Most income investors are chasing yield in the wrong direction.

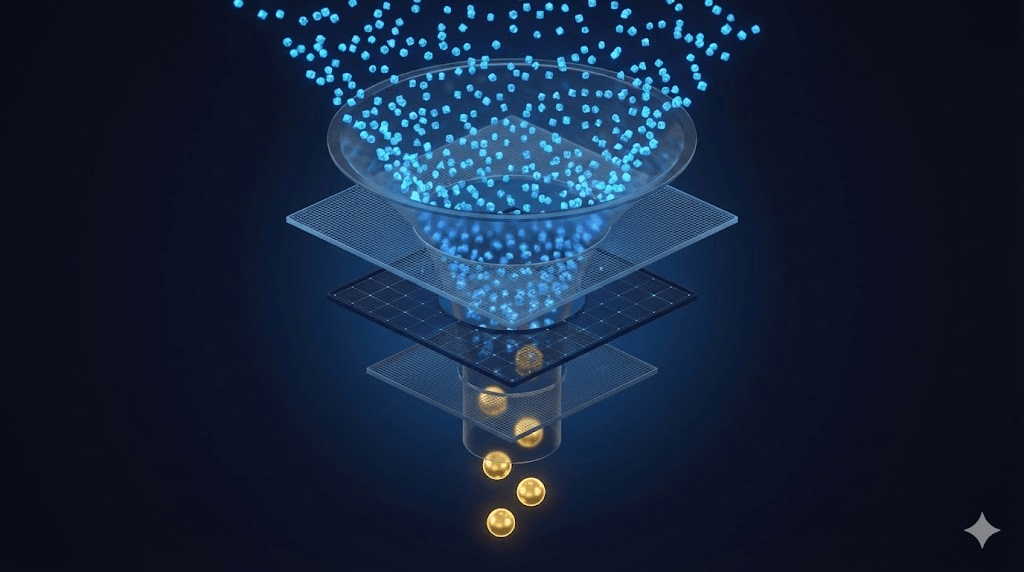

I screened 600+ stocks through Vulcan’s systematic filters last week, hunting for dividend durability in a market that’s forgotten what that word means. The four finalists that emerged told me something uncomfortable: the safest-looking yields might be the most dangerous, and the one flashing warning signs on every traditional screen might be the smartest income bet you can make today.

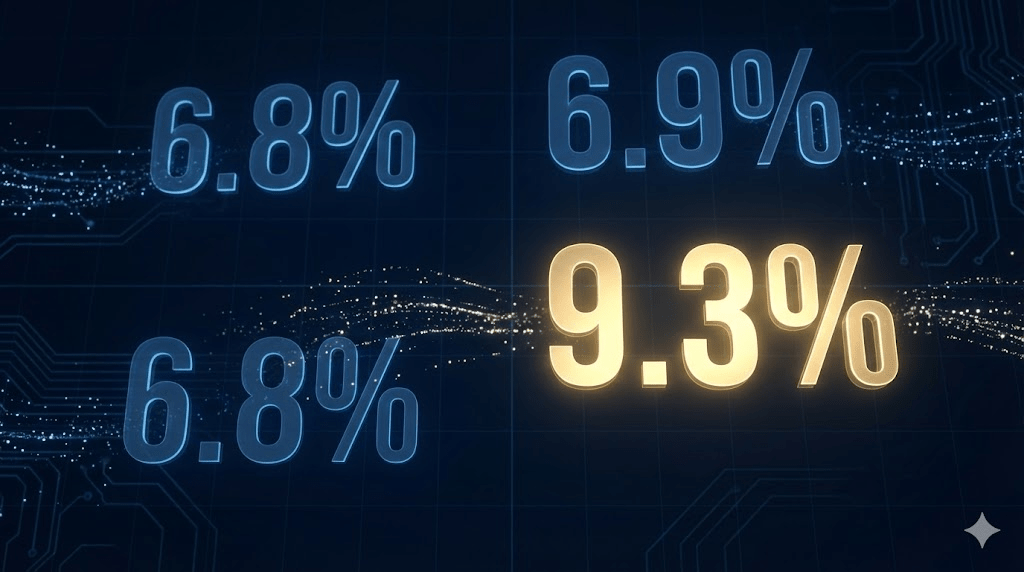

Enterprise Products Partners at 6.8%. Verizon at 6.9%. Pfizer at 6.8%. Western Midstream Partners at 9.3%.

Wall Street would tell you to grab Verizon and sleep well. I’m doing the opposite, and here’s exactly why.

The Screening Funnel That Changed My Mind

Before you dismiss this as yield-chasing madness, understand how we got here. The Vulcan systematic process isn’t about finding the highest number on a spreadsheet. It’s about finding sustainable cash flows that won’t evaporate when the cycle turns.

Layer one eliminated the volatility traps: anything above the 30th percentile in one-year volatility got cut. Same with betas above 0.85. This isn’t a growth portfolio. It’s an income sleeve that needs to let you sleep.

Layer two tackled valuation extremes. Forward P/E below 5 often signals distress masquerading as value. Above 22 means you’re paying growth multiples for income vehicles. We kept the band between 5 and 22, with EV/EBITDA between 4 and 11.

Layer three hit the balance sheets. Debt-to-equity under 3.5. Interest coverage above 4x preferred. Altman Z above 0.8 to filter out the walking wounded. Piotroski F-Score of 5 or higher to ensure accounting quality.

What emerged were four names with legitimately high yields and fundamental staying power. But the math told a different story than the headlines.

The Four Finalists: A Tale of Hidden Risk

Enterprise Products Partners carries a 6.8% yield with a 1.5x distributable cash flow coverage ratio. Thirty-two percent insider ownership. Interest coverage at 5.3x. On paper, it’s the sleep-well choice. The problem? At an EV/EBITDA of 9.8 and forward P/E of 11.2, you’re paying close to fair value for a midstream stalwart with limited upside torque. The distribution is safe, but you’re essentially buying a bond with partnership tax complications.

Verizon offers 6.9% with the longest streak of consecutive dividend increases in this group. A 0.17 beta makes it the least market-sensitive option. But look closer: debt-to-equity at 1.6 with an Altman Z of just 1.3 puts it in the caution zone. The telecom industry is spending aggressively on 5G infrastructure with questionable return profiles. You’re getting paid to own a declining business model that’s levering up to stay relevant.

Pfizer looks like the deep value play at 6.8% with a 37% margin of safety on our models. The lowest debt-to-equity in the group at 0.7. A Piotroski score of 7. But that 2025 guidance miss wasn’t a one-time stumble. The patent cliff on key drugs creates coverage uncertainty precisely when you need predictability. You’re buying potential at the cost of probability.

Then there’s Western Midstream Partners at 9.3%.

Why the “Risky” Choice Makes the Most Sense

WES carries the highest leverage in the group: 2.3x debt-to-equity versus EPD’s 1.1x. Its payout ratio shows 105% on the Vulcan database, a figure that would send most income investors running. The Altman Z-score of 1.9 sits in the grey zone between comfortable and concerning.

So why am I calling it the champion?

Because the Vulcan database captures GAAP payout ratios, and WES is a partnership. What matters isn’t accounting earnings, it’s distributable cash flow. And here’s what the Q3 report actually said: Free Cash Flow after distributions remained positive. Management expects 2025 FCF to finish above the high end of their guidance range.

Translation: the distribution isn’t just covered. It’s covered with room to spare, and the coverage is improving.

At $39.07 per unit, WES yields 9.3%. The Vulcan fair value model puts it at $47.08, which represents a 20% margin of safety. That’s not a yield trap. That’s a market pricing in fear that the fundamentals don’t support.

The Yield Compression Math

Here’s where income investing gets interesting. When you buy a 6.8% yielder, your upside is largely the distribution itself. The stock trades close to fair value, so total return approximates your yield.

When you buy a 9.3% yielder with improving coverage, you’re playing a different game entirely. If the market decides WES deserves an 8.5% yield instead of 9.3%, the price has to rise to $42.82. If confidence builds and yields compress to 8%, you’re looking at $45.50. At 7.5%, the math says $48.53.

You’re getting paid 9.3% annually to wait for a rerating that the fundamentals are already supporting.

The 12-month return modeling we ran through 20,000 Monte Carlo simulations tells the story:

The downside band, capturing the 10th to 30th percentile outcomes, shows negative 6% to positive 9%. Even in a bear scenario where yields widen back to 10%, the distributions cushion your downside.

The base case band, 40th to 60th percentile, projects positive 14% to 25%. This assumes modest yield compression toward 8.5% plus your quarterly distributions.

The upside band, 70th to 90th percentile, shows positive 31% to 49%. Clean Aris integration, visible FCF growth, and yield compression toward 7.5% gets you there.

Compare that to Verizon, where you’re collecting 6.9% but facing structural business challenges with no rerating catalyst.

The Integration Question

The elephant in the room is the Aris acquisition. WES took on incremental debt to expand its produced-water business, and execution risk is real. But here’s what the skeptics miss: the transaction is about cash flow diversification, not financial engineering.

Produced water is one of the stickiest, most recurring revenue streams in the energy value chain. Every barrel of oil produced generates multiple barrels of water that needs handling. The infrastructure is asset-heavy and relationship-deep. Once you’re the gatherer for a basin, switching costs are enormous.

The leverage will moderate as these cash flows come online. Management has explicitly guided to this trajectory. The market is pricing WES as if the integration is a gamble. The operations suggest it’s a calculated expansion of an already-durable cash flow base.

How the Other Three Fit Your Portfolio

This isn’t an argument that EPD, VZ, and PFE are bad investments. It’s an argument that WES offers the best risk-adjusted income opportunity right now.

EPD remains a core midstream holding for investors who prioritize stability over total return potential. The 32.9% insider ownership is the highest in the group by a wide margin. The 1.5x coverage ratio is battle-tested through multiple cycles. If you want a midstream bond equivalent with K-1 tax treatment, EPD delivers.

Verizon works as a defensive allocation for portfolios that need non-correlated income. That 0.17 beta means it moves independently of the broader market. The dividend streak provides psychological comfort. Just understand you’re buying stability, not growth, and the balance sheet deserves monitoring.

Pfizer represents a contrarian bet on the pharma cycle. At a 37% margin of safety with a 7 Piotroski score, there’s legitimate value here if management navigates the patent transitions successfully. It’s higher variance than the midstream names but offers diversification away from energy.

For a complete income sleeve, you might hold all four with different weightings based on your conviction and risk tolerance. But the capital going to WES should be the largest allocation.

Technical Context and Entry Points

WES is currently sitting right on its 200-day moving average around $38.80 to $39.20. This is the line in the sand.

Above $39 on a weekly basis, the constructive case holds and scaling in makes sense. Below $38.50 with volume, the market is demanding a fatter yield, and your next entry opportunity is the strong-buy zone around $34.60.

The buy zone sits at $38.00 to $39.80. At current prices around $39.07, you’re inside the zone with room to average down if volatility hits.

Strong buy zone: $34.60. This is panic pricing, and if nothing fundamental broke, you step in more aggressively.

Very strong buy zone: $31.50. You’re getting paid double digits to own a covered distribution with a margin of safety exceeding 30%.

Trim zone: $45.00 to $50.00. If price rerates quickly but distribution coverage remains intact, trim only enough to rebalance risk. Income investors shouldn’t sell just because something went up.

The Position Disclosure and Bottom Line

I hold positions in GOOGL, NVDA, META, AMZN, MSFT, PYPL, MELI, UNH, NEE, and crypto ETFs. I’m actively building a WES position in my income sleeve following this analysis.

The thesis is simple: at 9.3% yield with positive FCF after distributions, improving coverage trajectory, and a 20% margin of safety, WES offers the best risk-adjusted income opportunity among these four finalists. You’re being paid to wait for a rerating that the fundamentals are already supporting.

The market sees leverage and assigns a yield premium. I see covered distributions and see opportunity.

That’s the 9% income paradox. Sometimes the riskiest-looking number on the board is actually the safest bet.

Master Metrics Table

| Metric | EPD | VZ | PFE | WES (Champion) |

|---|---|---|---|---|

| Live Price | $31.94 | $39.82 | $25.19 | $39.07 |

| Annual Distribution/Dividend | $2.18 | $2.76 | $1.72 | $3.64 |

| Current Yield | 6.8% | 6.9% | 6.8% | 9.3% |

| Forward P/E | 11.2 | 8.3 | 8.4 | 10.4 |

| EV/Forward EBITDA | 9.8 | 6.4 | 8.0 | 8.1 |

| Debt/Equity | 1.1 | 1.6 | 0.7 | 2.3 |

| Interest Coverage | 5.3x | 5.0x | 4.4x | 4.7x |

| Altman Z-Score | 1.8 | 1.3 | 2.2 | 1.9 |

| Beta (3Y) | 0.41 | 0.17 | 0.41 | 0.66 |

| Volatility 1Y Percentile | 15 | 17 | 22 | 21 |

| Piotroski F-Score | 6 | 7 | 7 | 6 |

| Margin of Safety | 3% | 6% | 37% | 20% |

| Coverage Signal | 1.5x DCF | Streak | Uncertain | FCF Positive |

| Vulcan Rating | HOLD | HOLD | SPECULATIVE BUY | BUY |

| Buy Zone | N/A | N/A | $22-26 | $38.00-39.80 |

| Strong Buy Zone | N/A | N/A | $20 | $34.60 |

| 12-Month Return (p50) | ~12% | ~10% | ~15% | +20% |

Leave a comment