When Marvell Technology posted record quarterly revenue of $2.006 billion—a 58% year-over-year surge driven by AI data center demand—the stock promptly tanked 18%. Welcome to semiconductor investing in 2025, where beating expectations isn’t enough if your guidance whispers caution.

But here’s the disconnect that smart money is watching: while Wall Street obsesses over quarterly optics, Marvell just completed a $2.5 billion divestiture that transforms it into a pure-play AI infrastructure company. Sometimes the most important stories unfold in the balance sheet footnotes, not the earnings headlines.

The Pentagon’s Unspoken Infrastructure Problem

Every AI training cluster requires two things most investors never consider: custom silicon that doesn’t exist yet, and optical networking that can handle exponentially growing data flows. NVIDIA gets the headlines, but companies like Marvell build the roads these AI highways run on.

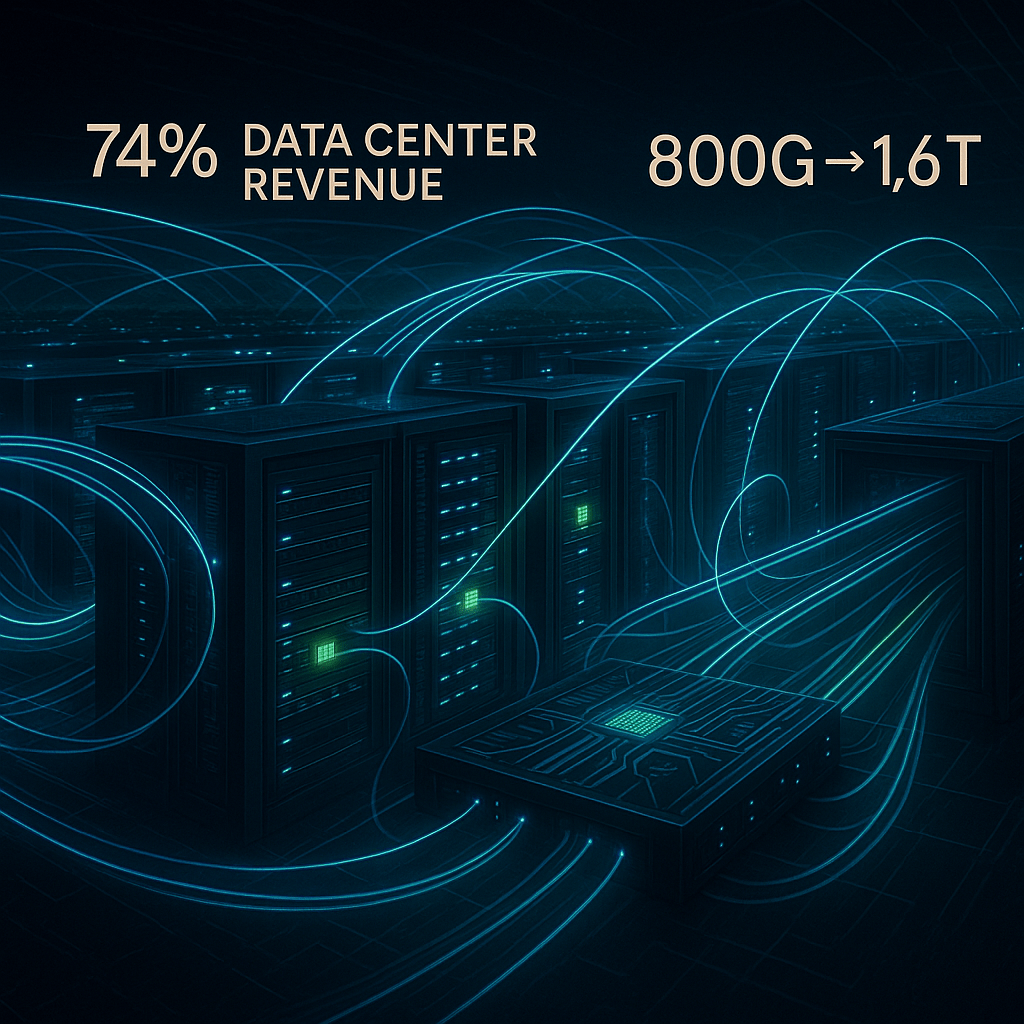

The numbers tell the story: data center revenue now represents 74% of Marvell’s business, up from virtually nothing three years ago. Their electro-optics division ships 800G transceivers today and is sampling 1.6 terabit units—the networking backbone that makes large language models possible. When hyperscalers like Microsoft and Google design their next-generation AI facilities, Marvell’s custom ASICs and optical DSPs aren’t optional components—they’re infrastructure requirements.

Yet the market treated this transformation like a quarterly miss story. At $62.87, MRVL trades at a 60% discount to its 52-week high despite fundamentally stronger positioning than when it peaked at $127.48.

Following the Smart Money Trail

The auto ethernet divestiture completed in August wasn’t just portfolio cleanup—it was strategic focus. Marvell now sits on $2.5 billion in cash with minimal exposure to cyclical automotive markets. Management can accelerate R&D spending, pursue strategic acquisitions, or return capital to shareholders without the distraction of non-core businesses.

Meanwhile, the custom silicon pipeline continues building momentum. These aren’t commodity chip sales—they’re multi-year partnerships with hyperscalers designing proprietary AI accelerators. Each design win represents lifetime value measured in billions, not millions. The Q3 guidance of $2.06 billion may have disappointed traders, but it reflects pipeline maturation rather than demand weakness.

Consider the competitive dynamics: optical DSP technology requires years of development and deep customer relationships. New entrants like Credo pose legitimate competition, but Marvell’s second-largest market share in wired networking didn’t emerge overnight. Their 800G-to-1.6T roadmap aligns perfectly with hyperscaler infrastructure upgrade cycles through 2027.

The Valuation Disconnect

At current prices, MRVL trades at 17.9x forward earnings despite 23.2% revenue growth and expanding margins. Compare that to semiconductor peers commanding 25-30x multiples with inferior growth profiles. The market is pricing in execution risk that may already be reflected in conservative guidance.

Our blended fair value analysis suggests intrinsic worth around $72 per share—14-15% upside from current levels. That incorporates both bull case scenarios where optical networking accelerates and bear cases where custom silicon ramps prove lumpier than expected. The risk-reward profile favors patient capital willing to look beyond quarterly noise.

More importantly, the technical damage has likely run its course. MRVL sits near oversold levels with support building around $60. For investors seeking exposure to AI infrastructure buildout, this selloff represents the type of entry opportunity that emerges once or twice per cycle.

Risk Management in Practice

This isn’t a “back up the truck” recommendation. Semiconductor investing requires discipline, especially with high-beta names like MRVL that can move 15-20% on earnings guidance. Position sizing should reflect volatility tolerance—2-4% maximum allocation in diversified portfolios.

The staged entry approach makes sense here: initial positions in the $60-62 range, with additional tranches if price revisits $55-57 support. Set stop-losses around $50—the level where fundamental thesis breakdown becomes more probable than temporary execution hiccups.

Key monitoring metrics include custom pipeline progression, optical DSP market share trends, and hyperscaler capex allocation. If Marvell can demonstrate consistent quarter-over-quarter growth in both segments through fiscal 2026, the current valuation discount should compress.

The Long Game

Wall Street often confuses quarterly execution with secular opportunity. Marvell’s transformation into an AI infrastructure pure-play positions it for multi-year growth regardless of near-term guidance conservatism. The $2.5 billion war chest provides strategic flexibility rare among mid-cap semiconductors.

Smart investors understand that today’s selloff reflects yesterday’s expectations, not tomorrow’s potential. In a world where AI training clusters double annually and optical networking becomes mission-critical infrastructure, companies like Marvell don’t stay cheap indefinitely.

The question isn’t whether AI networking demand will grow—hyperscalers have no choice but to upgrade their infrastructure. The question is whether investors have patience for the non-linear ramp cycles that define semiconductor investing.

Rating: Primary Buy on Pullbacks ($50-$60 range). Fair Value: ~$72. Position Size: 2-4% maximum.

At $62.87, MRVL offers compelling risk-adjusted returns for investors willing to look beyond quarterly optics toward the multi-year AI infrastructure buildout. The selloff has created the entry opportunity; execution over the next two quarters will determine whether contrarian positioning pays off.

Leave a comment