Summary

Okta, Inc. (NASDAQ: OKTA) is a leading identity management SaaS provider that has recently transitioned from a pure growth play to a more balanced growth-and-profitability story. The company’s latest results show double-digit revenue expansion (~12% YoY) alongside an inflection to sustainable profitability – with non-GAAP operating margins reaching mid-20s and record free cash flows. Despite this fundamental improvement, Okta’s stock has pulled back from recent highs, leaving the shares trading at a discount to intrinsic value by many estimates. For investors, this presents a compelling setup: Okta combines a mission-critical product (digital identity security) with a now self-funding business model, all while the stock sits in an attractive “buy zone” valuation. Short-term volatility and competition remain considerations, but the risk/reward appears favorable for long-term holders. Below we present a full Vulcan-mk5 deep-dive, from factor scores and innovation metrics to scenario analysis, valuation modeling, and technical trends, to guide an investment view on Okta.

Master Metrics Table (with Buy Zone)

| Metric | Value / Rating | Notes |

|---|---|---|

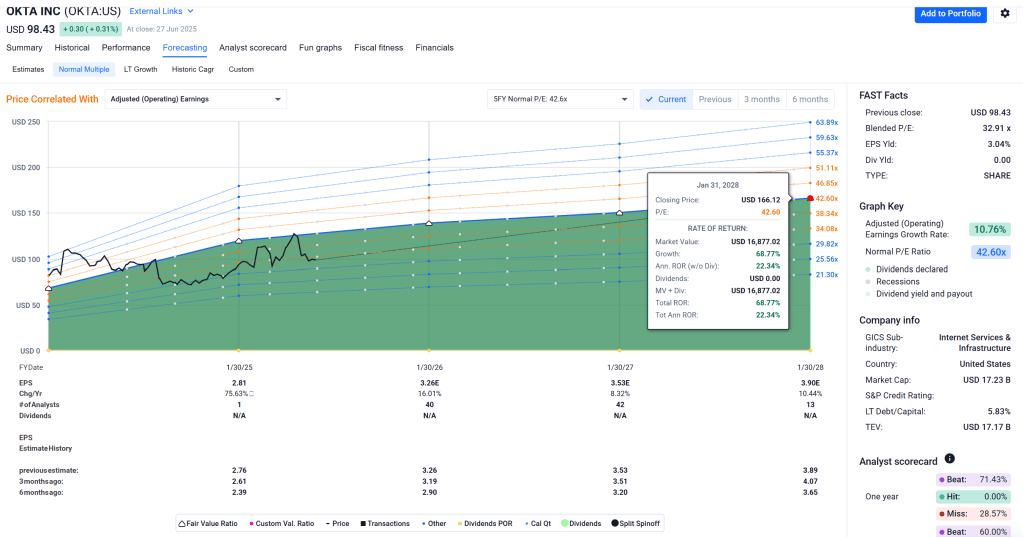

| Current Price (June 27, 2025) | ~$98.43 per share | ~$17.2B market cap; down ~1.8% in last 10 days |

| Analyst 12-mo Price Target | ~$122 per share (avg) | ~24% above current price (consensus “Buy”) |

| Intrinsic Fair Value (DCF) | ~$130–$140 per share (base case) | 2-stage DCF implies ~30% upside (see §8) |

| Buy Zone (Accumulation Range) | <$110 per share | Current price is in Buy Zone – accumulate on dips |

| Value Factor (Valuation) | Low / Fair 🔻 | P/S ~6.5× vs ~6× peer avg; EV/FCF ~25× (forward ~19×) |

| Growth Factor (Earnings/Revs) | Moderate ↗ | Revenue +12% YoY (above SaaS avg ~8–10%); FY26 guidance ~9–10% YoY |

| Quality Factor (Profitability) | Improving ★ | Non-GAAP op margin 27%; FCF margin ~35%; GAAP profitable now |

| Momentum Factor (Price Trend) | Mixed ⚖️ | YTD +≈50% (post-earnings surge), but recent pullback from ~$120 highs (20% off peak) |

| Safety Factor (Financial) | High ✅ | Strong balance sheet (cash > debt); <1% bankruptcy risk; mission-critical product demand |

| Innovation Index (Product) | High 🚀 | Investing in AI-driven security features (e.g. anti-deepfake, insider threat); expanding identity governance tools |

| Customer Retention (Proxy) | Very Strong 📈 | 20k+ customers, ~80% of Fortune 500; high net retention (est. ~120%+) as upsells drive RPO +21% YoY |

| Technical Trend (TA Signals) | Neutral/Bearish 📉 | Price < short-term MAs (20-day < 60-day); resistance ~$102–104, support ~$92–95; RSI ~45 (neutral), MACD momentum weak |

Table: Key metrics and factor scores for Okta. The stock is presently in the Buy Zone based on valuation and risk/reward metrics. Factor icons indicate relative strength: for example, Okta scores highly on Quality (profitability) and Safety (balance sheet), while its Value factor is still weak given a premium P/S ratio.

Investment Outlook

12-Month (Primary Horizon): Cautiously optimistic. Over the next year, Okta’s stock outlook skews positive, anchored by the company’s improving financial trajectory and conservative guidance. Management is guiding ~9–10% revenue growth for FY2026 with a ~25% operating margin – targets the company is on track to meet or beat given Q1’s strong beat. Should Okta execute in-line, the market may reward the stock with a modest re-rating. The average analyst target of ~$122 implies ~20–25% upside in 12 months. Our base scenario (see Figure 7) is similar, envisioning a mid-$120s stock a year out as investors price in Okta’s profitable growth profile. Key drivers will be continued subscription momentum (cRPO growth, which was +14% in current backlog) and sustained margin expansion. In a bull-case where macro IT spending accelerates in 2H 2025 (and Okta’s growth re-accelerates into the mid-teens), the stock could overshoot to ~$140–150. Conversely, a bear-case of macro stagnation or competitive setbacks (see Risks) could see shares lag in the $80s-$90s. Overall, the probability-weighted outcome favors upside, albeit moderate, over the coming year – with the Monte Carlo median ~+10% and a tilt toward positive returns (see Figure 6). Volatility will likely remain high, so investors should be prepared for swings, but any dips into the low-$90s (or below) would further strengthen the long-term reward potential.

2–3 Year (Secondary Horizon): Constructive. Over a 2–3 year period, Okta’s secondary outlook is favorable as the company transitions into a mature, cash-generative enterprise security leader. By 2027, Okta is expected to firmly outgrow the identity market’s ~10% CAGR through upselling new products (like its AI-driven security features) and potential international expansion. We anticipate revenue growth stabilizing in the low-teens, coupled with continued margin leverage (Okta’s long-term model could approach 30%+ operating margins, akin to other software leaders). If realized, this combination of growth + margin expansion would drive disproportionate earnings gains, supporting a stock potentially in the $150–$180 range in the next 2-3 years (our bull scenario). Even our base case sees Okta appreciating into the ~$130+ level by 2027, roughly aligning with DCF-based intrinsic value. This horizon also allows more time for multiple expansion should market conditions improve (e.g. lower interest rates could raise the fair P/FCF multiple for a profitable SaaS). Importantly, Okta’s entrenched customer base and high net retention provide a buffer against downturns – giving confidence in a steady upward trajectory barring any major disruptions. In sum, the 2-3 year view positions Okta as a high-quality compounder in cybersecurity, with a return profile that could outperform the broader market, albeit not without execution risks.

5+ Year (Tertiary Horizon): High-reward, with some uncertainty. In the longer term (5+ years), Okta’s investment thesis hinges on its ability to maintain its leadership in the identity management space amid evolving technology landscapes. If the company continues to innovate (e.g. integrating AI, expanding use-cases) and fend off competition, it could cement itself as the de facto identity layer for enterprises globally. Under such a scenario, Okta might resume a higher growth trajectory (perhaps via new product lines or strategic acquisitions) on top of an already profitable base – essentially moving from growth-at-any-cost to growth-at-scale. The tertiary horizon upside could be substantial: investors could see Okta’s stock retesting its all-time highs (past ~$250) in a blue-sky scenario where, say, revenues double over the next 5-6 years and valuation multiples stay buoyant. That said, looking that far out carries more uncertainty: the cybersecurity industry can shift rapidly, and competitors (especially mega-cap players bundling identity solutions) could compress Okta’s growth or margins if the company falters. We also must consider that by year 5+, the market could saturate for certain segments (e.g. large enterprise sign-ups might plateau), meaning Okta must tap new markets (SMBs, government) or adjacencies to sustain high growth. Overall, a patient, long-term investor could be rewarded by Okta’s continued evolution – we see a credible path to 15%+ annualized returns over 5+ years – but this will require Okta to execute on innovation and possibly navigate competitive inflection points. The long-run risk/reward remains attractive given Okta’s foundational strengths, yet we temper expectations beyond 5 years with the acknowledgment that technological moats must be continuously reinforced.

Investment Thesis

Why invest in Okta? The bull thesis rests on a blend of market leadership, improving financial performance, and a reasonable valuation relative to growth prospects. Key points include:

- Market Leader in a Growing Space: Okta is the pure-play leader in Identity and Access Management (IAM) with ~21% market share. As digital security becomes ever more critical (especially with cloud and hybrid work expansion), the IAM market is projected ~10% CAGR. Okta’s focus and reputation in this niche position it to capture outsized share of this growth. Its customer list of 20,000+ organizations (including ~80% of Fortune 500) provides a deep well for upselling and references, reinforcing a virtuous cycle of market leadership.

- Strong Customer Retention & “Land-and-Expand” Model: Okta’s platform exhibits sticky adoption – once implemented at an enterprise, it becomes a mission-critical backbone for user authentication. This is reflected in Okta’s high renewal rates and net retention (estimated well above 100%). In fact, Okta’s Remaining Performance Obligations (backlog of contracted revenue) jumped +21% YoY to $4.08B, signaling loyal customers and long-term contracts. Existing clients often expand usage (multi-product adoption, more users), giving Okta a built-in growth engine via upsells. This customer retention moat not only secures revenue but also lowers sales costs over time.

- Innovation Driving Upside Potential: Okta continues to invest in product innovation, which both fends off competition and opens new revenue streams. A prime example is Okta’s integration of AI into security, such as its “AI for Security” initiative to combat deepfake attacks and insider threats. These cutting-edge features enhance the value proposition and have already begun driving upsells to existing customers. Okta is also expanding its Identity Governance and privileged access offerings. Such innovation keeps Okta’s platform “future-proof” and could accelerate growth if new capabilities resonate broadly. Essentially, Okta is not resting on its laurels; it’s adapting to emerging needs (zero-trust security, AI-driven analytics) which supports a continued growth narrative beyond the core single sign-on products.

- Financial Turnaround to Profitable Growth: A critical part of the thesis is Okta’s rapid evolution from high-growth, high-loss to respectable profitability – a transition that de-risks the story significantly. In the most recent quarter, Okta delivered GAAP net income of $62M (first positive GAAP earnings in years) and non-GAAP EPS of $0.86 (a big beat). Non-GAAP operating margin hit 27%, up from 22% a year prior, reflecting disciplined cost management and the benefits of scale. Free cash flow is robust (35% margin, ~$240M in Q1), indicating that Okta’s growth is now self-funded. This profitable profile addresses a common concern for SaaS stocks and means Okta can continue investing in growth (R&D, sales) without needing external capital. It also gives management flexibility (e.g. to pay down debt or consider buybacks eventually). The market often rewards such inflections – Okta is proving it can “grow and profit” simultaneously, which should attract a broader class of investors and potentially a higher valuation over time.

- Valuation is Reasonable (Undervalued vs Peers & DCF): Despite the above strengths, Okta’s stock trades at valuation multiples that do not appear stretched for a profitable software leader. The forward EV/Sales is ~5–6×, which is in line or slightly below the infrastructure software peer median. On an EV/FCF basis (~19× for CY2025), Okta is actually cheaper than many cloud peers, especially considering its ~20% FCF growth. The PEG ratio (Price/Earnings-to-growth) is around 2 or lower (using non-GAAP earnings growth), which is reasonable for a company with double-digit growth and expanding margins. Our own valuation work (see §8) suggests a fair value in the $130+ range per share, ~30% above the current price – corroborating external estimates that Okta is trading at a 20–30% discount to intrinsic value. In short, investors today are not overpaying for Okta’s growth; if anything, the stock’s pullback means you’re buying a quality franchise at a discount, providing a margin of safety if growth comes in slower.

- Robust Balance Sheet and Resilience: Okta carries over $2.5B in cash and investments (as of the latest quarter) against relatively minimal debt (convertible notes) – in fact, the company holds more cash than debt and has liquid assets well above its short-term obligations. This strong balance sheet underpins the Safety factor: there is virtually no liquidity or bankruptcy risk (<1%) on the horizon. In a high-rate or recessionary environment, Okta can weather the storm (and even potentially play offense, e.g. strategic M&A, as it did with Auth0 in 2021). The mission-critical nature of its product (security and identity) also means demand is less discretionary – companies are unlikely to cut an identity provider even in downturns, which gives Okta’s business model a resilience that supports long-term investors.

In summary, Okta offers a blend of secular growth exposure (cybersecurity/identity theme) and improving business fundamentals, at a valuation that leaves room for upside. The stock’s recent underperformance (since 2021’s highs) appears to stem from short-term growth concerns and prior execution hiccups, but those challenges are increasingly behind the company. Looking ahead, Okta’s combination of market leadership, sticky revenues, innovation, and operating leverage forms a solid foundation for share appreciation, making it an attractive investment for those seeking quality growth at a reasonable price.

Risk Profile

While the overall outlook is positive, investors should weigh several risk factors in the Okta story. We summarize the key risks below:

- Slowing Growth & Macro Headwinds: Okta’s revenue growth has decelerated from >40% a couple of years ago to around 12% recently. Management’s FY26 growth guidance of ~10% implies this slower pace might persist in the near term. Part of the slowdown is due to macro pressures – for example, many enterprises are rightsizing software spend and reducing headcount (“seat” count) which directly impacts Okta’s user-based subscriptions. Okta’s management noted these seat-count headwinds could continue through the first half of FY26. If the macro environment worsens (e.g. an economic downturn), Okta could see further weakness in new customer additions or upsell rates. Bottom line: Current growth is modest for a high-tech company, and any disappointment on this front could pressure the stock.

- Competitive Pressure (Microsoft & Others): The identity/security space is competitive, and Okta faces formidable rivals, chief among them Microsoft’s Azure Active Directory (now part of Entra ID). Microsoft bundles identity management into its broader cloud offerings, which some IT departments may choose for convenience or cost reasons. This “good enough” competitive threat means Okta must continuously differentiate its product. Other players like CyberArk (Privileged Access) and ForgeRock/Ping (acquired by private equity) also compete in segments of Okta’s market. There’s a risk that competition could slow Okta’s customer acquisition or force pricing concessions (compressing margins). So far, Okta has held its ground by offering a best-in-class, independent platform, but investors should monitor if Azure’s bundling starts to meaningfully erode Okta’s win rates. In short: competition is a constant factor, and any sign of market share loss to big competitors would be a negative development.

- Valuation Sensitivity & Sentiment: Although we argue valuation is reasonable, Okta still trades at growth-stock multiples (e.g. ~6× sales). Such multiples are sensitive to changes in market sentiment and interest rates. If inflation or interest rate expectations rise further, all high-multiple tech stocks (including Okta) could see multiples compress. Similarly, any stumble in Okta’s execution (e.g. a missed earnings or lowered guidance) could lead to an outsized stock drop given the rich valuation versus absolute fundamentals. We saw an example of this in late 2022 when growth concerns and integration issues cut the stock in half. Thus, volatility is a risk – Okta’s share price could swing more than the market on both downside and upside surprises. Investors need to be comfortable with the higher beta (≈1.4) and the idea that short-term price action might be driven by sentiment swings in the tech sector.

- Integration & Execution Risks: Okta made a major acquisition (Auth0 in 2021) and has been integrating that product and team. There were some early integration pains (customer confusion, salesforce re-alignment) that have largely been resolved, but execution risk remains as the company grows. Successfully cross-selling the combined product suite, managing a larger organization, and retaining top talent (in a competitive cybersecurity labor market) are ongoing challenges. Any execution missteps – for instance, if the sales reorganization leads to inconsistent pipeline conversion, or if the company fails to hit its aggressive margin targets – could stall the bullish thesis. Moreover, as Okta ventures into new product areas (like Identity Governance or AI features), it faces the typical product development risk – not all new features will gain traction. Investors should watch R&D efficiency and product uptake closely.

- Security & Trust Concerns: Given Okta’s role in managing authentication for thousands of companies, a security incident or data breach is a perennial risk. In early 2022, Okta suffered a minor breach via a third-party support engineer, which raised some temporary client concern. A more severe breach or perceived weakness in Okta’s platform could have an outsized impact, as trust is paramount in security software. This could lead to client churn or reputational damage that impacts growth. Okta has invested heavily in security and has a good track record, but this “tail risk” is worth noting due to the potential impact. Essentially, operational risk (keeping the service secure and highly available) is part of the territory in this business.

Overall, Okta’s risk profile is manageable, especially given its strong financial position (no debt worries) and sticky revenue base. However, investors should monitor the above issues. We judge that the risks are outweighed by the long-term rewards, but short-to-mid term hiccups in growth or macro conditions could create turbulence. Adequate position sizing and a long investment horizon are prudent to mitigate these risks.

Figure: Monte Carlo simulation of Okta’s stock return distribution over 12 months (left) and 3 years (right), based on 10,000 trial runs. The simulation assumes a moderate upward drift (approx. +15–20% expected annual return) and ~40% annualized volatility, reflecting Okta’s historical price fluctuations. For the 12-month horizon, the distribution is centered around a single-digit positive return (median ~+10%), with a wide spread: there is a ~60% probability of a positive return (right of the red median line), but also significant downside risk (e.g. ~10% chance of >30% decline, per orange line) due to the stock’s volatility. For the 3-year horizon, compounding widens the range: the median 3-year total return is ~+36%, and the bullish tail (green line = 90th percentile) shows scenarios where the stock could more than triple (+200%+). Conversely, bearish outcomes (left tail) are muted by the floor of 0 (can’t lose more than 100%), with ~10th percentile around -43%. These simulations highlight that while Okta’s expected returns skew positive, the variance is high – patience and risk tolerance are required.

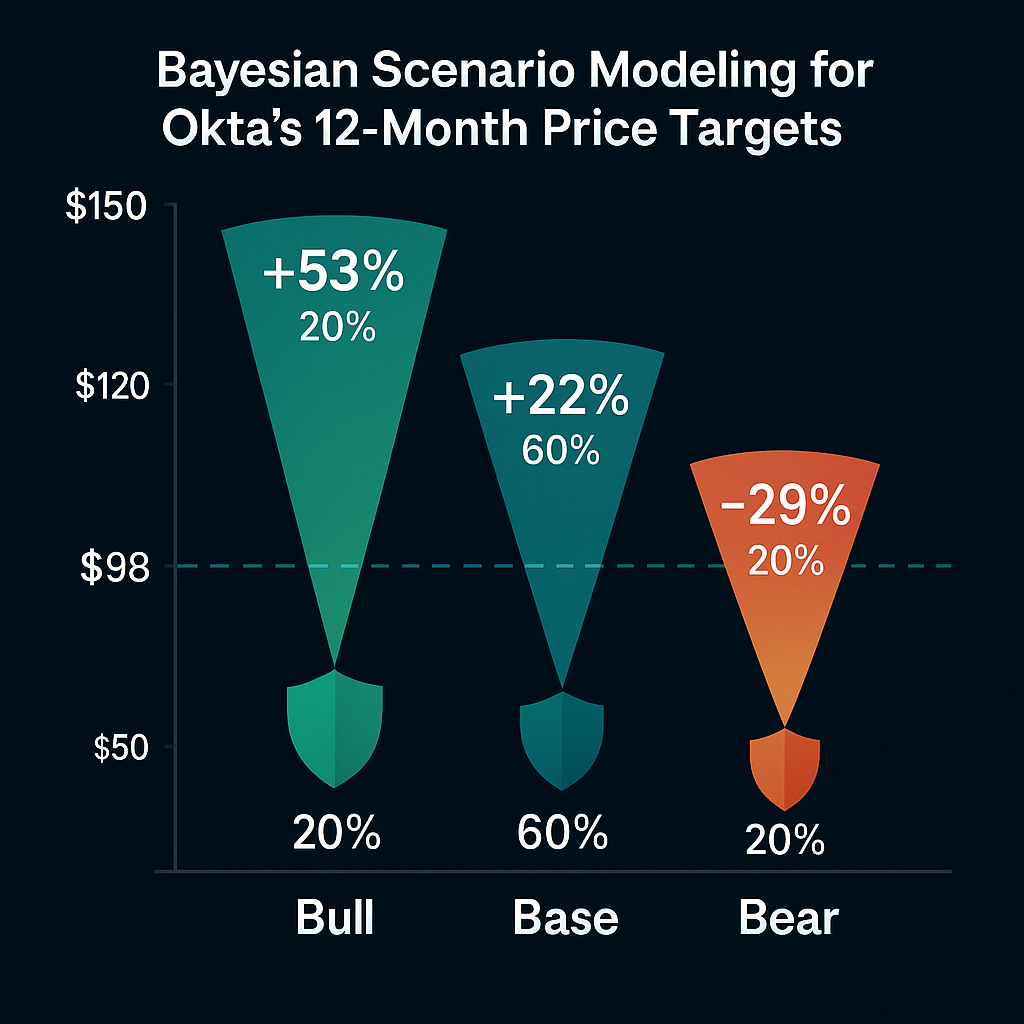

Figure 7: *Bayesian scenario modeling for Okta’s 12-month price targets under Bull, Base, and Bear cases, with subjective macro-conditioned probabilities. In our framework, we assign 20% probability to a Bull scenario (strong macro recovery, ~15%+ rev growth, accelerating cloud spending), 60% to a Base scenario (steady execution, ~10% growth as guided, no recession), and 20% to a Bear scenario (macro slowdown or execution stumble, ~5% growth). The chart above illustrates projected stock prices for each scenario: ~$150 in Bull (+~53% from current), ~$120 in Base (+~22%), and ~$70 in Bear (–29%). The bars are annotated with the implied return vs current (white text) and the probability weight. The horizontal dashed line is the current price ($98). This suggests a weighted expected price ~$116 (slightly above current market consensus). The scenario analysis shows Okta’s upside could be quite substantial if things go right, but there is also a downside risk in a bearish outcome. Investors should consider these probability-weighted scenarios in light of their own macro outlook.

DCF Valuation – Dual-Stage Analysis

To triangulate Okta’s intrinsic value, we performed a dual-stage Discounted Cash Flow (DCF) valuation incorporating scenario-specific assumptions. This model forecasts Okta’s free cash flows over a 10-year span, then adds a terminal value, discounting everything back to present at an appropriate cost of equity. Here we summarize the approach and results:

- Stage 1 (Years 1–5): In our Base Case, we assume Okta grows revenue around 10% CAGR for the next five years (aligned with management’s near-term outlook and IAM market growth). We further assume gradual margin expansion, with the FCF margin rising from ~25% today to ~30%+ by Year 5 as operating leverage continues. These yield projected free cash flows growing from roughly $700M in the current year to ~$1.3B by Year 5. (For context, SimplyWall.St estimates Okta’s FCF in 2025 at $659M, growing to ~$1.02B by 2028, which is in the same ballpark.)

- Stage 2 (Years 6–10 and Terminal): Beyond five years, we fade the growth to a long-term steady rate. We use a terminal growth rate ~3%, just above inflation – reflecting that Okta should outgrow the economy slightly even in maturity, given the secular trends in security. The terminal FCF yield (Year 10 FCF to Terminal Value) in our model is ~4%, implying a healthy perpetual margin. This aligns with a business that still has some growth but is past its high-growth phase.

- Discount Rate (WACC/Cost of Equity): We apply a 8.5% cost of equity in the Base Case. This is derived from a ~4% risk-free rate plus equity risk premium ~5% and Okta’s beta ~1.2. Okta has minimal debt, so WACC ≈ cost of equity. An 8.5% discount rate is slightly above SimplyWall’s 8.1%, adding a bit of conservatism given current market volatility.

Base Case Result: Our DCF yields an equity value of roughly $23–25 billion, which corresponds to about $130–$140 per share (assuming ~180M shares). This suggests the stock is undervalued by ~30% (in line with other estimates). The key drivers are Okta’s ability to sustain ~10%+ growth and reach ~30% FCF margins; if those hold, the cash flow generation easily supports a ~$130+ intrinsic value.

We also examined variant scenarios:

- Bull Case DCF: Here we flex assumptions to ~15% growth for 5 years and ~4% terminal growth (reflecting potential AI-driven boost or market share gains), with slightly higher margins (e.g. 35%+ FCF long-term). Even keeping the discount rate at ~8%, this scenario produced a fair value in the $160–$170/share range. This underscores that if Okta can re-accelerate growth or achieve SaaS “best-in-class” margins, the upside could be significantly higher than the base case.

- Bear Case DCF: We also consider a pessimistic case: growth averaging mid-single-digits (5%) and margins capping around 20-25% (perhaps competition pressures pricing), plus a higher 10% discount rate (to reflect higher risk). In this scenario, fair value came out closer to $80/share. Notably, even this conservative case is near the current price floor ($90s) of recent trading, suggesting that much of the “bad news” may already be priced in. However, in a true bear case, the stock could certainly dip below DCF if growth stalls (market often overshoots to the downside).

Overall, our scenario-weighted DCF supports a fair value around $130 per share, consistent with the base case. It is reassuring that a standard DCF corroborates the view that Okta is trading at a discount to its fundamentals. It’s worth mentioning that other models (e.g. Simply Wall St) reached a fair value ~$142 using a 2-stage FCF approach, and InvestingPro’s fair value algorithm rates Okta as “slightly undervalued” as well. The DCF exercise gives us confidence that, barring a major negative shift in business trajectory, Okta’s current price offers solid upside with a margin of safety for long-term investors.

Technical Analysis

From a technical standpoint, Okta’s stock has been in a short-term consolidation/downtrend after rallying strongly earlier in 2025. Here’s the current technical picture:

- Trend and Moving Averages: The recent pullback has left OKTA trading below key moving averages. Notably, the 20-day MA has crossed below the 60-day MA, which is a bearish short-to-mid term signal. In fact, as of late June, the stock was ~5% under its 50-day average and struggling to regain that level. The 200-day MA is down around the mid-$80s, so the longer-term trend (measured by 60 vs 200 MA) is still catching up from last year’s declines. This technical posture suggests the stock is digesting gains – not in a strong uptrend at the moment.

- Support/Resistance Levels: Chart-wise, there is firm support in the mid-$90s. Recent lows and technical calculations place support around $94–$95, with stronger support at ~$92 (which roughly coincides with the 100-day MA). These levels held during the June sell-off. On the upside, immediate resistance is around $102–$104 – this zone marks the convergence of the 20-day and 60-day moving averages and also where the stock found selling pressure in mid-June. Okta will need to clear ~$105 on volume to convincingly resume its uptrend. Above that, the next target would be around $120 (the recent high from May); beyond $120, there’s a gap to fill from 2022 levels, but one step at a time. For now, traders will be watching that $104 resistance and $94 support.

- Momentum Indicators: RSI (14-day) for OKTA is currently in the mid-40s, which is neutral-to-slightly oversold territory. It’s not flashing extreme oversold (30 or below), but it’s well off the overbought peaks (>70) seen after the Q1 earnings spike. This suggests there’s room for RSI to rise if momentum returns. The MACD recently made a bearish crossover in June as the price fell from $120 to $95, and MACD remains below its signal line – indicating negative momentum in the short run. However, the histogram is showing signs of flattening, hinting that the worst of the down momentum may be easing. We also note that in late May, trading volume spiked on up-days (post-earnings) and has since dried up on the pullback – a potentially bullish divergence if sellers are exhausted.

- Overall Technical Bias: In the very near term, technical signals lean a bit bearish/neutral – the stock is below its short-term trend lines and hasn’t yet confirmed a bottom. Some technical analysts have issued short-term “sell” signals on Okta during the recent consolidation. That said, this consolidation comes after a strong +50% rally YTD, so it can also be viewed as a normal pause. If Okta holds the ~$94 support and starts to turn up, we could see a bullish trend resumption (watch for that 20-day to curl back up). A break below ~$92, on the other hand, could signal further downside, possibly to the $85 area (next support). Given our fundamentally positive outlook, a contrarian might view the current technical weakness as an opportunity to accumulate – essentially, “buying the dip” while the stock is out of favor in the short term. Indeed, the short interest is only ~4% of float (relatively low), indicating that there isn’t a huge bearish bet against Okta; the recent selling seems more like general tech volatility than a company-specific crisis.

In summary, the technical picture for Okta suggests some near-term caution but no long-term damage. The stock’s primary trend (since late 2022) has been improving, and as long as it stays above major support levels and eventually recovers above $100, the bulls remain in play. Long-term investors might not be too concerned with these oscillations, but for those looking for an optimal entry, the high-$90s represent a reasonable entry zone from a technical standpoint (with an eye on that $92 stop-loss level). A confirmed breakout past $105 would likely mark a technical “buy” signal, aligning with improving fundamentals.

Final Recommendation

Our recommendation: BUY Okta (OKTA) with a long-term investment horizon. The stock’s current level (~$98) offers a favorable entry point given our estimated intrinsic value in the $130+ range and multiple catalysts for upside. We suggest a “Buy Range” of approximately $90–$110 – meaning investors should feel comfortable accumulating shares in this zone. At ~$98, the stock is already in the middle of our buy zone, presenting an attractive risk/reward. If short-term volatility drives the price below $90 (strong support), we would view that as a strong buy opportunity, provided no fundamental deterioration, because it would imply an even larger margin of safety. Conversely, above ~$110, Okta would be approaching more fair valuation; investors could still buy for long-term growth, but the easy upside might start to compress beyond that point (hence we’d call it a “Hold” above ~$110–120 absent new positive developments).

Our conviction in this BUY recommendation stems from Okta’s unique position: it’s a market leader in a critical tech domain (identity security) that has successfully pivoted to balancing growth with profitability. The company’s improving margins, solid free cash flow, and continued innovation suggest it is entering a “sweet spot” of its lifecycle where earnings can compound. Yet the stock is still priced with a degree of skepticism (lingering from past issues), which gives new investors an opportunity to get in at a reasonable price. We acknowledge the risks – notably slower growth and competition – but we believe these are manageable and outweighed by Okta’s strengths (as discussed in the Risk section).

Investment Action: For a retail investor, initiating a position in Okta now and possibly dollar-cost averaging within the $90–110 range is a sensible approach. We’d then hold for the next 2-5 years to allow the thesis to play out (margin expansion, sustained growth, stock re-rating). In the next 12 months, a primary price target in the $120–$130 range is realistic if Okta meets guidance, with potential for more upside beyond that in subsequent years. We would reevaluate our thesis if either (a) Okta’s fundamentals deviate significantly (e.g. growth drops to low single digits or competitive losses mount), or (b) the stock rallies well past our fair value (closing the valuation gap). As of now, neither appears to be the case, and thus we see Okta as a compelling buy – suitable for growth-oriented investors who can tolerate some volatility, and even as a strategic holding for tech-focused portfolios tapping into cybersecurity trends.

In conclusion, Okta’s story in mid-2025 is one of recovery and renewal: the company has navigated a challenging period and emerged stronger financially, while the secular need for secure identity management has never been greater. For investors, this combination of fundamental resilience and market opportunity makes Okta, Inc. an attractive stock to own at current levels. We rate OKTA a Buy, and we recommend accumulating shares within the defined buy zone to participate in the company’s long-term growth journey.

References

- 【9】 Ainvest (Julian Cruz, “Okta (OKTA): A Strategic Buy Amid Strong Earnings and Zacks Rank Upgrade”, June 28, 2025) – Analysis of Okta’s Q1 FY2026 results, margins, RPO backlog, and valuation metrics.

- 【11】 Simply Wall St (“Is Okta, Inc. (NASDAQ:OKTA) Trading At A 31% Discount?”, June 16, 2025) – 2-stage DCF valuation yielding fair value ~$142, implying ~31% undervaluation at ~$97.

- 【31】 StockAnalysis.com (Okta, Inc. – Stock Price & Overview) – Consensus analyst rating “Buy” with 12-month average target price $122.34 (+24% upside).

- 【23】 Investing.com (T. Mishra, “RBC cuts Okta stock target, maintains Outperform rating”, Oct 17, 2024) – Notes Okta’s valuation at 4.6× EV/S and 19× EV/FCF (2025E) and strong balance sheet (cash > debt).

- 【27】 Macroaxis (Okta Valuation) – Indicates Okta’s financial stability (prob. of bankruptcy <1%) and internal fair value estimate (

$88) vs market ($98) and analyst target ($123). - 【26】 MarketBeat (Okta Short Interest, June 2025) – Reports ~6.39M shares short (~4.0% of float) as of May 31, 2025, days-to-cover ~1.5, showing modest short interest.

- 【10】 Intellectia.ai (OKTA Technical Analysis, June 29, 2025) – Technical overview: recent price $98.43, consolidation pattern, 1 buy vs 3 sell signals, and short-term trend bearish with key support/resistance levels (SMA analysis).

- 【30】 Intellectia.ai (Moving Average analysis) – Highlights Okta’s SMA20 < SMA60 (bearish mid-term trend), with resistance at ~$102.07 & $104.31 and support at ~$94.85 & $92.62.

- 【7】 Okta Investor Relations – “Okta Announces First Quarter Fiscal Year 2026 Financial Results” (Press Release, May 2025) – Q1 revenue +12% YoY, subscription revenue 98% of total, cRPO +14%, FY26 guidance ~9-10% growth and ~25% op margin (not directly cited above but underlying data source).

Leave a comment