health. Interest coverage is 13.8x, meaning AppLovin could service its debt nearly 14 times over with operating income alone. Cash on the balance sheet climbed to $2.5 billion.

The catalyst calendar is stacked. The self-service e-commerce platform, currently in referral-only mode, is scheduled for general availability in the first half of 2026. CEO Adam Foroughi confirmed on the earnings call that existing e-commerce advertisers who lapped Q4 2024 into Q4 2025 “saw material increases in spend as our models just keep getting better.” Q1 2026 revenue guidance of $1.745 to $1.775 billion came in above Wall Street consensus, implying roughly 52% year-over-year growth even after adjusting for the gaming divestiture. And on February 9, short seller CapitalWatch publicly apologized and retracted its negative report, removing an overhang that had contributed to the selloff.

Why the Tape Broke (And Why It Does Not Change the Math)

The 50% drawdown from December highs came from a cocktail of fear, not fundamentals. Google announced Project Genie, an AI initiative that spooked investors worried about competitive disruption to AppLovin’s AXON engine. Anthropic released new productivity tools that triggered a broader software selloff. And the CapitalWatch short report, now retracted, added fuel to an already jittery tape.

None of these events impaired AppLovin’s cash generation. Not one dollar of free cash flow was lost. In fact, the quarter reported during the selloff was the best the company has ever delivered. That is the definition of a “quality compounder meets broken tape” setup.

The bear argument boils down to two real concerns and one phantom. The real ones: high beta (3-year beta of 2.16) means this stock amplifies market moves in both directions, and debt-to-equity at 2.4x looks optically aggressive. The phantom: competition from Google or Meta displacing AXON’s advantage. But here is the counter: AppLovin’s operating margins surged from 44% to 77% in the past year alone while competitors were actively trying to take share. The toll road keeps getting wider, not narrower.

Five Risks You Need to Size Before You Buy

Precision matters when the position could move 20% in a week. Here are the specific risks:

First, multiple compression from macro beta. With a beta above 2, a garden-variety 10% S&P correction could translate to a 20%+ drawdown in APP, regardless of fundamentals. This is not a low-volatility compounder. Size accordingly.

Second, leverage optics under stress. Debt-to-equity of 2.4x is manageable with 13.8x interest coverage today, but a severe ad-spend recession could compress margins enough to make that leverage uncomfortable. Watch quarterly interest coverage as your canary.

Third, estimate revision momentum is mixed. Current-quarter EPS estimates have ticked up slightly, but next-quarter estimates drifted down modestly over the past 30 days. If the revision trend turns persistently negative, the bear probability in the forward distribution rises and your add triggers should move lower.

Fourth, ad-cycle cyclicality. Even the best performance marketing platforms see spending pauses during economic slowdowns. AppLovin’s e-commerce expansion diversifies this risk, but the gaming ad market remains cyclical.

Fifth, key-person risk. Adam Foroughi’s vision has driven the entire transformation from gaming company to AI-powered ad platform. His departure would remove a significant catalyst and deserve an immediate thesis review.

How to Play It: Zones, Tranches, and Invalidation

The Vulcan-mk5 internal blended fair value comes in at approximately $540, which gives you a 32% margin of safety at the current $366.91 price. Analyst consensus targets cluster around $700 to $750, and the GNG model fair value sits near $755. The internal BFV is deliberately conservative because uncertainty is high.

Buy Zones (computed off BFV, HIGH uncertainty regime):

| Zone | Price Level | Action |

|---|---|---|

| Buy | Below $475 | Initiate position |

| Strong Buy | Below $432 | Add to starter |

| Very Strong Buy | Below $391 | Current zone |

| Ultra Value | Below $351 | Aggressive add |

Staged Entry Plan:

Tranche 1 (starter): 25% to 35% of intended position at or near current price. Tranche 2 (add): 25% if price holds between $351 and $391. Tranche 3 (aggressive): remaining 30% to 50% only if price enters Ultra zone below $351 or if upward estimate revisions resume.

Trim triggers: Reduce 10% to 20% as price approaches BFV around $540. Consider heavier trims above $594 (BFV +10%) if the rally lacks revision support.

Invalidation: If quarterly interest coverage drops below 8x, or free cash flow conversion breaks below 60% of net income for two consecutive quarters, the quality thesis weakens materially and BFV needs a downward revision.

Forward Distribution: What Monte Carlo and Bayesian Models Show

Running 10,000 Monte Carlo paths over 12 months with a high-volatility regime (seeded at 42 for reproducibility):

The expected mean total return is approximately +20%, but the spread is enormous. The P10 outcome (downside tail) implies a price around $186, representing a roughly 49% loss. The P50 (median) outcome lands near $377, essentially flat from here. The P90 outcome (upside tail) projects roughly $764, more than doubling your money.

Probability of loss over 12 months: approximately 48%. That is not a typo. This is a high-beta, high-conviction setup where the range of outcomes is deliberately wide.

The Bayesian scenario model assigns 32% probability to a bull case (+75%, multiple re-expansion plus continued execution), 55% to a base case (+25%, partial mean reversion toward BFV), and 13% to a bear case (-35%, macro risk-off combined with ad-spend fears). The probability-weighted expected return is positive, but only if you size for the volatility.

The Bottom Line

AppLovin is not safe. It is mispriced. There is a critical difference. A company generating $1.3 billion in quarterly free cash flow at 84% EBITDA margins, with a Piotroski 9/9 and ROIC above 60%, does not deserve to trade at a 32% discount to even a conservative intrinsic value estimate. But the tape demands respect. Stage your entry. Set your invalidation triggers. And let the cash engine do what cash engines do.

Master Metrics Table

| Metric | Value | Source |

|---|---|---|

| Price (as-of) | $366.91 | Live 2026-02-13 |

| Sector / Industry | Comm. Services / Advertising Agencies | Vulcan DB |

| Market Cap | ~$124B | Computed |

| Quality Score | 97 | Vulcan DB |

| Growth Score | 98 | Vulcan DB |

| Value Score | 47 | Vulcan DB |

| Sentiment Score | 37 | Vulcan DB |

| Piotroski F-Score | 9 | Vulcan DB |

| ROIC | 61.8% | Vulcan DB / SR triangulation |

| Interest Coverage | 13.8x | Vulcan DB |

| Altman Z-Score | ~20.4 (Very High) | Vulcan DB |

| Fwd P/E | ~28x | Vulcan DB |

| Beta (3Y) | 2.16 | Vulcan DB |

| Debt / Equity | 2.4x | Vulcan DB |

| Gross Margin | 79.7% | Vulcan DB |

| Operating Margin | 55.0% (TTM); 76.9% Q4 | Vulcan DB / Earnings |

| Net Margin | 44.9% | Vulcan DB |

| Q4 Revenue | $1.66B (+66% YoY) | Q4 2025 Earnings |

| Q4 Adj. EBITDA | $1.40B (84% margin) | Q4 2025 Earnings |

| Q4 FCF | $1.31B (+88% YoY) | Q4 2025 Earnings |

| Full-Year 2025 Revenue | $5.48B (+70% YoY) | Q4 2025 Earnings |

| Cash Balance | $2.5B | Q4 2025 Earnings |

| Q1 2026 Revenue Guide | $1.745-1.775B | Q4 2025 Earnings |

| FCF Per Share | $9.76 | Vulcan DB |

| Internal BFV | ~$540 | Vulcan-mk5 blend |

| Margin of Safety | ~32% | Computed vs BFV |

| Analyst Consensus Target | ~$714 | Consensus |

| Max Drawdown (1Y) | -57.0% | Vulcan DB |

| Monte Carlo Mean Return (12M) | ~+20% | Vulcan-mk5 (seed 42) |

| Probability of Loss (12M) | ~48% | Vulcan-mk5 |

Leave a comment