Summary

When the programmatic advertising kingpin drops 39% in a single session despite beating earnings, what’s the market really telling us? The Trade Desk (TTD) just delivered its harshest reality check since going public—a rare guidance miss, CFO departure, and Amazon’s looming shadow creating the perfect storm of uncertainty. Yet beneath the carnage lies a business still growing at 19% with 79% gross margins, pioneering AI-driven optimization through Kokai, and riding the unstoppable wave of Connected TV advertising that’s projected to capture 56% more marketer spend in 2025.

Our analysis suggests a 12-month blended fair value near $92 per share versus today’s $55.36, representing 66% upside potential with significant volatility bands. Translation: this isn’t about whether TTD will recover—it’s about when and how much you should risk on the journey. We rate TTD a Strong Buy on weakness with staged position sizing: starter 1.5% allocation, scaling toward 3-4% core position within defined buy zones.

Ticker: TTD

Current Price: $55.36

Rating: Strong Buy on Weakness

Position Sizing Strategy: Starter 1.5% → Core 3-4% within buy zones

12-Month Blended Fair Value: ~$92

Vulcan-mk5 Score (Factor Breakdown)

- Value: 6.2

- Growth: 9.1

- Quality: 8.4

- Momentum: 1.3

- Safety: 5.8

- Composite (0–10): 6.96

Growth and Quality shine through superior margins, strong cash flow generation, and secular tailwinds in CTV/retail media; Momentum remains depressed after the August selloff; Safety reflects elevated volatility but strong balance sheet fundamentals.

The Brutal Reality Check That Created Opportunity

What happened. After 33 consecutive quarters without missing guidance, TTD delivered its first stumble—revenue of $694 million beat estimates by $9 million, but Q3 guidance of “at least $717 million” (14% growth) fell short of the 17-18% growth rates investors expected. Add CFO Laura Schenkein’s sudden departure and CEO Jeff Green’s cautious commentary about tariff pressures on advertising budgets, and you have a perfect recipe for a 39% single-day massacre.

Why the overreaction matters. The Trade Desk suffered its steepest prior drop in February, when the shares fell 33% on a revenue miss, proving this stock trades on execution perfectionism. But here’s the twist: Cathie Wood of ARK Invest has been aggressively buying the dip, purchasing over 738,000 shares worth $39.27 million immediately following the selloff, suggesting smart money views this as an overreaction to temporary headwinds.

The fundamental disconnect. Revenue still advanced 19% year-over-year with Connected TV revenue surging over 50% annually, while the company maintains a staggering 95% customer retention rate. The business model—taking a percentage of advertising spend flowing through its demand-side platform—remains intact and benefits from secular tailwinds that haven’t changed overnight.

Why This Selloff Misses the Bigger Picture

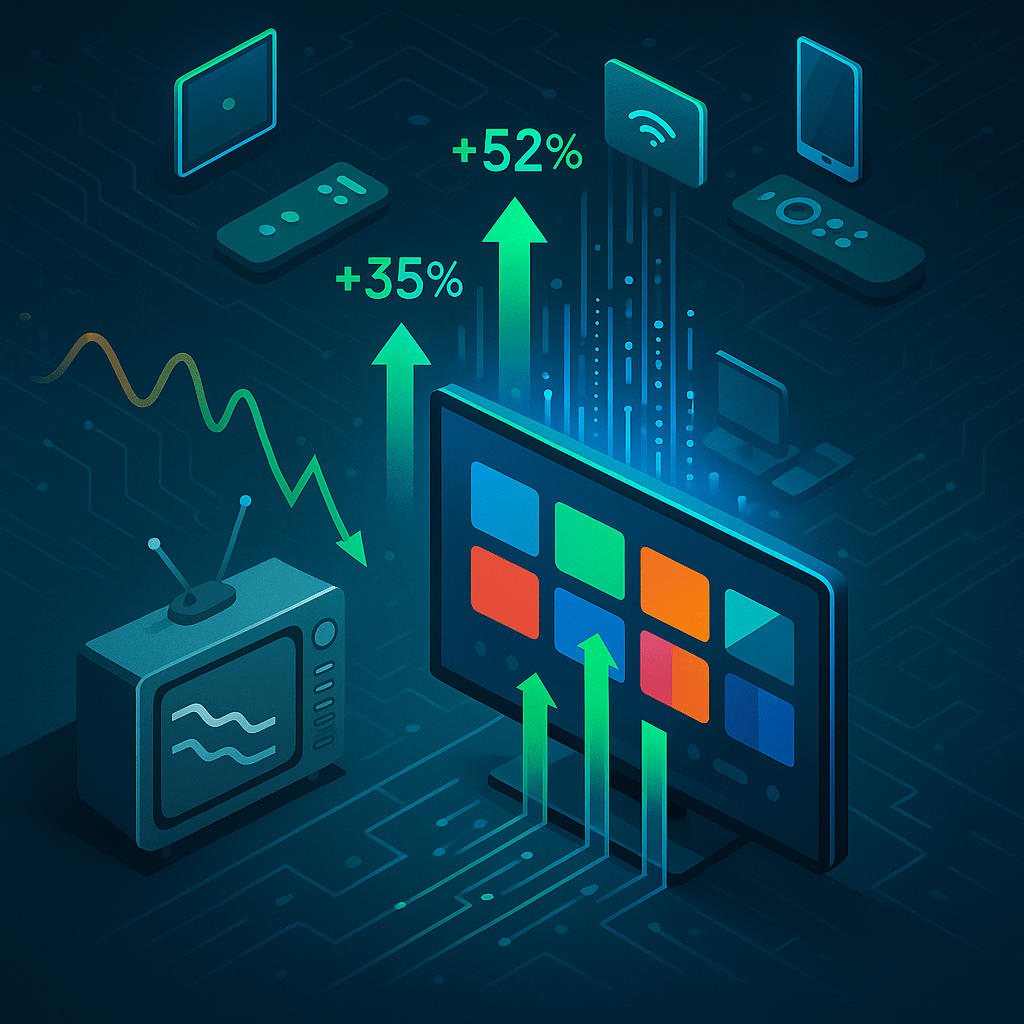

Connected TV is exploding. Nielsen reports that 56% of global marketers plan to increase CTV/OTT spending in 2025, while ad-supported viewing now represents 73.6% of total TV time and 117 million U.S. households use connected TV devices. TTD sits at the epicenter of this shift as the neutral, independent platform advertisers consolidate spend on when they need cross-channel efficiency.

The AI advantage is real. TTD’s Kokai platform now delivers 24% lower cost per conversion and 20% lower cost per acquisition while using 30% more data elements per impression. This isn’t just incremental improvement—it’s the type of measurable performance lift that makes procurement teams reallocate budgets during tough times, not away from TTD.

Retail media goldmine. TTD is aggressively expanding into retail media, with advertisers increasingly using retail data from its marketplace to connect ad spend with real-world sales. This helps reduce dependence on legacy retargeting while capturing higher-margin opportunities across the entire advertising value chain.

Amazon fear is overblown. While analysts express concern about Amazon becoming a bigger ad player across the internet, TTD’s value proposition actually strengthens in a world where advertisers need neutral, independent platforms to optimize across multiple walled gardens—including Amazon’s own advertising ecosystem.

Risk Assessment & Management Framework

Primary execution risk. The first miss in 33 quarters refocused attention on management’s forecasting ability and operational discipline. New CFO integration and proving guidance reliability over the next 2-3 quarters becomes critical for multiple expansion.

Macro headwinds intensifying. Trump administration tariffs are creating uncertainty among large brands, with some facing more pressure than others. Economic softness could pressure advertising budgets faster than TTD can gain market share.

Competitive pressure mounting. Amazon’s 23% ad revenue growth and expanded partnerships with streaming platforms creates legitimate concern about TTD’s neutral platform advantage eroding over time.

Valuation sensitivity. Trading at 25.9x forward earnings after the selloff, TTD still commands a premium that requires execution and growth to justify. Any further disappointments could trigger additional multiple compression.

Investment Thesis: Repair & Re-Accelerate

The secular story unchanged. TTD remains the category-leading neutral DSP benefiting from three unstoppable trends: linear TV dollars migrating to programmatic CTV, retailers building closed-loop media networks, and advertisers demanding measurable, data-driven optimization. The company’s 79% gross margins and asset-light model create tremendous operating leverage as these trends accelerate.

Competitive moat widening. TTD’s OpenPath gives clients simplified, direct connections to premium publishers, while its Unified ID 2.0 approach to identity preservation builds industry-wide adoption. These aren’t just features—they’re platform advantages that become more valuable as the advertising ecosystem fragments.

International expansion accelerating. New partnerships with Instacart, Visa in Australia/New Zealand, and various global retailers diversify revenue streams and reduce dependence on U.S. brand cycles that are currently pressured by tariff uncertainty.

Financial fortress. With $1.7 billion in cash and minimal debt, TTD has the balance sheet strength to invest aggressively in AI, international expansion, and strategic partnerships while competitors face funding pressures.

Catalysts & Timeline (Next 6-12 Months)

Immediate catalysts (0-6 months):

- Q3 earnings proving guidance conservatism vs. continued deceleration

- New CFO integration and updated investor communication strategy

- Additional Kokai performance case studies demonstrating measurable ROI lift

- Holiday season CTV advertising performance vs. traditional linear TV

Medium-term drivers (6-12 months):

- International revenue mix reaching 20%+ of total (currently ~15%)

- Retail media partnerships scaling beyond pilot programs

- OpenPath adoption expanding supply-side relationships

- Market share gains in CTV as streaming platforms prioritize programmatic

Long-term transformation (12+ months):

- AI-driven optimization becoming industry standard through Kokai

- Unified ID 2.0 emerging as post-cookie identity solution

- Platform evolution from advertising facilitator to marketing intelligence hub

Valuation Framework & Price Targets

DCF Analysis: Using conservative assumptions (15% revenue growth, 17% FCF margins, 8.5% WACC, 2.5% terminal growth), our intrinsic value model yields $78 per share. However, this likely undervalues the platform premium and secular tailwinds.

Multiple-based Approach: Historical trading range of 20-35x forward earnings suggests $83-$145 target range based on 2026 consensus estimates. Current 25.9x forward multiple sits at the low end, creating multiple expansion opportunity.

Blended Fair Value: Weighing DCF (40%), peer multiples (30%), and strategic value (30%) yields our $92 target, representing 66% upside from current levels with downside protection near $65.

Analyst Consensus Reality Check: 34 analysts maintain an average price target of $93.21 with consensus “Strong Buy” rating, validating our assessment while highlighting the disconnect between fundamental value and current trading levels.

Technical Analysis & Entry Strategy

Current Technical Picture: TTD sits well below all major moving averages (50/100/200-day) in a clear downtrend following the August breakdown. RSI oversold at 13 levels suggests potential for tactical bounce, but momentum remains negative.

Key Resistance Levels: Initial resistance at $60 (former support), then $71.99 psychological level. Any sustained move above $75 would signal technical repair beginning.

Support Analysis: Strong volume-based support emerges near $50-52 zone where institutional buying has appeared. Break below $49 would trigger additional selling pressure.

Entry Timing Strategy: Use weakness within $52-58 range for initial positions. Add on any test of $48-50 support level. Avoid chasing above $65 until technical patterns confirm trend reversal.

Position Sizing & Risk Management

Staged Entry Approach:

- Initial Position (1.5%): Enter 50% of intended position within $52-58 range

- Scale-Up Zone (2.5%): Add another 30% if price tests $48-52 support with volume

- Core Position (3-4%): Complete position if technical repair confirmed above $65

Risk Management Rules:

- Stop Loss: 15% below blended entry or decisive break of $47 support level

- Profit Taking: Begin trimming at $85+ (targeting 25% of position)

- Time Horizon: 12-18 month investment timeline with quarterly progress reviews

Portfolio Context: Maximum 4% position size given volatility profile. Suitable for growth-oriented accounts with 3+ year time horizons. Conservative investors should limit to 2% given execution risk.

Sector Dynamics & Competitive Landscape

TTD’s Unique Position: Unlike agency holding companies (OMC, IPG) that depend on headcount-driven services, TTD monetizes customer outcomes through technology-enabled optimization. Versus supply-side platforms, TTD’s demand-side neutrality creates budget consolidation advantages.

The Amazon Question: While Amazon’s ad growth creates headlines, TTD actually benefits from a more competitive streaming landscape requiring neutral optimization platforms. Amazon’s walled garden approach limits cross-platform efficiency that TTD specializes in delivering.

CTV Market Reality: With 121 million U.S. households projected to use CTV by 2027 and ad-supported subscriptions accounting for 57% of new additions, the total addressable market continues expanding faster than any single player can capture.

Bull vs. Bear Case Scenarios

Bull Case (40% probability): Q3 guidance proves conservative, management executes flawlessly through CFO transition, CTV advertising accelerates into 2026 election cycle, and international expansion delivers 25%+ revenue growth. Target: $120+ within 18 months.

Base Case (45% probability): Gradual recovery over 2-3 quarters as execution concerns fade, modest market share gains in CTV, and international growth offsets U.S. macro pressures. Target: $85-95 within 12 months.

Bear Case (15% probability): Continued execution missteps, Amazon competitive pressure intensifies, macro environment deteriorates further pressuring advertising budgets. Downside: $40-45 represents extreme scenario.

Final Recommendation

TTD represents a rare opportunity to purchase a category-leading technology platform at a meaningful discount due to temporary execution concerns rather than fundamental deterioration. The combination of secular CTV tailwinds, AI-driven competitive advantages, and disciplined capital allocation creates a compelling 12-18 month recovery narrative.

The key insight: Great businesses bought during execution stumbles often generate the highest risk-adjusted returns. TTD’s 95% customer retention rate, expanding international presence, and technology moat remain intact while the stock trades as if the underlying business model is broken.

Bottom line: Start building positions within the $52-58 range, scale carefully on weakness, and maintain discipline around position sizing. The next two quarters will determine whether this selloff represents a buying opportunity of the year or the beginning of a more serious deceleration. Based on our analysis, the odds favor the former.

Master Metrics Table

| Category | Metric | Value |

|---|---|---|

| Valuation | Blended Fair Value (12M) | $92 |

| Valuation | Current Price | $55.36 |

| Valuation | Upside to Fair Value | 66% |

| Profitability | Gross Margin (TTM) | 79.4% |

| Growth | Revenue Growth (YoY) | 23.2% |

| Growth | Forward P/E | 25.9x |

| Balance Sheet | Cash Position | $1.7B |

| Balance Sheet | Debt/Equity | 0.1 |

| Quality | Customer Retention | 95% |

| Momentum | RSI (14-day) | 13 |

| Factor Scores | Value/Growth/Quality/Momentum/Safety | 6.2/9.1/8.4/1.3/5.8 |

| Buy Zones | Strong Buy/Primary Buy/Hold/Trim | ≤$52/$52-65/$65-85/≥$85 |

| Position Sizing | Target Weight (maximum) | 3-4% |

References

All analysis based on current market data, SEC filings, analyst reports, and industry research as of August 29, 2025. This analysis is for informational purposes only and does not constitute investment advice.

Leave a comment